Reversal Momentum Compound Strategy

Overview

The Reversal Momentum Compound strategy combines a reversal strategy and a momentum strategy. By utilizing both price reversal signals and momentum indicator signals, it captures market turning points more precisely and gets in the market in a timely manner as price starts to reverse.

Strategy Logic

The strategy consists of two parts:

-

123 Reversal Strategy: Go long when close is higher than previous close for 2 consecutive days after 2 days of lower close, and 9-day slow K line is below 50; Go short when close is lower than previous close for 2 consecutive days after 2 days of higher close, and 9-day fast K line is above 50.

-

DAPD Momentum Breakout Strategy: DAPD is the average difference between 21-day high and 21-day low. Determine entry and exit points based on DAPD breakout.

A entry signal is generated when two strategies give aligned signals. Stay sideline when signals are conflicting.

Advantages

The strategy combines the merits of reversal and momentum strategies, capturing turning points more precisely. Main advantages:

-

Dual filter increases signal reliability. Higher success rate when signals align.

-

123 pattern reduces risk of whipsaws.

-

DAPD momentum suitable for trending products.

Risks

-

Signal timing mismatch risk. Signals from two strategies may not align perfectly.

-

Parameter tuning difficulty. Hard to optimize two sets of parameters together.

-

Doubled transaction cost risk. Commission fees apply to both strategies.

Optimization

-

Optimize signal alignment of two strategies.

-

Test effectiveness of different parameter sets on different products.

-

Only take high-conviction signals to filter out weak ones.

Conclusion

The Reversal Momentum Compound strategy captures reversing price timely by combining merits of reversal and momentum strategies. Dual filters increase success rate. Further performance improvement can be achieved by optimizing signal alignment. The strategy suits investors with sufficient capital and trading expertise.

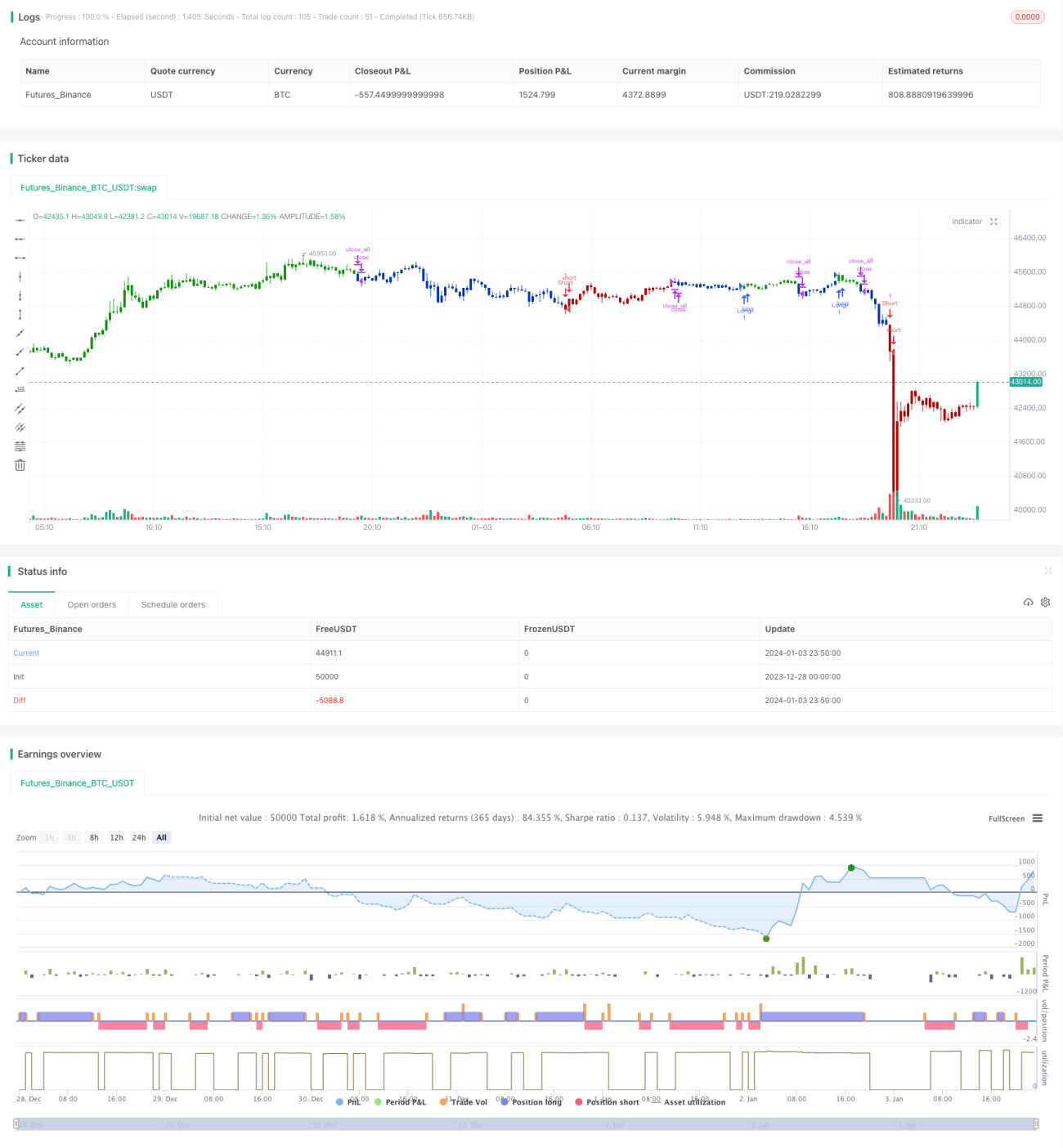

/*backtest

start: 2023-12-28 00:00:00

end: 2024-01-04 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 10/12/2019

// This is combo strategies for get a cumulative signal. - 1