Leveraged Position Sizing with Margin Call Risk Management Strategy

Overview

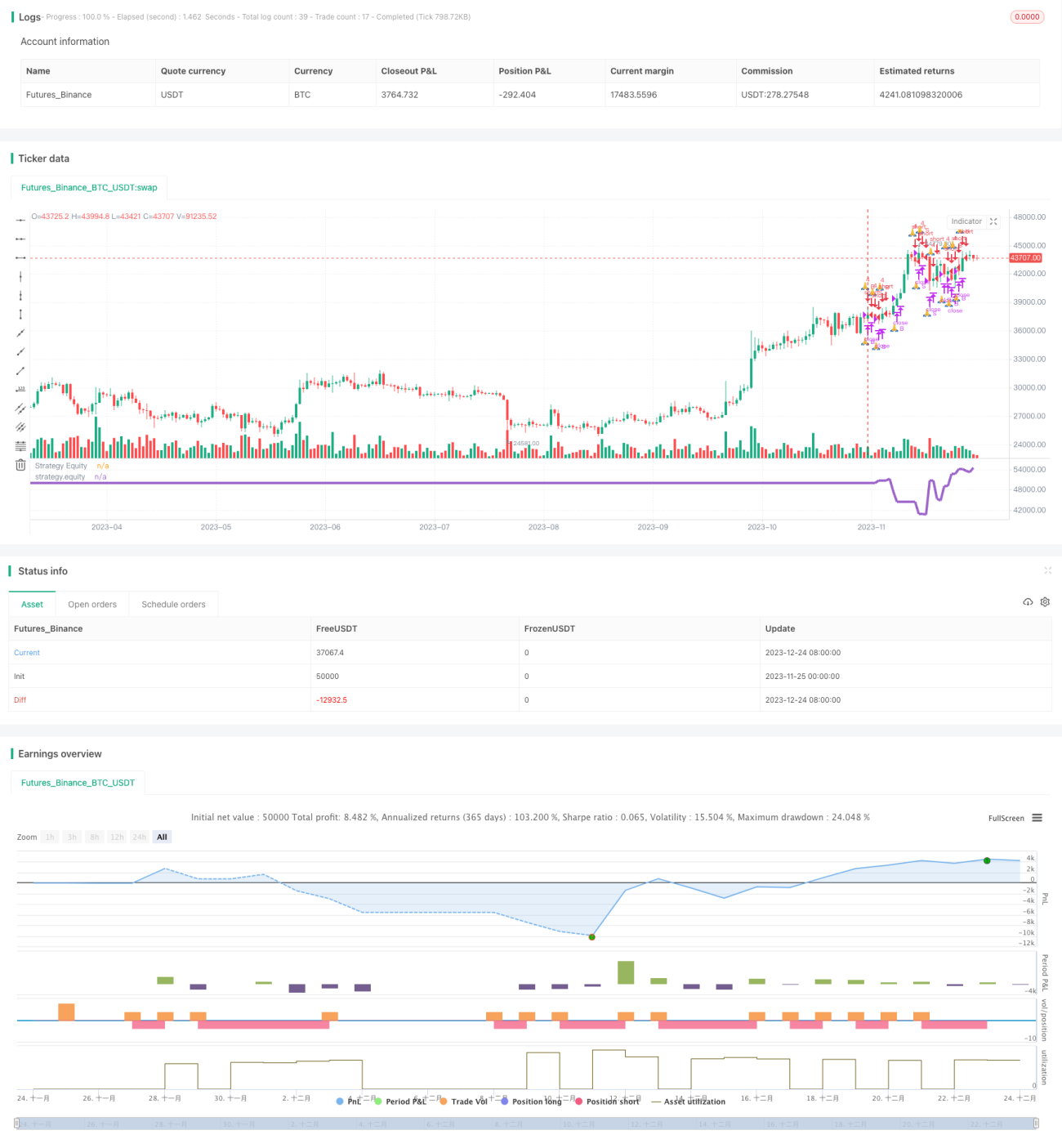

This strategy manages risk by setting high leverage and margin call conditions to close positions during significant market fluctuations.

Strategy Logic

- Set high leverage, e.g. 4x

- Define margin call level, e.g. $25,000

- Stop opening new trades when equity falls below margin call level

- Close all positions when margin call triggered as equity continues dropping

By doing so, the strategy can cut losses in time during drastic market moves to prevent margin call risks.

Advantages Analysis

- Flexible leverage customization based on personal risk tolerance

- Margin call mechanism prevents account blowups

- Timely stop loss with high leverage to mitigate risks

Risk Analysis

- Leverage amplifies both profits and risks

- Margin call level needs alignment with stop loss

- Stop loss subject to slippage risks

Risks can be reduced by adjusting leverage, aligning margin call and stop loss, optimizing stop loss, etc.

Optimization Directions

- Add trend filter to avoid counter-trend trades

- Optimize stop loss to prevent slippages

- Set trading hour filters to avoid trades in certain sessions

- Incorporate machine learning models to dynamically tune parameters

Summary

The strategy manages risk with leverage and margin call settings to prevent account blowups. However, high leverage also increases risks. Additional efforts like trend validation, stop loss optimization and trading hour control can help further reduce risks. Complex techniques like machine learning can also be leveraged to dynamically optimize parameters and strike a balance between profitability and risk management.

- 1