Moving Average System Trading Strategy

Overview

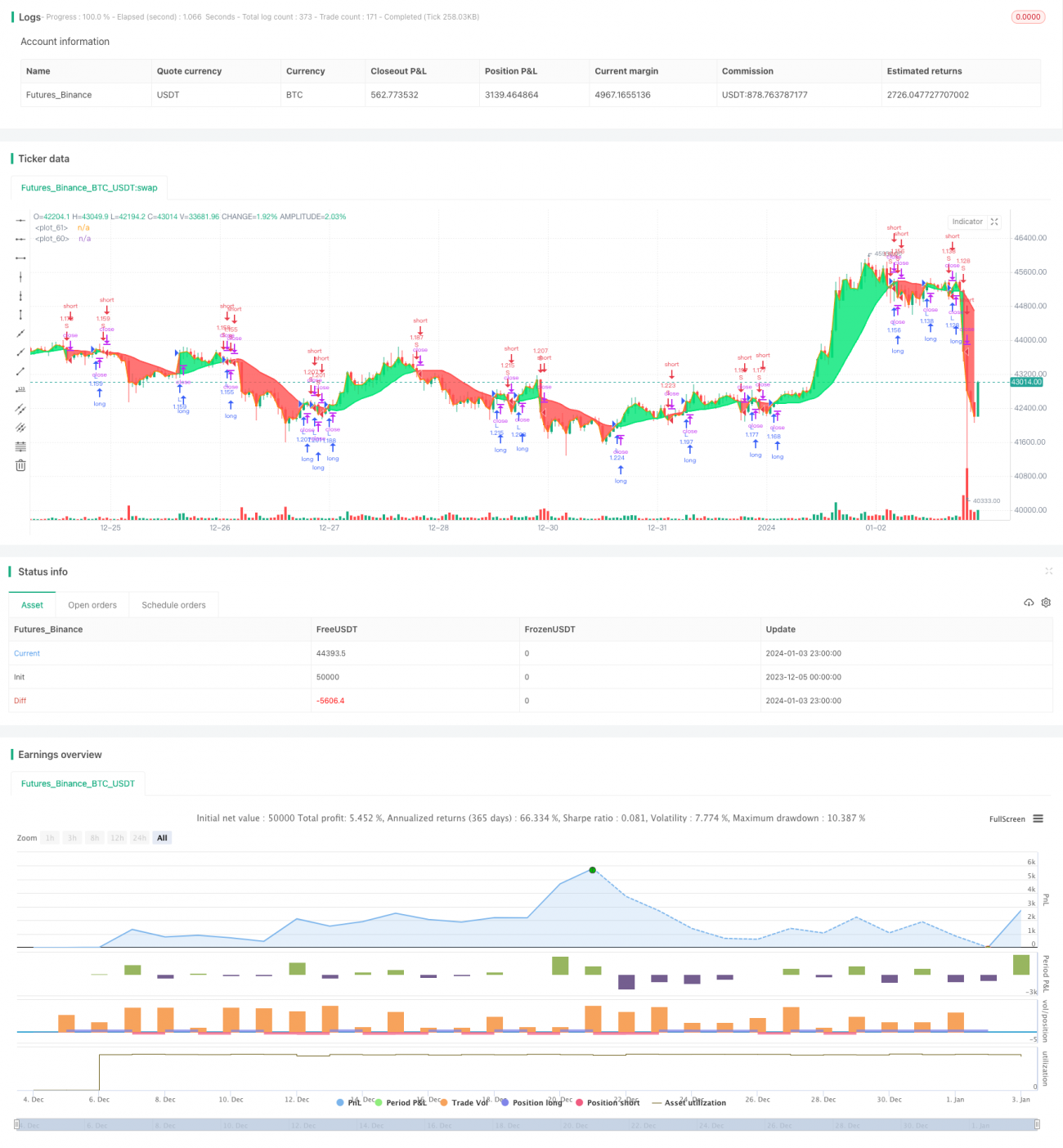

This article discusses a trading strategy based on a simple moving average. The strategy compares the closing price with a 17-period moving average, going long when the closing price crosses above the moving average and going short when it crosses below.

Strategy Logic

Moving Average Calculation

The strategy uses the following parameters to calculate the moving average:

- MA Source: Default to average of OHLC (OHLC4)

- MA Type: Default to Simple Moving Average (SMA)

- MA Length: Default to 17

Based on these parameters, the getMAType() function is called to calculate the 17-period SMA of closing prices.

Trading Signal Generation

Then compare the relationship between the closing price and the moving average:

- Close > Moving Average: Long signal

- Close < Moving Average: Short signal

When the closing price crosses above the moving average from below, a long signal is generated. When it crosses below from above, a short signal is generated.

Trade Execution

During the backtest period, open long positions when long signals appear and open short positions when short signals appear.

Advantage Analysis

The biggest advantage of this strategy is that the logic is very simple and clear. With just one indicator, it judges the trend reversal based on the direction change of the indicator. The strategy is easy to understand and implement, suitable for beginners to learn.

In addition, moving averages belong to trend-following indicators, which can effectively track trend changes and avoid interference from short-term market noise.

By adjusting parameters, it can adapt to different cycles and different products.

Risk Analysis

Firstly, this strategy relies solely on one indicator, so the judgment criteria are relatively single, which may generate more false signals.

Also, as a trend following system, it does not work well in range-bound and sideways markets.

Besides, without stop loss or take profit, there is a risk of expanding losses.

The solutions are to incorporate other indicators, optimize parameter combinations to reduce false signals. Add stop loss and take profit to control risks and optimize drawdowns.

Optimization Directions

Here are some ideas for optimizing the strategy:

-

Adjust moving average parameters, optimize period numbers, e.g. change to 30-period or 50-period.

-

Try different types of moving averages, like EMA, VIDYA etc. They have varying sensitivity to price changes.

-

Add other indicators in combination, e.g. MACD to judge strength; RSI to reduce false signals.

-

Add stop loss mechanisms. Set fixed percentage or ATR-based trailing stop loss to control single-trade loss amount.

-

Add take profit mechanisms. Set target profit percentage to maximize profits.

These optimizations can make the strategy performance more stable and avoid excessive drawdowns.

Summary

This article analyzes a simple trading strategy based on a 17-period moving average. The strategy has simple signal sources, easy to understand and implement, belonging to a typical trend following system. Through in-depth interpretation of the strategy, its pros and cons are analyzed, and multiple dimensions of optimization ideas are proposed. It is believed that through continuous optimization and enrichment, this strategy can gradually evolve and achieve stable returns in live trading as well.

/*backtest

start: 2023-12-05 00:00:00

end: 2024-01-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Simple 17 BF 🚀", overlay=true, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.0)

/////////////// Time Frame ///////////////- 1