Quantitative Trading Reversal Trend Combo T3-CCI Strategy

Overview

This strategy combines the use of reversal trend strategy and T3-CCI indicator to generate trading signals at market reversal points. It belongs to short-term quantitative trading strategies.

Strategy Principle

-

Reversal Trend Strategy Part: Use 2-day close price comparison to judge price reversal signals, combined with 9-day slow K-line indicator to determine overbought and oversold areas, and generate long and short signals.

-

T3-CCI Part: Use T3 moving average to resmooth the CCI indicator to reduce false signals and determine overbought and oversold areas. It is used together with the reversal trend strategy to filter entry timing.

The final trading direction is determined by the integrated signals from both parts.

Advantage Analysis

-

Using two types of indicators and price comparisons can effectively identify potential reversal points.

-

The application of T3 moving average improves the quality of CCI signals and reduces false signals.

-

The combined use of different types of strategies can be expected to improve the overall stability of the strategy.

Risk Analysis

-

In case of reversal failure, it will generate wrong signals and losses. Timely stop loss is required to control risks.

-

Improper parameter settings will also affect strategy performance. Parameters need to be adjusted according to different markets.

-

Reversal signals have poor timeliness and cannot capture rapid reversals in time.

Optimization Directions

-

Increase trend filtering to avoid losses caused by reversal failures.

-

Try machine learning methods to automatically optimize parameters.

-

Increase stop loss mechanism.

-

Explore more efficient indicators to judge reversal timing.

Summary

This strategy combines multiple technical indicators to judge potential reversal points. It can effectively tap market reversal opportunities and is suitable for short-term operations. Through measures such as parameter adjustment, stop loss protection, combination with trend judgment and other optimization methods, the stability of the strategy can be further enhanced.

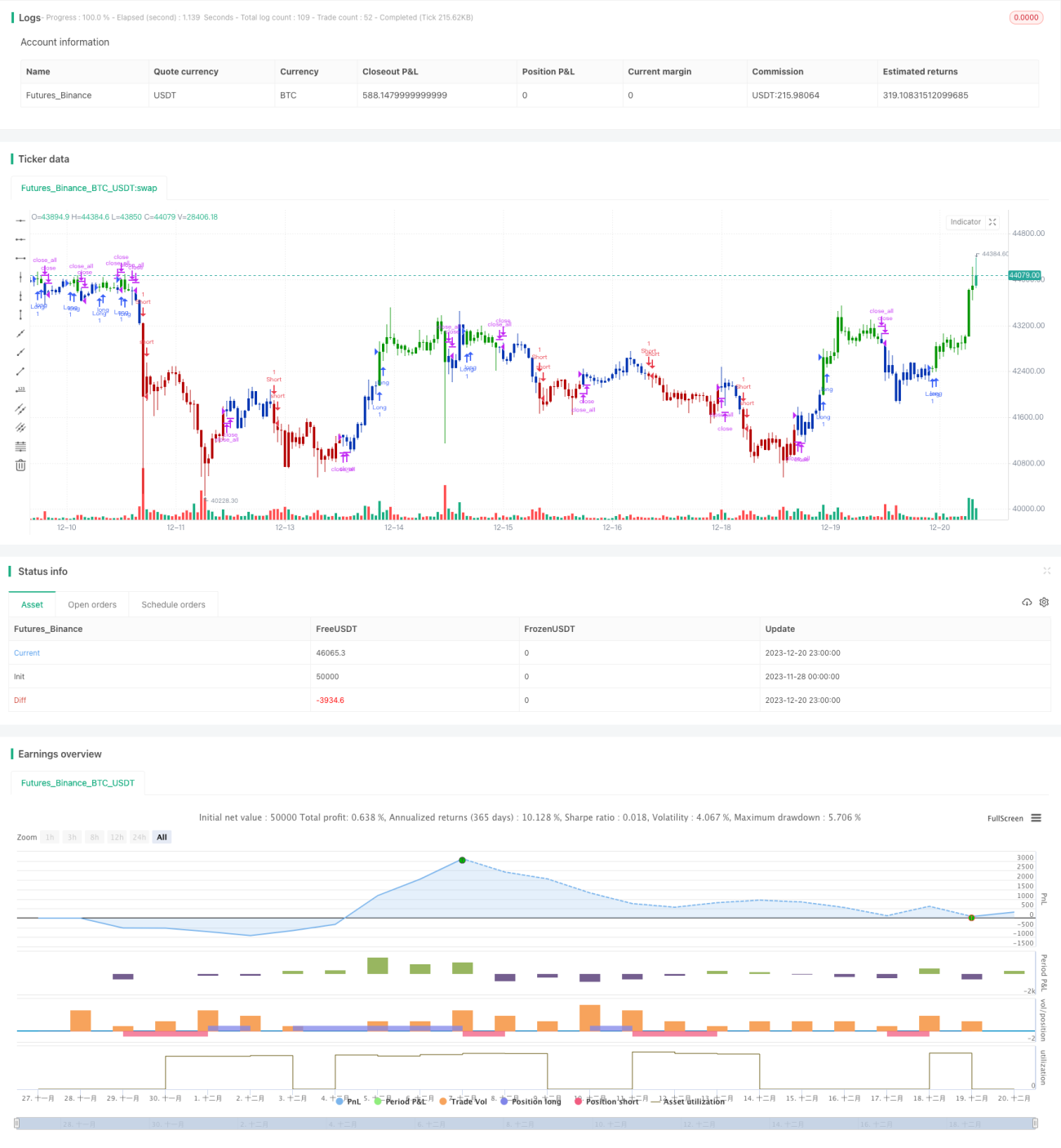

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 23/10/2020

// This is combo strategies for get a cumulative signal. - 1