Trend Reversal Momentum Indicators Crossover Tracking Strategy

Overview

This strategy combines MACD, RSI, ADX and other momentum technical indicators to identify price reversal signals and adopt reverse strategies to enter when the strong trend reverses. The strategy also sets stop loss and take profit to lock in profits and control risks.

Strategy Principle

This strategy first combines MACD indicator's fast and slow moving average crossovers to judge price trends; then uses RSI indicator to filter false breakouts and ensure that trading signals are generated only after actual price reversals occur; finally utilizes ADX indicator to verify again whether prices have entered a trending state. Trading signals are generated only when all the above conditions are met simultaneously.

Specifically, when MACD fast line crosses above slow line, RSI is higher than 50 and rising, ADX is greater than 20, it is a buy signal; when MACD fast line crosses below slow line, RSI is lower than 50 and falling, ADX is greater than 20, it is a sell signal.

Advantage Analysis

The biggest advantage of this strategy is that it combines multiple indicators to effectively filter whipsaws and erroneous signals, truly locking the inflection points of trend reversals, thus obtaining a higher win rate. In addition, setting stop loss and take profit locks in profits and controls risks, which can effectively hedge the impact of unexpected events.

Risk Analysis

The biggest risk of this strategy is the misjudgment of trend reversal, such as price making a deep retracement resulting in misjudgment. In addition, the sustainability of the new trend after reversal may not be sufficient to make enough profit.

The solutions are to further optimize parameters, adjust stop loss margin, or incorporate more auxiliary indicators for signal filtering.

Optimization Directions

This strategy can be further optimized in the following directions:

-

Optimize the combination of MACD and RSI parameters to improve the accuracy of price reversal judgments;

-

Increase more indicators filtering, such as KD, BOLL etc, to form the effect of indicators encompassing each other;

-

Dynamically adjust stop loss margin according to different market conditions;

-

Modify take profit position in real time according to the actual trend after reversal.

Summary

This strategy combines multiple momentum indicators to identify potential price reversal opportunities. Through parameter optimization, incorporating more auxiliary indicators, dynamically adjusting stop loss and take profit strategies, the stability and reliability of the strategy can be further improved to lock the various trading opportunities provided by the markets.

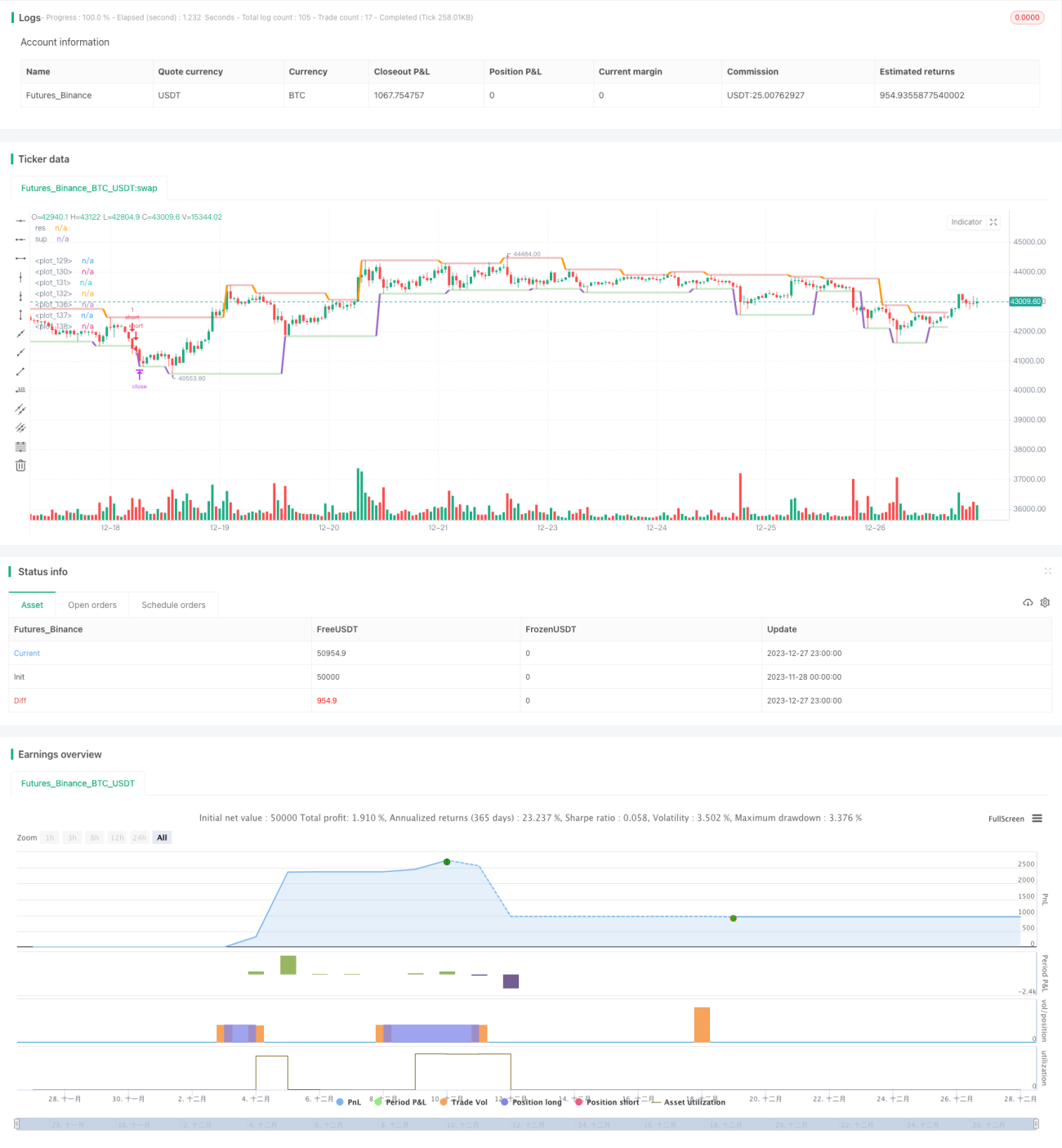

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AHMEDABDELAZIZZIZO

//@version=5- 1