Moving Average Envelopes Trading Strategy

Overview

The Moving Average Envelopes trading strategy is a trend following strategy. It sets up percentage envelopes above and below a moving average line as trading signals when price breaks out the envelopes. The strategy can be used for both trend following and identifying overbought/oversold market conditions.

Strategy Logic

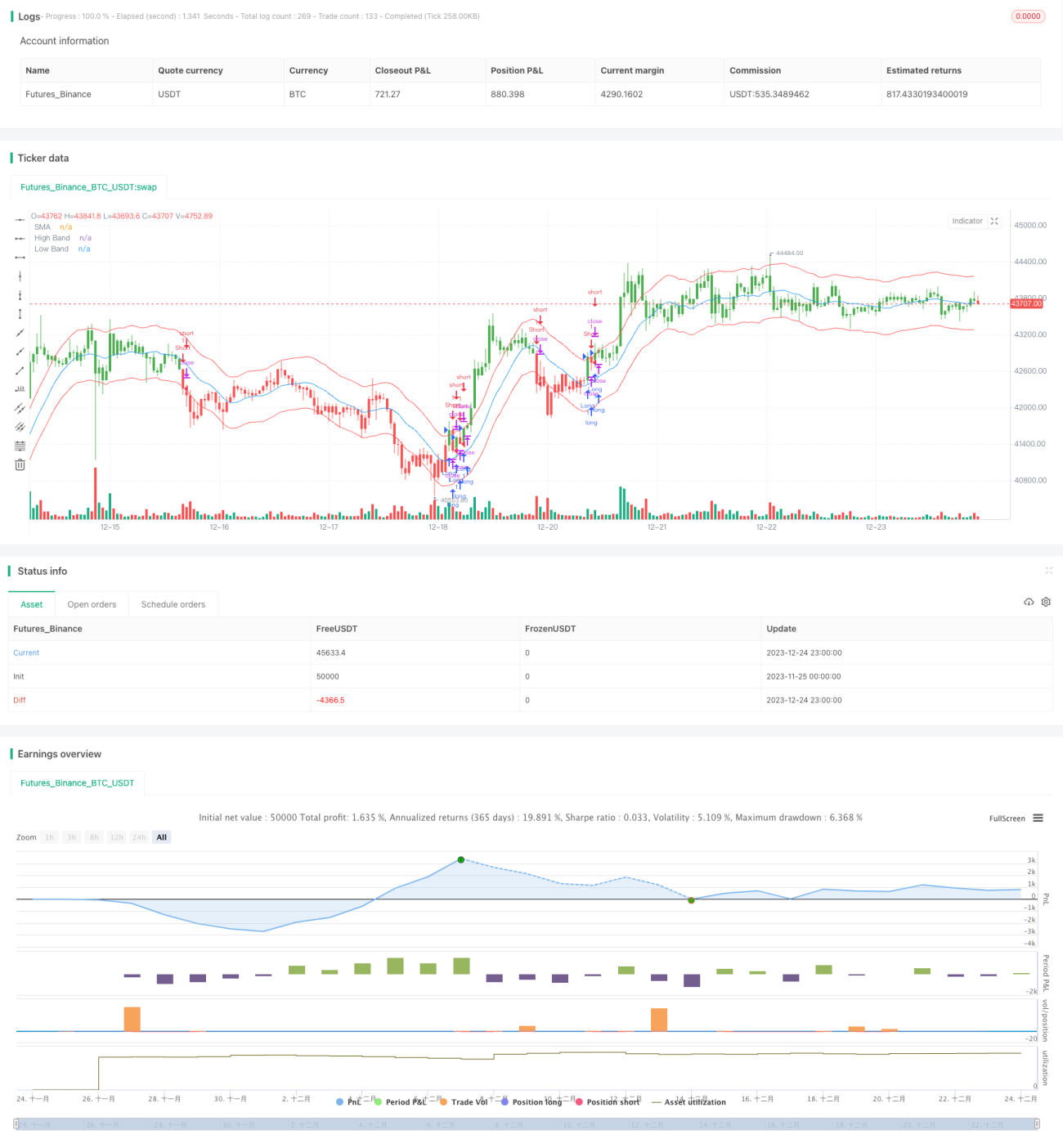

The strategy is based on a 14-period simple moving average (SMA). The upper envelope is calculated as: SMA + SMA × input percentage. The lower envelope is calculated as: SMA - SMA × input percentage. This forms up and down trading bands parallel to the SMA.

When close price goes above the upper band, a long position is taken. When close price goes below the lower band, a short position is taken. Otherwise, maintain a flat position. The input parameter "reverse" allows reverse trading.

The strategy uses 3 indicators:

-

xSMA - 14-period simple moving average, the midline.

-

xHighBand - Upper percentage envelope.

-

xLowBand - Lower percentage envelope.

Advantages

The advantages of this strategy include:

-

Simple logic, easy to understand and implement.

-

Can be used for both trend following and identifying overbought/oversold levels. Avoids missing trends in rangy markets.

-

Trade frequency can be controlled by adjusting the percentage envelopes parameters. Lowers trading risk.

-

Flexibility in choosing moving average periods for different timeframes and instruments.

-

The reverse input parameter adds flexibility. Can trade with or against the trend.

Risks and Solutions

There are some risks to the strategy:

-

Deep pullbacks beyond the envelope range can happen in strong trends, missing some profits. Can lower percentage parameters to control risk.

-

Frequent false signals may occur in choppy/ranging markets. Can increase moving average period to filter signals.

-

Too narrow envelopes may trigger excessive whipsaws. Can wisely widen envelope range.

-

Sudden volatility from news events can cause losses. Using stop loss helps manage risk.

Optimization

The strategy can be optimized:

-

Test moving averages of different periods and find optimal parameters with best signals.

-

Optimize percentage envelopes for maximum profitability and controllable risk.

-

Adding filters like MACD and KD to avoid bad signals in choppy/complex market conditions.

-

Combine with trend strength indicators like ADX to improve entry timing.

-

Test effectiveness across different instruments. Customize parameters per product.

-

Incorporate stop loss strategy to limit downside risk per trade.

Conclusion

Overall this is a typical trend following strategy with easy backtesting parameters. It can also identify overbought/oversold levels. Further parameter optimization and combination with other indicators can significantly improve its practical effectiveness for trading. This is a valuable strategy worthy of further research and application.

/*backtest

start: 2023-11-25 00:00:00

end: 2023-12-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 04/03/2018

// Moving Average Envelopes are percentage-based envelopes set above and - 1