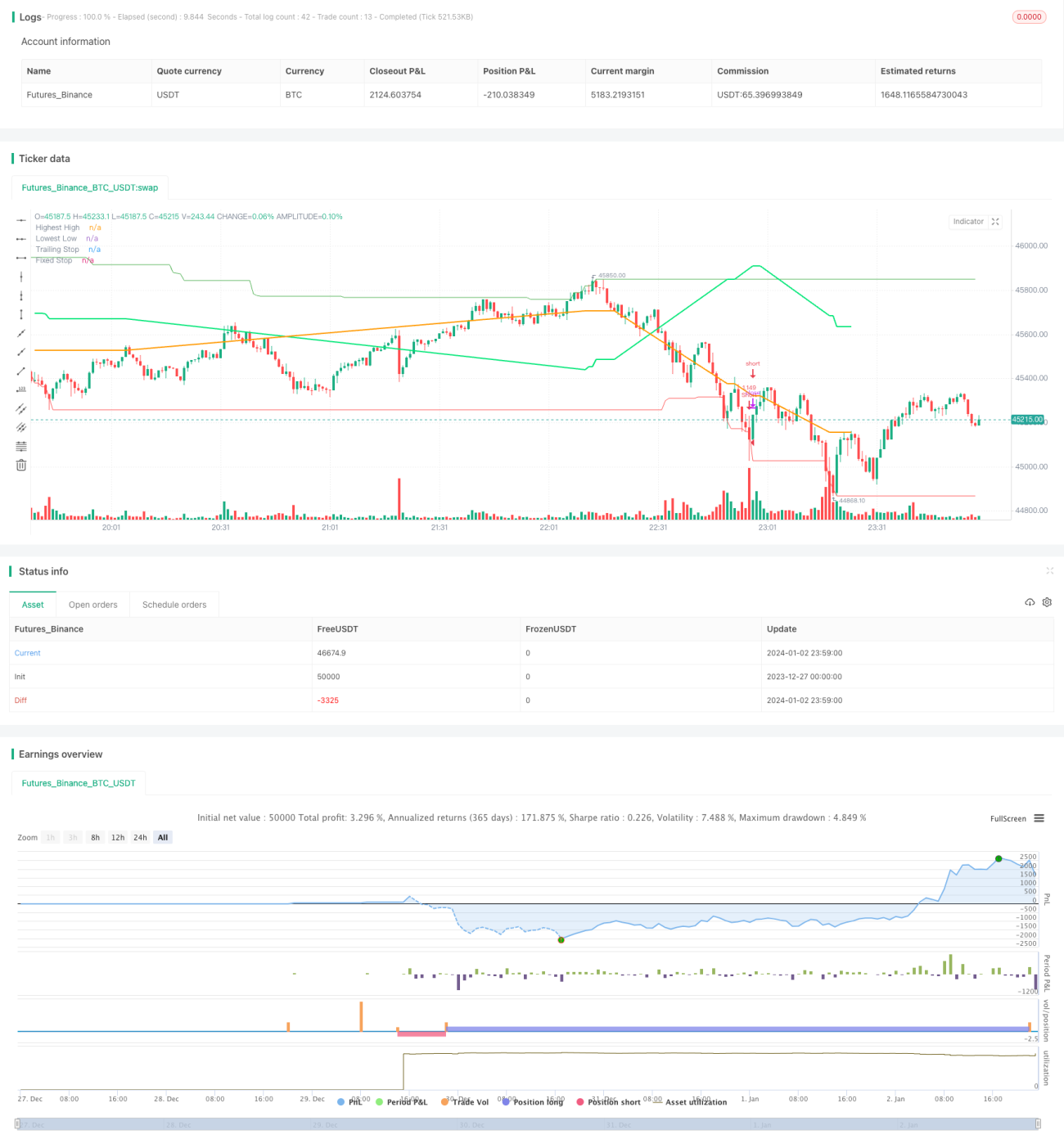

概述

双趋势震荡策略是一种结合趋势和震荡的量化交易策略。它利用两个指标的组合来识别趋势的方向和力度,并在趋势震荡的时候寻找较好的入场时机。

策略原理

该策略主要利用了两个公开指标:Trend Surfers和Mawreez's Trend Oscillator。

Trend Surfers是一个趋势跟踪止损指标。它通过计算一定周期内的最高价和最低价,来判断价格走势并给出建议的止损位置。比如,当价格突破最近168根K线的最高价时,就是看涨信号;当价格跌破最近168根K线的最低价时,就是看跌信号。

Mawreez's Trend Oscillator则是一个双线震荡指标。它类似MACD,通过DI的差值来判断趋势的方向和力度。该指标曲线在0轴以上为看涨,以下为看跌。

该策略的交易规则是:

多头入场:Trend Surfers突破最高线和Mawreez's Trend Oscillator指标为看涨时买入

空头入场:Trend Surfers跌破最低线和Mawreez's Trend Oscillator指标为看跌时卖出

止损方式为趋势跟踪止损加固定止损。

优势分析

该策略结合了趋势和震荡指标,既可以捕捉趋势,也可以在震荡中寻找较好价格入场,具有以下优势:

- 双重指标过滤,可以有效避免假突破

- 结合趋势和震荡,容易抓住价格在震荡区间中的低位吸筹布局或高位轻装上阵

- 采用多重止损方式,可以很好控制风险

风险分析

该策略也存在一些风险:

- 双重指标组合,容易漏单

- 趋势指标和震荡指标可能会发出冲突信号

- 固定止损可能会过早止损

针对这些风险,可以采取以下措施加以规避:

- 适当宽松指标参数,降低滤波率

- 增加趋势判断规则,避免指标冲突

- 动态调整止损位置

优化方向

该策略还有进一步优化的空间:

- 测试不同参数组合和周期参数,寻找最佳参数

- 增加波动率、交易量等辅助判断规则

- 采用机器学习技术动态优化指标和参数

总结

双趋势震荡策略综合运用趋势跟踪和震荡指标的优点,既可以识别趋势方向,又可以把握震荡机会,通过参数和规则优化,可以将策略盈利能力进一步提升。该策略有良好的发展前景。

策略源码

Pine

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1