Premium Double Trend Filter MA Ratio Strategy

Overview

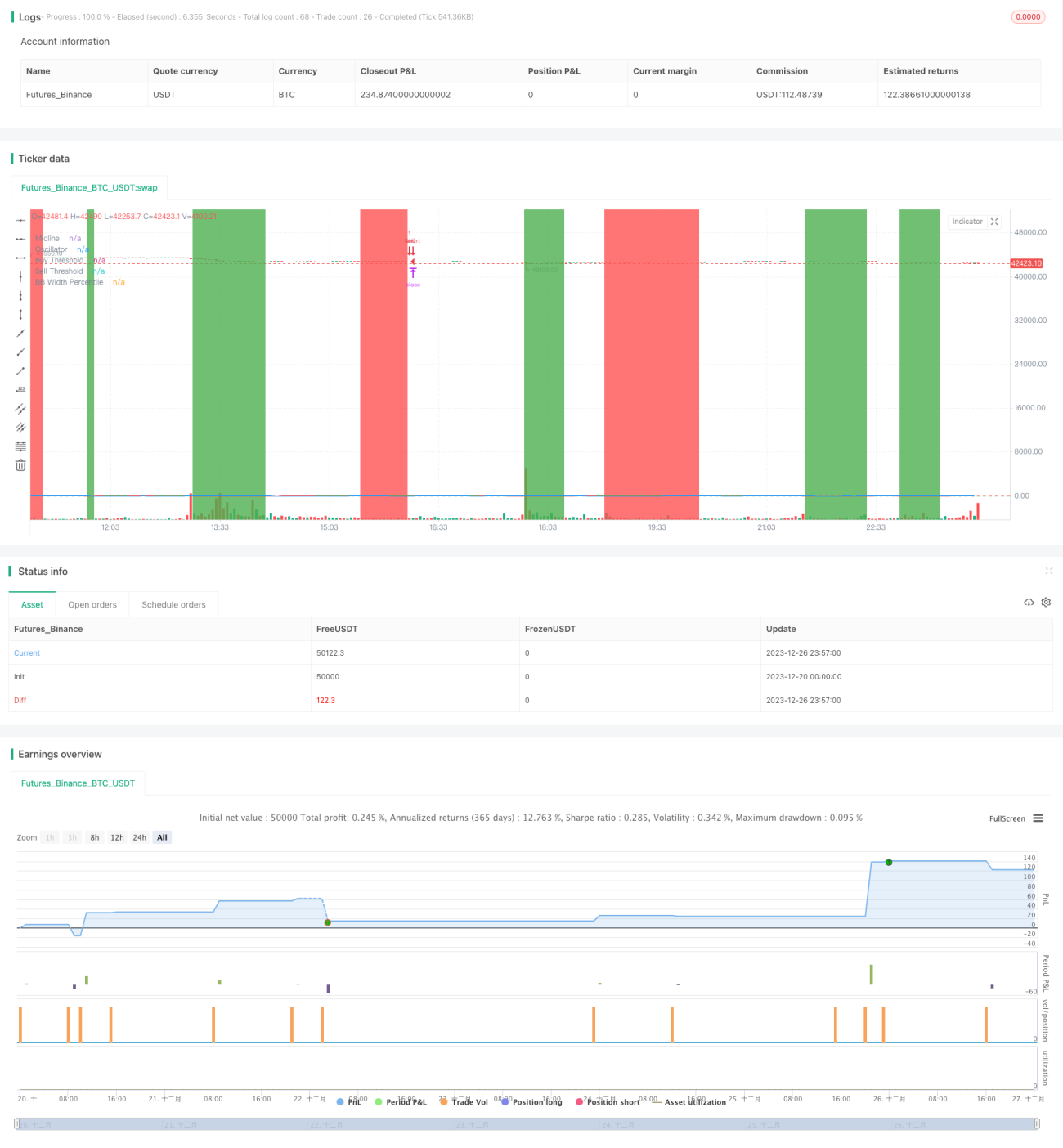

This strategy is based on double moving average ratio indicator combined with Bollinger Bands filter and double trend filter indicator. It adopts chained exit mechanisms for trend following. This strategy aims to identify mid-to-long term trend direction through moving average ratio indicator. It enters the market at better entry points when trend direction is clear. It also sets take profit, stop loss exit mechanisms to lock in profits and reduce losses.

Strategy Logic

- Calculate fast moving average (10-day) and slow moving average (50-day), get their ratio called price moving average ratio. This ratio can effectively identify mid-to-long term trend changes.

- Convert price moving average ratio into percentile, which represents relative strength of current ratio in past periods. This percentile is defined as oscillator.

- When oscillator crosses above buy entry threshold (10), long signal triggers. When crossing below sell threshold (90), short signal triggers for trend following.

- Combine with Bollinger Bands width index for signal filtering. Trade when BB width shrinks.

- Use double trend filter indicator, only taking long when price is in uptrend channel and short when in downtrend for avoiding reverse trading.

- Chain exit strategies are set, including take profit, stop loss, and combined exit. Multiple exit conditions can be preset with priority to maximum profit exit.

Advantages

- Double trend filter ensures reliability in identifying main trend, avoiding reverse trading.

- MA ratio indicator detects trend change better than single MA.

- BB width effectively locates low volatility periods for more reliable signals.

- Chained exit mechanism maximizes overall profit.

Risks and Solutions

- More false signals and reversals with unclear trend during ranging markets. Solution is to combine with BB width filter for tighter signals.

- MA has lagging effect, failing to detect trend reversal instantly. Solution is to shorten MA parameters properly.

- Stop loss may be hit instantly with price gaps, causing large loss. Solution is to loosely set stop loss parameter.

Optimization Directions

- Parameter optimization on MA periods, oscillator thresholds, BB parameters through exhaustive tests to find best combination.

- Incorporate other indicators judging trend reversal like KD, MACD to improve accuracy.

- Machine learning model training with historical data for dynamic parameter optimization.

Summary

This strategy integrates double MA ratio indicator and BB to determine mid-to-long term trend. It enters Market at best point after trend confirmation with chained profit-taking mechanisms. It is highly reliable and efficient. Further improvements can be achieved through parameter optimization, adding trend reversal indicators and machine learning.

- 1