Momentum Tracking Strategy

Overview

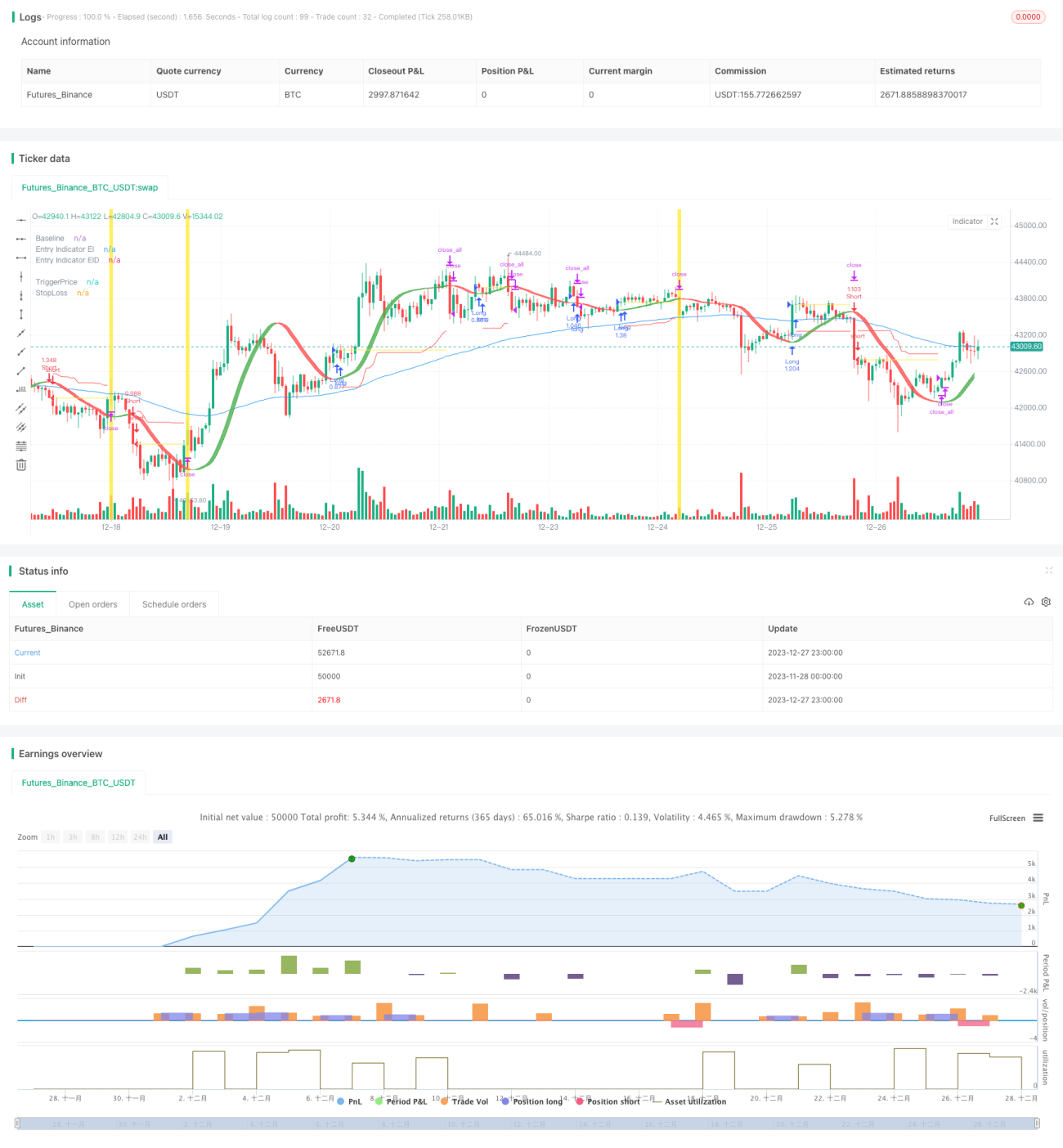

The Momentum Tracking strategy uses the Hull Moving Average as the main indicator to determine the price trend direction. At the same time, the strategy incorporates other indicators such as baseline, confirmation indicator, etc. to verify the price trend and filter false signals. After entering the market, the strategy uses the Average True Range to calculate the dynamic stop loss to track trends for profit.

Strategy Principle

The core of the Momentum Tracking strategy is the Hull Moving Average. The Hull Moving Average is more sensitive to price changes and can effectively determine the trend direction. When the price breaks through the Hull line upwards, an upward trend is confirmed, going long; when the price breaks through the Hull line downwards, a downward trend is confirmed, going short.

In addition, the strategy also introduces a baseline indicator to judge short and long term trends; a confirmation indicator is used to filter false breakouts. A trading signal will only be triggered when both the baseline and the confirmation indicator have verified the trend direction.

After entering the market, the strategy uses the average true range and Hull EMA to set the stop loss position. As the trend continues, the stop loss line will continue to move up/down to lock in trend profits.

Advantage Analysis

The Momentum Tracking strategy combines the advantages of trend judgment and risk control, which can obtain good returns in trending markets. Compared with fixed stop loss strategies, it can track trend runs by moving stop losses and avoid being stopped out by normal market fluctuations.

The combination of multiple indicators also makes the strategy more sensitive to market changes, while effectively filtering out false signals. In addition, the strategy also provides multiple adjustable parameters for users to optimize based on their own market judgment.

Risk Analysis

The strategy relies mainly on trend indicators and is prone to generating wrong signals and stop losses during consolidations. In addition, the combination of multiple indicators can also lead to conflicts between indicators. Improper parameter settings can also lead to poor strategy performance.

Consider adding an additional judgment module in the strategy to pause trading when indicators show divergence; or adopt a voting mechanism to synthesize the judgement results of multiple indicators. For parameter settings, the optimal parameters can be found through backtest optimization methods.

Optimization Directions

The Momentum Tracking strategy can be optimized in the following directions:

- Increase judgment modules, such as volatility module, pause trading when volatility is high;

- Increase machine learning module, use machine learning algorithms to determine indicator weights;

- Optimize indicator parameters to find the best parameter combination;

- Optimize the moving stop loss algorithm to better track the trend;

- Add risk management modules such as trailing stop loss, dynamic position adjustment, etc.

Summary

In summary, the Momentum Tracking strategy is an excellent trend tracking strategy. It successfully combines trend judgment and dynamic stop loss, which can effectively track and profit from trends. With further optimization, it is expected to achieve better strategy performance. The strategy provides a good reference for the construction of quantitative trading strategies.

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1