1

关注

1802

关注者

概述

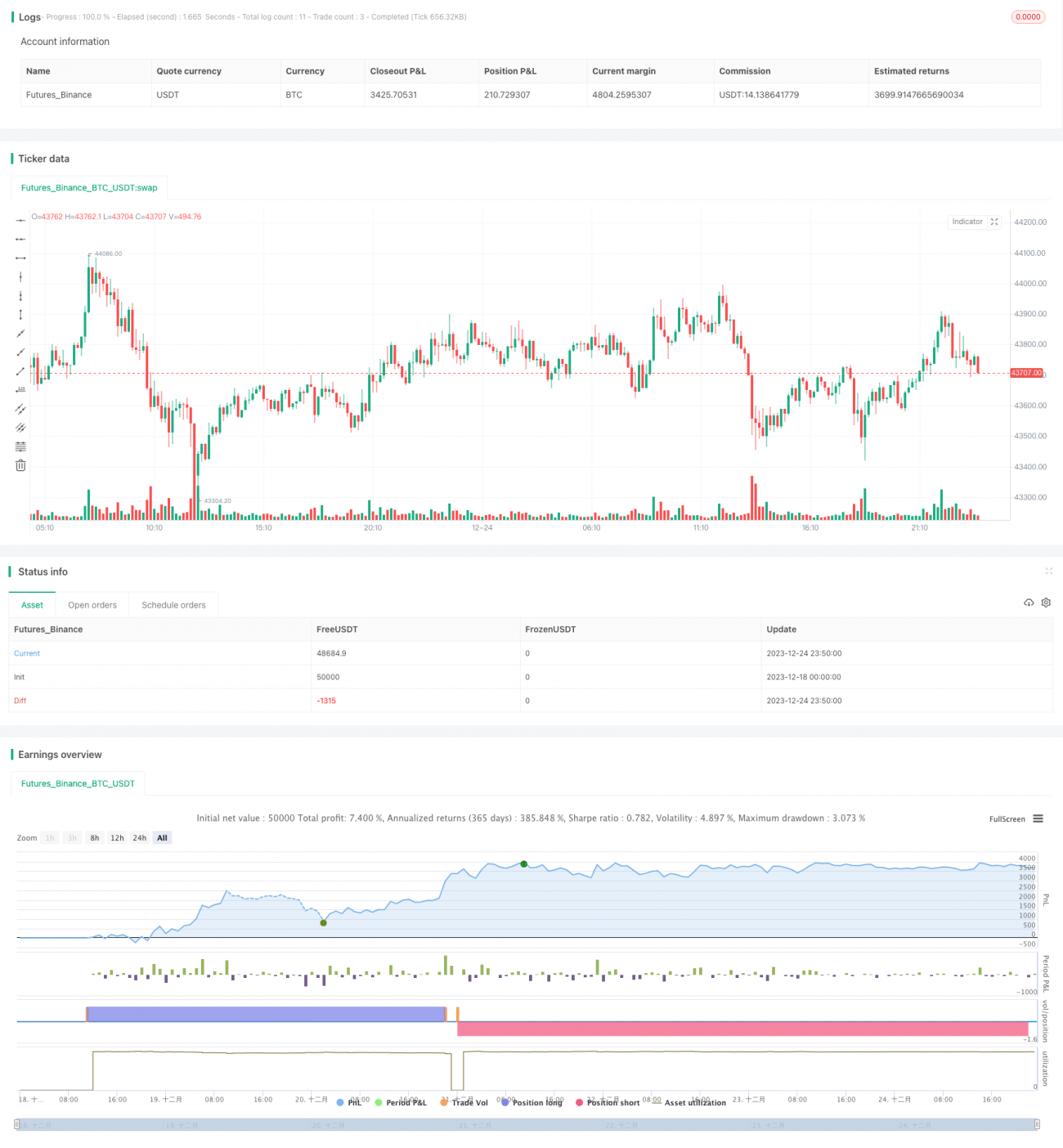

本策略名称为“黄金交叉芬奇策略”,其结合了移动平均线tech术指标MACD、相对强弱指标RSI以及黄金分割线原理中的斐波那契回撤/扩张理论,实现了对比特币等加密货币的量化交易。

策略原理

- MACD指标判断买卖点

- 设置MACD快线和慢线的EMA周期为15和30

- 判断快线上穿慢线为买点,下穿为卖点

- RSI指标过滤假信号

- 设置RSI的参数为50周期

- RSI指标可用来辅助过滤掉部分MACD给出的假信号

- 斐波那契理论确定SUPPORT/RESISTANCE

- 结合近期(如38根K线)的最高价和最低价

- 计算出黄金分割线的0.5斐波纳契回撤和扩张位

- 可用作支撑位和阻力位判断

- 均线和RSI判断超买超卖

- 50周期均线可判断目前是否处于超买超卖状态

- RSI指标也可判断超买超卖

- 反手开仓机制

- 给用户提供是否反手做单的选项

- 根据用户选择可灵活调整做多做空逻辑

优势分析

本策略最大优势在于可全天候运行,可大幅降低人工操作成本。另外,由多种指标组合可提高胜率,在牛市效果尤其明显。具体优势如下:

- 可7*24小时全自动量化交易,无需人工干预

- MACD指标判断买卖时机准确

- RSI指标可过滤掉部分假信号

- 斐波那契理论增加了交易决策依据

- 50均线和RSI判断超买超卖状态

- 可通过反手做单机制调整适应市场变化

风险分析

本策略也存在一些风险,主要来自于巨幅行情的反转,这时止损可能较难起到作用。此外,持仓时间过长也会存在一定风险。主要风险点如下:

- 止损距离过近,巨幅行情难以起到防护作用

- 持仓时间过长带来的系统性风险

对应解决方法如下:

- 适当放宽止损距离,保证止损充分起到作用

- 优化持仓周期,降低持仓时间过长的风险

优化方向

本策略主要可从以下几个方向进行优化:

- 优化MACD指标的参数,提高买卖信号准确率

- 优化RSI指标的参数,提高指标的实用性

- 测试更多周期的斐波那契理论取值

- 加入更多滤波指标,进一步降低假信号概率

- 结合更多大周期指标判断市场趋势

总结

本策略综合多个量化指标判断买卖时机,可全天候自动化交易加密货币市场。通过优化各指标参数和加入更多辅助指标,可望进一步提升策略盈利水平。该策略可为用户节省大量人工操作时间成本,值得量化交易者深入研究与应用。

策略源码

Pine

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1