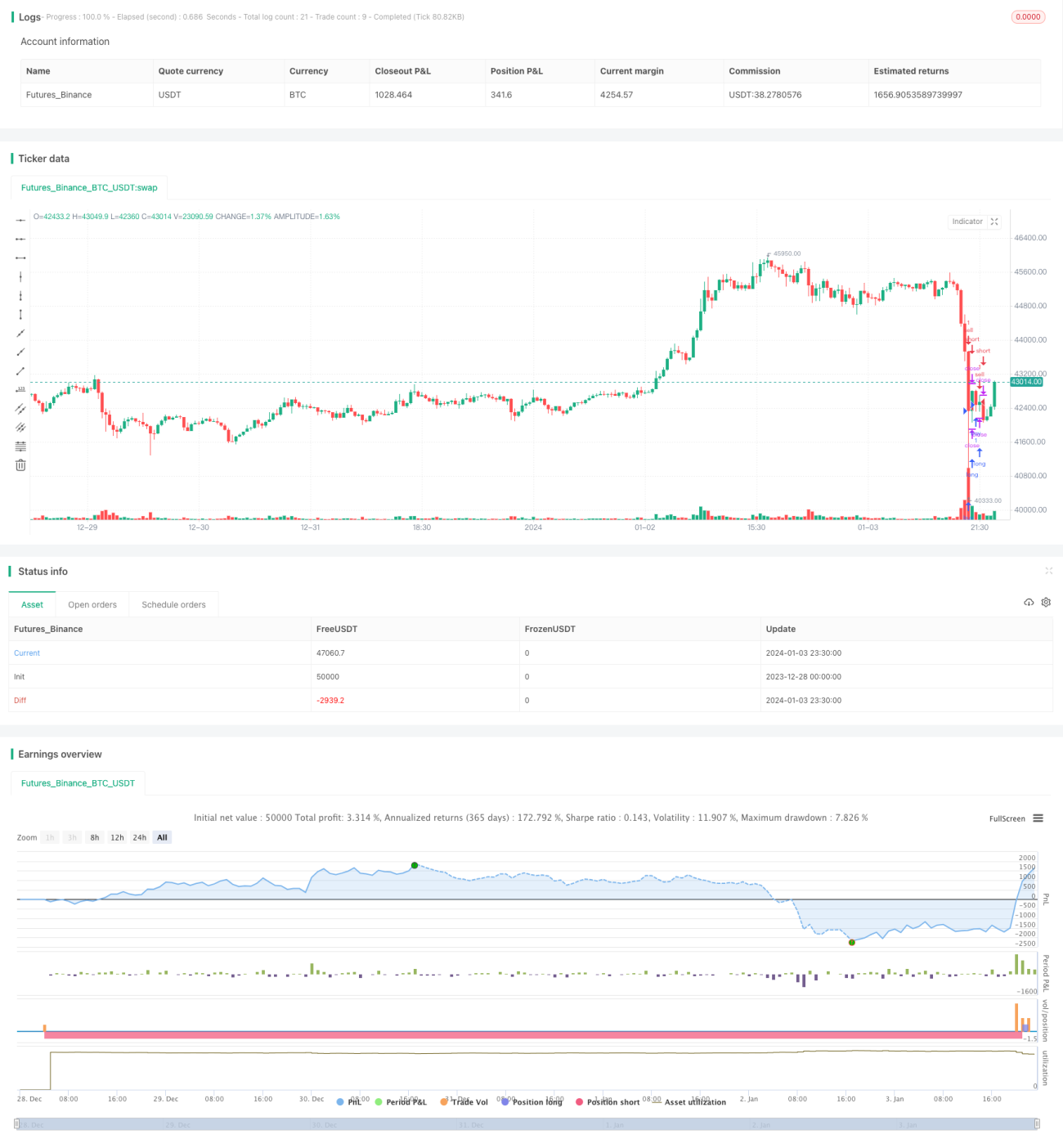

Price Drop Buy Strategy in Downtrend with Stop Loss

Overview

This strategy uses the RSI indicator to determine the potential market trend direction, combined with the Bollinger Bands indicator to identify key support and resistance areas, and looks for low absorption opportunities in trend shock markets to establish long positions and take profits at overbought areas.

Strategy Logic

-

Use the RSI indicator to determine the potential market trend direction. RSI below 40 is considered an oversold area where the market could turn bullish. RSI above 50 is considered an overbought area where the market could turn bearish.

-

Use the Bollinger Bands indicator to identify key support and resistance areas. The middle band of Bollinger Bands is the moving average line of price, and the upper and lower bands form the standard deviation channel of price. Prices approaching the lower band present low absorption opportunities.

-

When RSI <40 and price approaches the Bollinger lower band, it is determined as a low absorption long opportunity to establish a long position.

-

When RSI >50 or profits exceed 50%, close long positions to take profits and cut losses.

Advantage Analysis

-

Use RSI to determine potential market trend direction to avoid trading against the trend.

-

Identify precise entry timing combining with Bollinger Bands to locate low absorption points.

-

Adopt trend shock methodology to prevent being trapped.

-

Flexible stop profit and stop loss mechanism to maximize profits.

Risk Analysis

-

Improper Bollinger parameters may fail to correctly locate the support area.

-

Trend breakthroughs or false breakthroughs could lead to errors in overbought and oversold judgements.

-

Improper stop profit and stop loss points setting may lead to premature exit or enlarged losses.

Optimization Directions

-

Optimize Bollinger parameters for more accurate identification of support and resistance areas.

-

Incorporate other indicators like MACD and KDJ to filter false signals.

-

Dynamically optimize stop profit and stop loss algorithms to maximize profits while minimizing losses.

Summary

This strategy determines potential trend direction with RSI, combined with Bollinger Bands to identify support areas, realizing low buy high sell, which is a typical trend shock strategy. With proper optimization, it can become a reliable and stable profitable quantitative strategy.

- 1