Reversal Tracking Strategy with Double Mechanisms

Overview

This strategy combines the strengths of double mechanism indicators by using 123 pattern to determine reversal signals, and aided by Price Volume Index to determine momentum signals, in order to capture short-term reversal trends.

Strategy Logic

-

123 pattern for reversal signal

-

Constructed with 9-day Stoch fast line and slow line

-

When close price falls for 2 consecutive days and rises on the 3rd day, and Stoch fast line is below 50, a buy signal is generated

-

When close price rises for 2 consecutive days and falls on the 3rd day, and Stoch fast line is above 50, a sell signal is generated

-

-

Price Volume Index for momentum signal

-

PVI judges momentum by comparing volume change between previous and current day

-

When PVI crosses above its N-day moving average, momentum amplifies and a buy signal is generated

-

When PVI crosses below its N-day moving average, momentum declines and a sell signal is generated

-

-

Dual signal combination

- Trading signals are only generated when 123 reversal and PVI momentum signals agree

In summary, this strategy leverages the advantage of dual mechanism indicators to effectively identify short-term price-volume reversal opportunities.

Advantage Analysis

-

123 pattern catches key short-term reversal spots

-

PVI momentum judges coordinated price-volume action to avoid false breakouts

-

Parameter optimized Stoch filters out most noise signals in turbulent zones

-

Dual signal reliability higher than single signals

-

Intraday design avoids overnight risks suitable for short-term trading

Risk Analysis

-

Failed reversal risk

- 123 pattern reversal signals do not always succeed with pattern failure risks

-

Indicator failure risks

- Stoch, PVI and other indicators can fail in certain anomalous markets

-

Dual signal miss risk

- Relatively stringent dual signal criteria may miss some single signal opportunities

-

High trading frequency risks

- Close monitoring of position sizing and risk control is needed for the high frequency strategy

Optimization Direction

-

Large parameter optimization space

- Windows, cycles of Stoch, PVI etc. have optimization space

-

Can incorporate stop loss strategies

- Mobile stop loss can ensure win rate

-

Consider adding filter conditions

- Tests can add moving average, volatility filters etc.

-

Optimize dual signal portfolio

- Test combinations of more dual indicator strategies

Summary

This strategy forms a high-reliability short-term price-volume reversal system through the combination of Stoch and PVI indicators. Compared to single indicators, it has higher win rate and positive expectancy. Sharpe ratio can be further improved via optimization and risk control. In conclusion, this strategy leverages the strengths of dual mechanism indicators to effectively capture short-term reversal opportunities in the market, and is worth live testing and optimization.

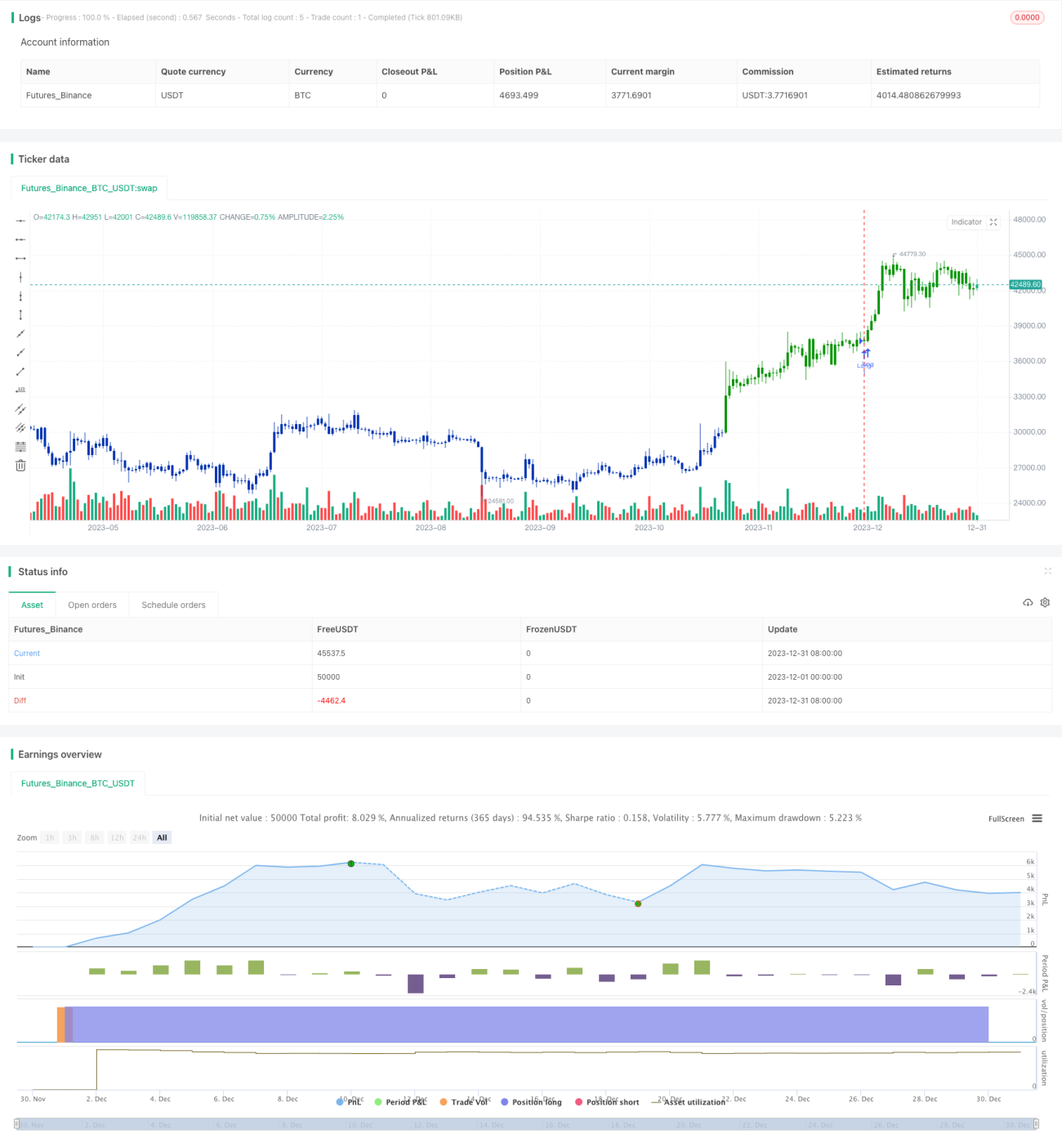

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/04/2021

// This is combo strategies for get a cumulative signal. - 1