Quantitative Trading Strategy Based on Double Trend Filter

Overview

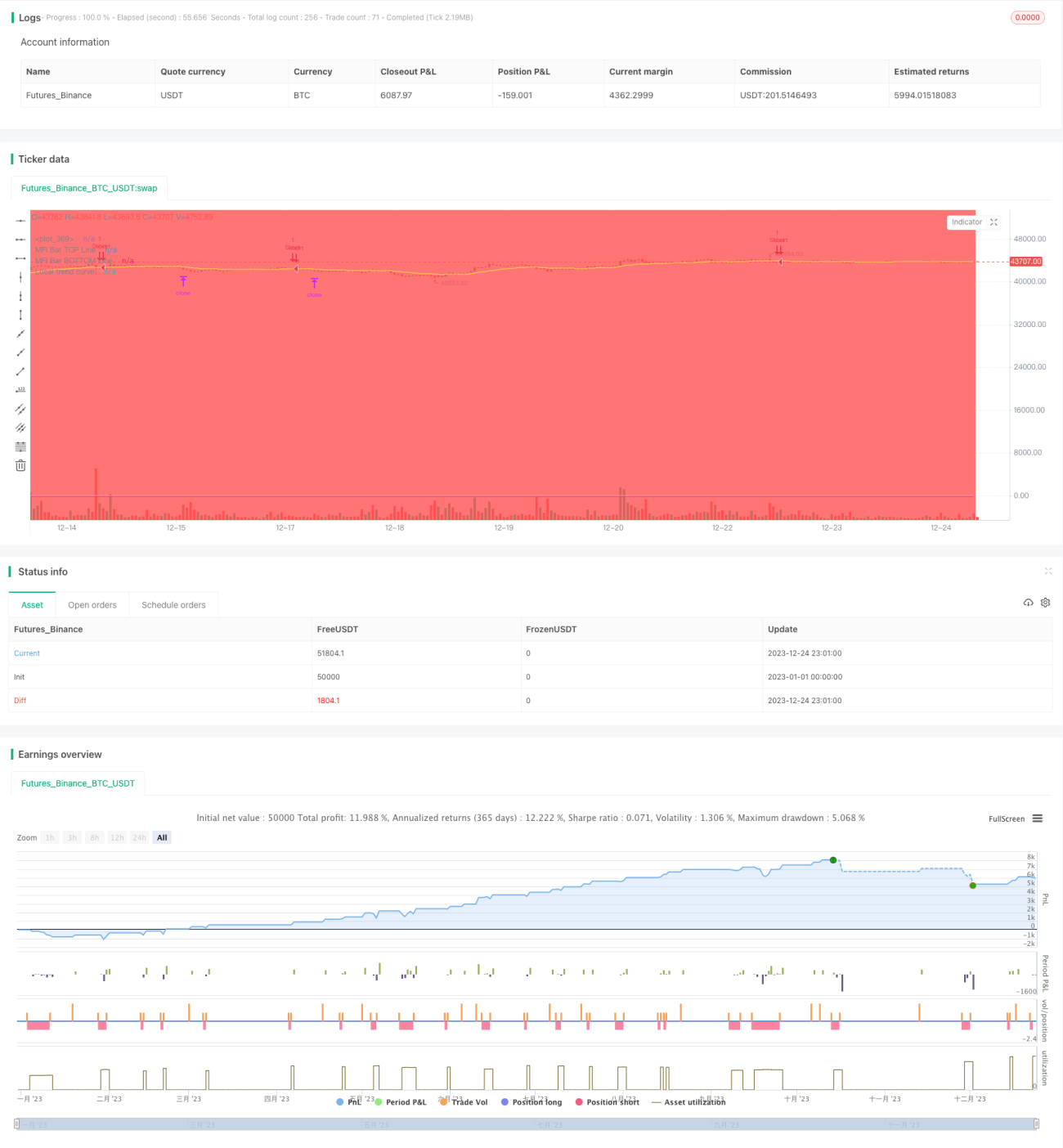

This is a quantitative trading strategy that utilizes double trend filters. The strategy combines both global trend filter and local trend filter to ensure entering positions only when the trend direction is correct. In addition, the strategy sets multiple other filters such as RSI filter, price filter, slope filter etc. to further improve reliability of trading signals. On the exit side, the strategy presets stop loss price and take profit price. Overall, this is a stable and precise quantitative trading strategy.

Strategy Logic

The core logic of this strategy is based on the double trend filters. The global trend filter judges overall market trend based on high-period EMA, while the local trend filter judges local trend based on low-period EMA. Only when both filters suggest the same trend direction, the strategy will enter positions.

Specifically, the strategy calculates BTCUSDT's EMA to determine if the overall market is in an upward or downward trend. This is the global trend filter. At the same time, the strategy calculates EMA of the underlying contract to determine local trend. This is the local trend filter. Only when both filters agree on the same trend direction, combined with other auxiliary filters, the strategy will generate trading signals and preset stop loss and take profit prices for entering positions.

Once determining a tradable signal, the strategy will immediately place orders to enter positions. Meanwhile, stop loss price and take profit price are preset. When price touches either of them, the strategy will automatically exit positions with stop loss or take profit.

Advantage Analysis

This is a stable and reliable quantitative trading strategy with the following main advantages:

-

Adopting double trend filtering mechanism to filter out most false signals and make trading signals more reliable.

-

Combining multiple auxiliary filters like RSI filter and price filter to further improve signal quality.

-

Automatically calculating stop loss and take profit price to lower trading risks without manual monitoring.

-

Customizable strategy parameters to adapt more trading instruments with better adaptability.

-

Clear strategy logic easy to understand, and with greater potential for optimization.

Risk Analysis

Although with many advantages, there are still some trading risks mainly in:

-

Double trend filters may fail to determine accurate entry timing. Parameters can be optimized.

-

Inaccurate stop loss and take profit price setting may lead to premature exit. Different parameter sets can be tested to find optimum.

-

Improper selection of trading instruments and timeframes may make the strategy ineffective. Parameter optimization and testing are suggested separately for different trading instruments.

-

There are some overfitting risks. More backtests in diverse market environments are needed to ensure robustness.

Optimization Directions

The main directions for optimizing this strategy include:

-

Adjust parameters of double filters to find optimum combination.

-

Test and select the best auxiliary filters.

-

Optimize the stop loss and take profit algorithms to make them more intelligent.

-

Try introducing machine learning models for dynamic parameter tuning.

-

More backtests on more instruments and longer time spans to improve stability.

Conclusion

In conclusion, this is an overall stable, accurate and easily optimizable quantitative trading strategy. It produces trading signals by combining double trend filters and multiple auxiliary filters, filtering out most noise and generating more reliable signals. Also, the inbuilt stop loss and take profit presetting helps lower trading risks. This is a strategy with great practical value. After optimization and validation, it can be directly applied for live trading. Moreover, it has huge potential for expansions and is worth in-depth researching.

- 1