Dual-Factor Combo Reversal and Mass Index Strategy

Overview

This strategy is a combo reversal trading strategy based on a dual-factor model. It integrates the 123 reversal pattern and the Mass Index factors to achieve a cumulative effect for the strategy signals. It will only go long or short when both factors emit a buy or sell signal simultaneously.

Strategy Logic

123 Reversal Factor

This factor operates based on the 123 price pattern. When the closing price relationship over the past two days is "low-high" and the Stoch indicator is below 50, it signals a bottom reversal and goes long. When the closing price relationship is “high-low” and Stoch is above 50, it signals a top reversal and goes short.

Mass Index Factor

This factor judges trend reversals based on the expansion or contraction of the price fluctuation range. As the range expands, the index rises and as the range narrows, the index falls. It generates a sell signal when the index crosses above a threshold and a buy signal when crossing below a threshold.

The strategy only opens positions when the two factors emit signals in the same direction, achieving profitable trades while avoiding false signals from a single factor.

Advantage Analysis

- Dual-factor model combines price pattern and volatility indicator for better signal accuracy

- 123 pattern catches local extremums, Mass Index captures global trend reversal points, complementary strengths

- Only taking signals when two factors agree avoids false signals and enhances stability

Risk Analysis

- Probability exists for both factors to emit wrong signals concurrently, causing losses

- Failure rate of reversals exists, need to set stop loss to control downside

- Improper parameter tuning may lead to overfitting

Risks can be reduced via expanding training set, strict stop loss, multi-factor filtering etc.

Optimization Directions

- Test more price and volatility indicator combinations

- Add ML model to judge signal quality and dynamically size positions

- Incorporate volume, Bollinger Bands etc. to discover more alpha

- Employ walk forward optimization for robustness

Conclusion

This strategy combines two factors, price pattern and volatility indicator, to only take signals when they agree, avoiding false signals from a single factor and improving stability. But risks remain for concurrent wrong signals. We can further enhance performance and risk-adjusted returns by expanding dataset, setting stop loss, optimizing factor combinations and more.

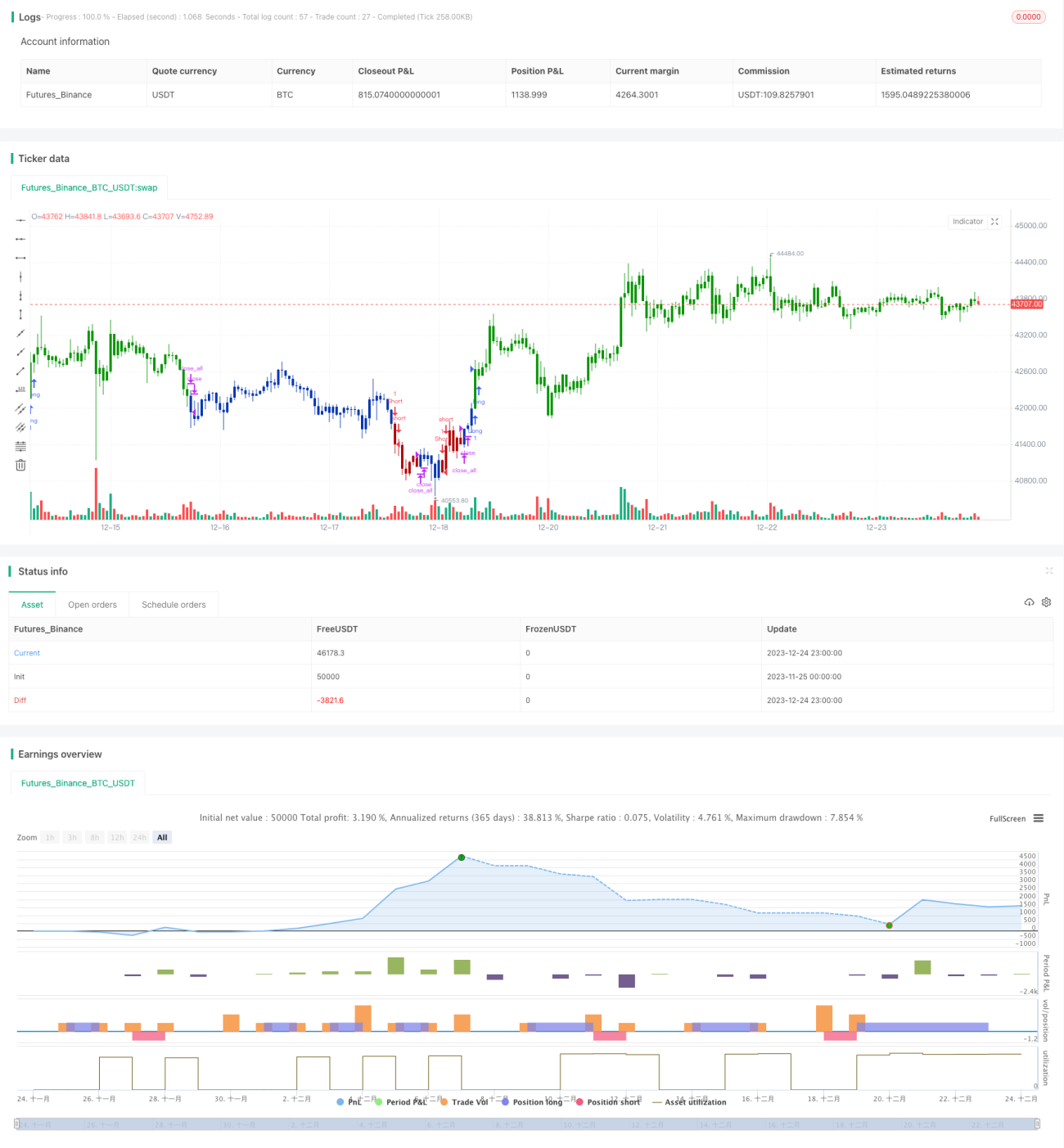

/*backtest

start: 2023-11-25 00:00:00

end: 2023-12-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/02/2021

// This is combo strategies for get a cumulative signal. - 1