Quant Strategy Based on Linear Regression Intercept

Overview

This strategy uses linear regression techniques to calculate the linear regression intercept and uses it as a trading signal to construct a quantitative trading strategy. By analyzing the price time series of stocks, this strategy fits a linear regression trend line and uses the linear regression intercept to judge whether prices are overestimated or underestimated, thereby generating trading signals.

Strategy Principle

The linear regression intercept indicates the predicted value of Y (usually the price) when the time series value X is 0. This strategy presets the parameter Length, takes the closing price as the source sequence, and calculates the linear regression intercept (xLRI) of the most recent Length days. When the closing price is higher than xLRI, go long; when the closing price is lower than xLRI, go short.

The specific calculation formula is as follows:

xX = Length *(Length - 1)* 0.5

xDivisor = xX *xX - Length* Length *(Length - 1) *(2 * Length - 1) / 6

xXY = Σ(i *Closing Price[i]), i from 0 to Length-1

xSlope = (Length *xXY - xX* Σ(Closing Price, Length))/ xDivisor

xLRI = (Σ(Closing Price, Length) - xSlope * xX) / Length

Through such calculations, the linear regression intercept xLRI for the most recent Length days can be obtained. The strategy judges the price highs and lows based on it to generate trading signals.

Advantages

This strategy has the following advantages:

- Using linear regression techniques, it has certain predictive and trend judgment capabilities for prices.

- Fewer parameters, simpler model, easy to understand and implement.

- Customizable parameter Length to adjust strategy flexibility.

Risks and Solutions

This strategy also has some risks:

- Linear regression fitting is merely a statistical fitting based on historical data, with limited ability to predict future price trends.

- If the company's fundamentals undergo major changes, the results of linear regression fitting may become invalid.

- Improper setting of the parameter Length may lead to overfitting.

Countermeasures:

- Appropriately shorten the parameter Length to prevent overfitting.

- Pay attention to changes in the company's fundamentals and intervene manually to close positions when necessary.

- Adopt adaptive parameter Length to dynamically adjust according to market conditions.

Optimization Directions

This strategy can also be optimized in the following aspects:

- Add a stop loss mechanism to control single loss.

- Combine with other indicators to form a combination strategy to improve stability.

- Add parameter self-adaptive optimization module to make Length parameter change dynamically.

- Add a position control module to prevent over-trading.

Summary

This strategy constructs a simple quantitative trading strategy based on the linear regression intercept. Overall, the strategy has some economic value, but there are also some risks to note. Through continuous optimization, it is expected to further improve the stability and profitability of the strategy.

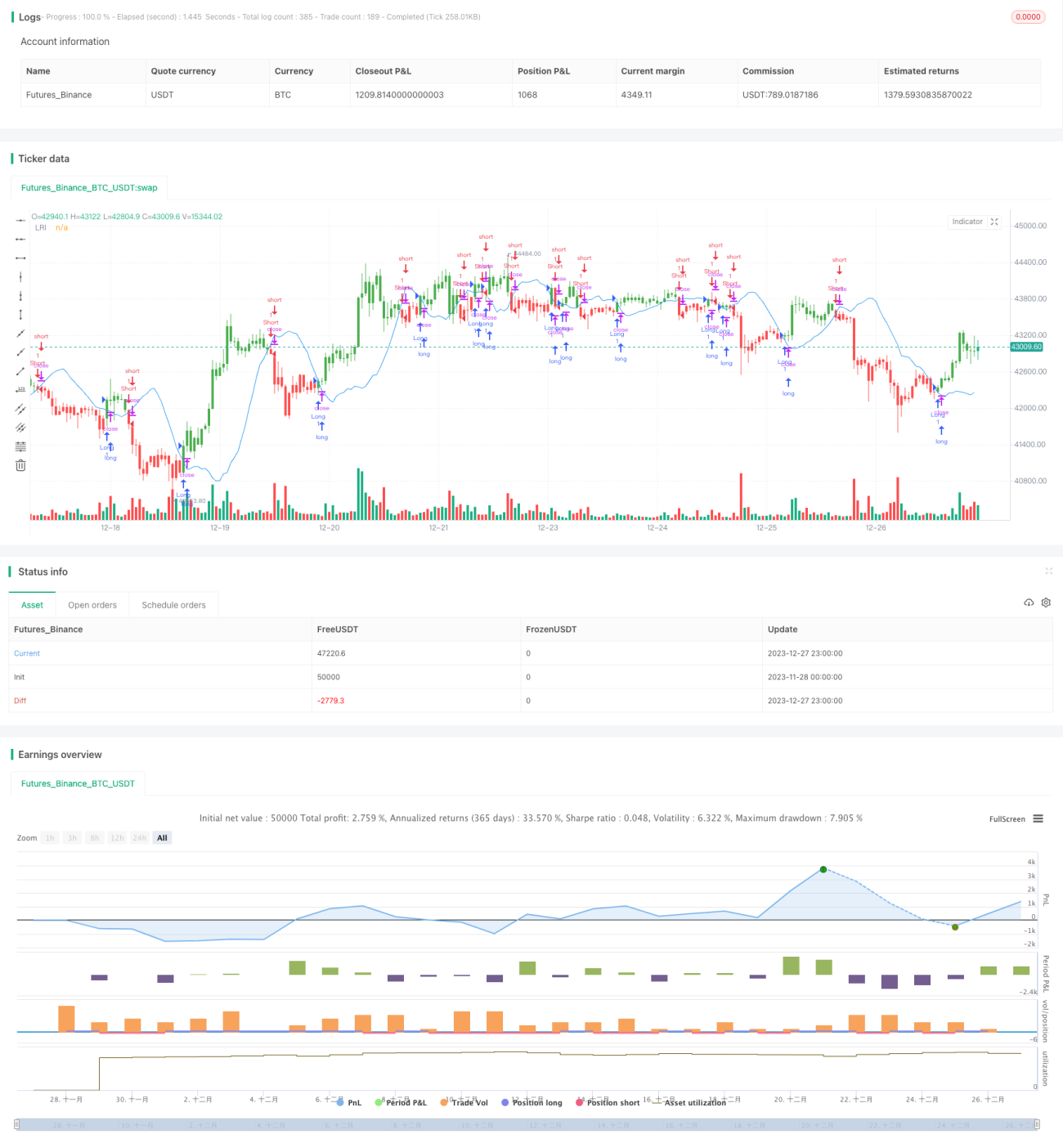

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 21/03/2018

// Linear Regression Intercept is one of the indicators calculated by using the - 1