Trend Following Moving Average Trading Strategy

Overview

This strategy is a trend following moving average trading strategy. It uses moving averages of highest and lowest prices with different parameter settings to determine market trends and generate trading signals at turning points. It goes long when price breaks above the upward-tracking moving average line and goes short when price breaks below the downward-tracking line. The strategy also utilizes ATR to set stop loss and take profit levels.

Strategy Logic

The strategy employs simple moving averages of highest and lowest prices with different parameters to define market trends. Specifically, it creates two sets of tracking moving average systems:

-

The h1 and l1 system tracks the trend from upside. h1 is the simple moving average of highest prices, acting as the upper band of the trend; l1 is constructed by h1 minus the ATR value, serving as the lower band. A long signal is generated when price breaks above h1, and a close signal is generated when price falls below l1.

-

The h2 and l2 system tracks the trend from downside. h2 is the simple moving average of lowest prices, acting as the lower band; l2 is constructed by h2 plus the ATR value, serving as the upper band. A short signal is generated when price breaks below h2, and a close signal is generated when price rises above l2.

The dual-band systems can more accurately identify trend turning points and filter out some noisy trades. Meanwhile, the ATR value is used to set stop loss and take profit levels to control risk-reward ratio per trade.

Advantage Analysis

The main advantages of this strategy include:

- The dual-band system filters noise and identifies turning points more precisely.

- ATR dynamically tracks volatility, enabling effective per trade stop loss control.

- The logic is simple and easy to understand, suitable for beginners to learn.

- Parameters can be flexibly tuned for adapting to different market environments.

Risk Analysis

There are also some risks associated with this strategy:

- Breakout signals from the bands could lag, missing opportunities at early trend stages.

- Tracking moving averages have weaker ability in catching curved trends.

- Trading costs are not considered. They could be high with high frequency trading.

Solutions:

- Shorten moving average periods for more sensitive signals.

- Incorporate other indicators like MACD to determine trend types, avoiding over-trading in ranging zones.

- Adjust position sizing to lower trading frequency.

Optimization Directions

The strategy can be optimized from the following aspects:

- Utilize machine learning algorithms to auto-tune parameters for adapting to changing markets.

- Incorporate trading volume to avoid false breakouts.

- Add micro position sizing rules to link position size with trend strength.

- Optimize stop loss mechanisms with trailing stops etc.

Conclusion

In conclusion, this is a simple and practical trend following strategy. The core philosophy is to identify trend turning points and control per trade loss through dual-band filtering and dynamic ATR stops. It has definite practical merits and also large room for optimization. Better performances could be achieved through parameter tuning, incorporating other indicators etc.

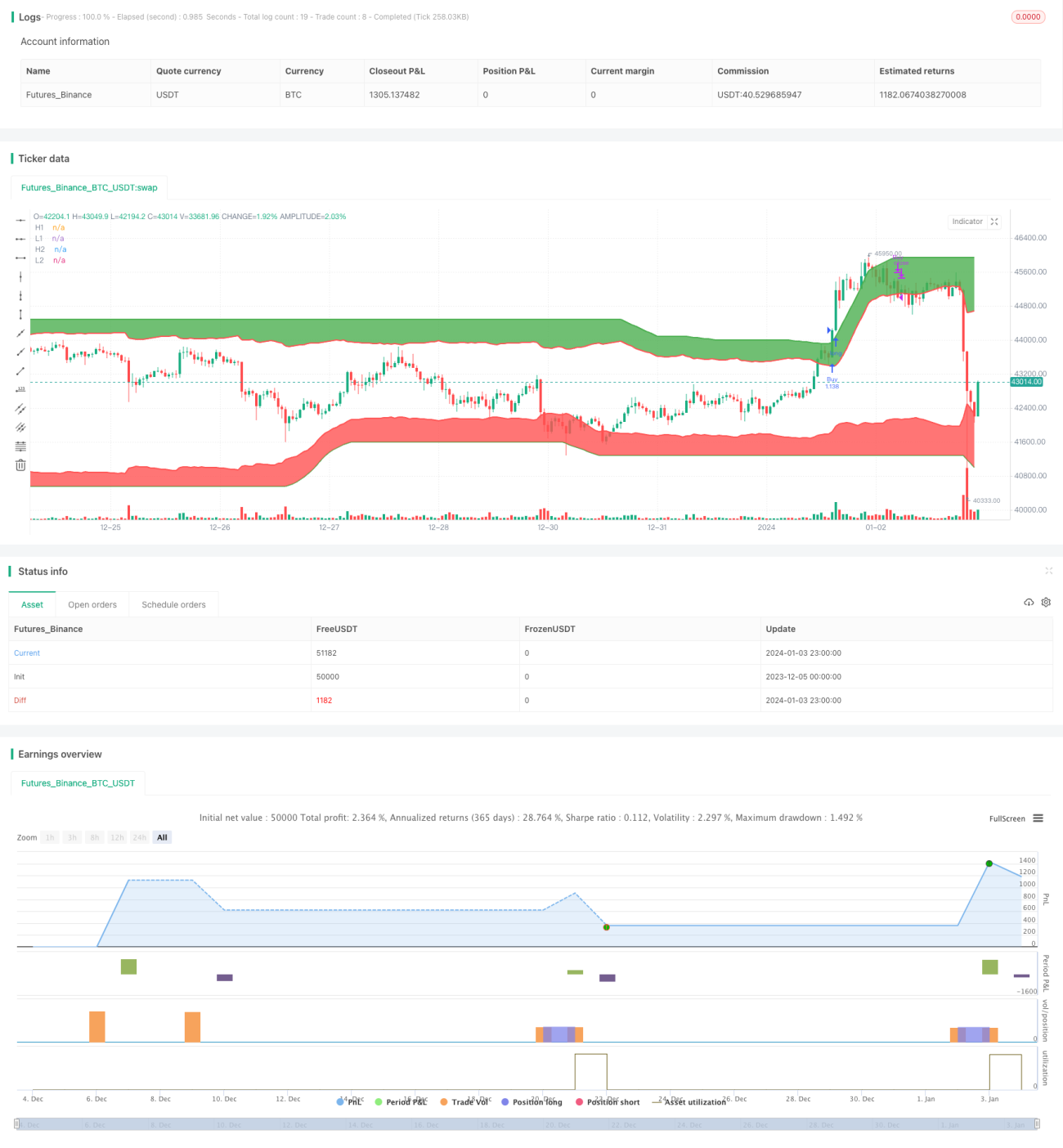

/*backtest

start: 2023-12-05 00:00:00

end: 2024-01-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("I Like Winners And Love Loosers!", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

highest_length = input(200, type=input.integer, minval=1, title="Highest Length")- 1