Dual Reversal High-Low Strategy

Overview

The Dual Reversal High-Low strategy is a quantitative strategy that combines dual signals. It integrates a reversal-based intraday strategy and a trend judgment strategy that utilizes the difference between yesterday's highest price and a moving average. The strategy aims to achieve more stable buy and sell signals to further avoid the issuance of incorrect signals.

Principles

First, the reversal strategy part. This strategy judges the formation of signals when there is a reversal in the closing price for two consecutive days, while combining the judgment of overbought and oversold states using the stochastic indicator. Specifically, it is a sell signal when the closing price changes from rising to falling for two consecutive days, and the fast stochastic indicator is above the slow stochastic indicator; it is a buy signal when the closing price changes from falling to rising for two consecutive days, and the fast stochastic indicator is below the slow stochastic indicator.

Second, the high-low strategy part. This strategy uses the difference between yesterday's highest price and a 13-period exponential moving average to determine the trend. It generates a buy signal when the highest price is above the moving average; it generates a sell signal when the highest price is below the moving average.

Finally, this strategy integrates the two signals. It takes a buy action when both signals show a buy signal at the same time; it takes a sell action when both signals show a sell signal at the same time.

Advantages

This dual signal strategy can effectively reduce incorrect signals and unnecessary trades. The reversal part can determine overbought and oversold conditions to avoid chasing highs and selling lows. The high-low part can determine price trend divergences to avoid false breakouts. When combining the judgments, actual trading signals are only generated when the dual signals are in the same direction, which can significantly improve the reliability of the signals and reduce ineffective trades.

In addition, the reversal and the high-low parts use different types of indicators and judgment criteria, so they can serve to validate each other and further reduce incorrect signals. When special situations occur in the market, a single indicator is prone to incorrect signals, while combined judgments can offset some errors. This kind of multi-indicator integrated judgment strategy can obtain more reliable and stable trading signals.

Risk Analysis

The biggest risk of this strategy is that sustained reasonable one-sided signals may be ignored in a strong trending market. When the trend is very obvious, the signal judgment of the reversal part may be wrong, which will cause the one-sided signals in the high-low part to fail to be executed as trades. This is especially prominent in trending bull and bear markets.

In addition, improper parameter settings can also affect the strategy. The parameter settings in the reversal part need to take into account the cycle moving average system, and the moving average period in the high-low part needs to be coordinated. If the periods of both are improper, there will be mediocre false signals or simply no signals.

Optimization

First, the length parameter of the moving average in the high-low part can be tested to make it more coordinated with the cycle indicators in the reversal part. The current 13-period indicator in the high-low part may be too sensitive, and trying longer periods may obtain more stable judgments.

Second, the reversal part can also test using K-line entities instead of using only the closing price which is easily influenced. Considering that a reversal of a larger real body K-line may have a stronger signal effect.

Finally, it can also try to only consider taking trades when reversal signals appear during the session, as the current intraday holding method has higher risks. Changing to adopt temporary reversal trading can avoid some holding risks.

Conclusion

The dual reversal high-low strategy integrates signals from multiple indicators and conducts dual verification before issuing buy and sell signals. This strict signal filtering mechanism can effectively reduce the impact of invalid and incorrect signals on actual trading. The strategy successfully controls the frequency of ineffective trades, making each trade more reliable, and avoids blindly following short-term market moves. Through parameter optimization, it may achieve better performance in certain markets.

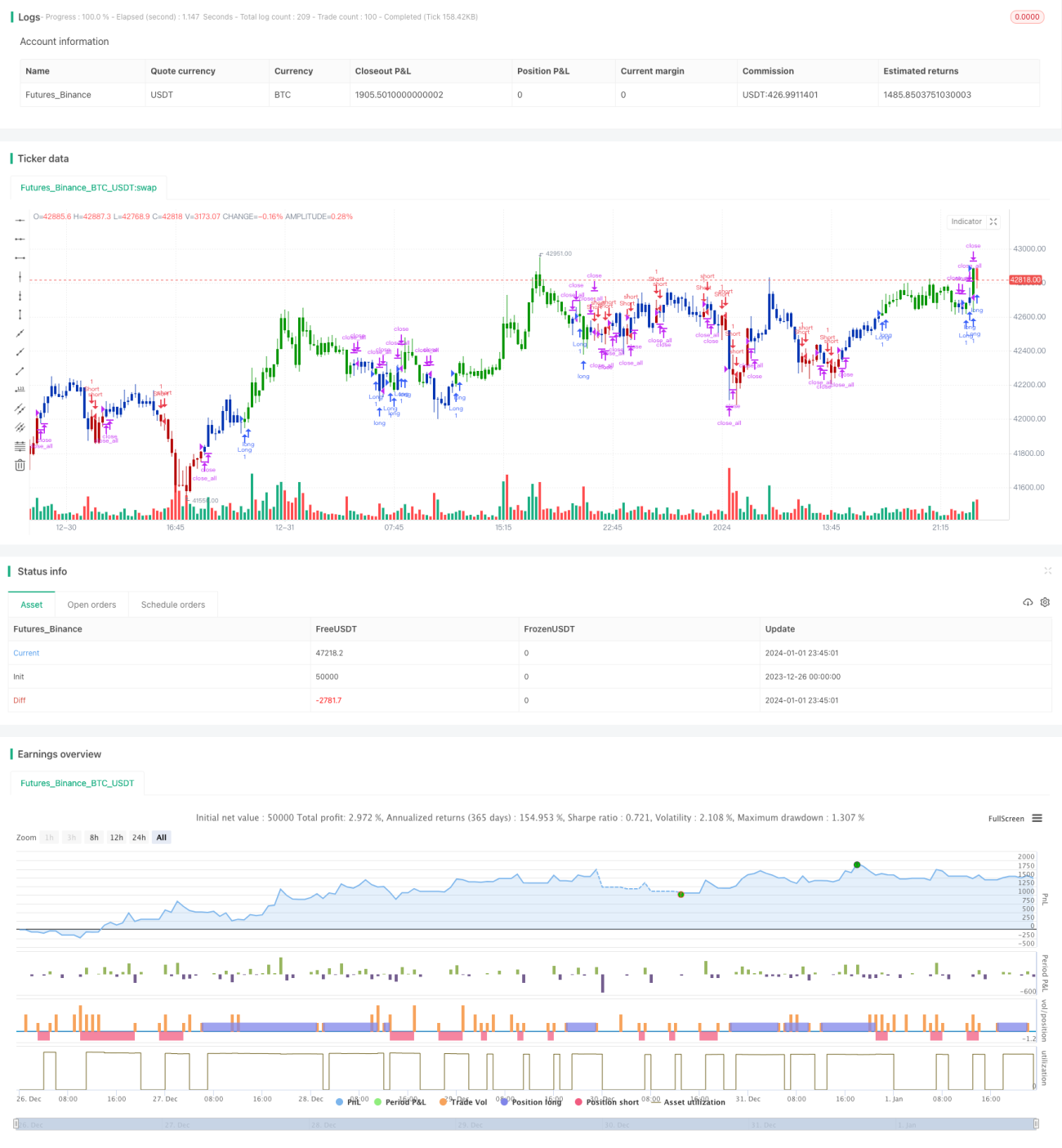

/*backtest

start: 2023-12-26 00:00:00

end: 2024-01-02 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 23/11/2020

// This is combo strategies for get a cumulative signal. - 1