ATR Trend Following Strategy Based on Standard Deviation Channel

Overview

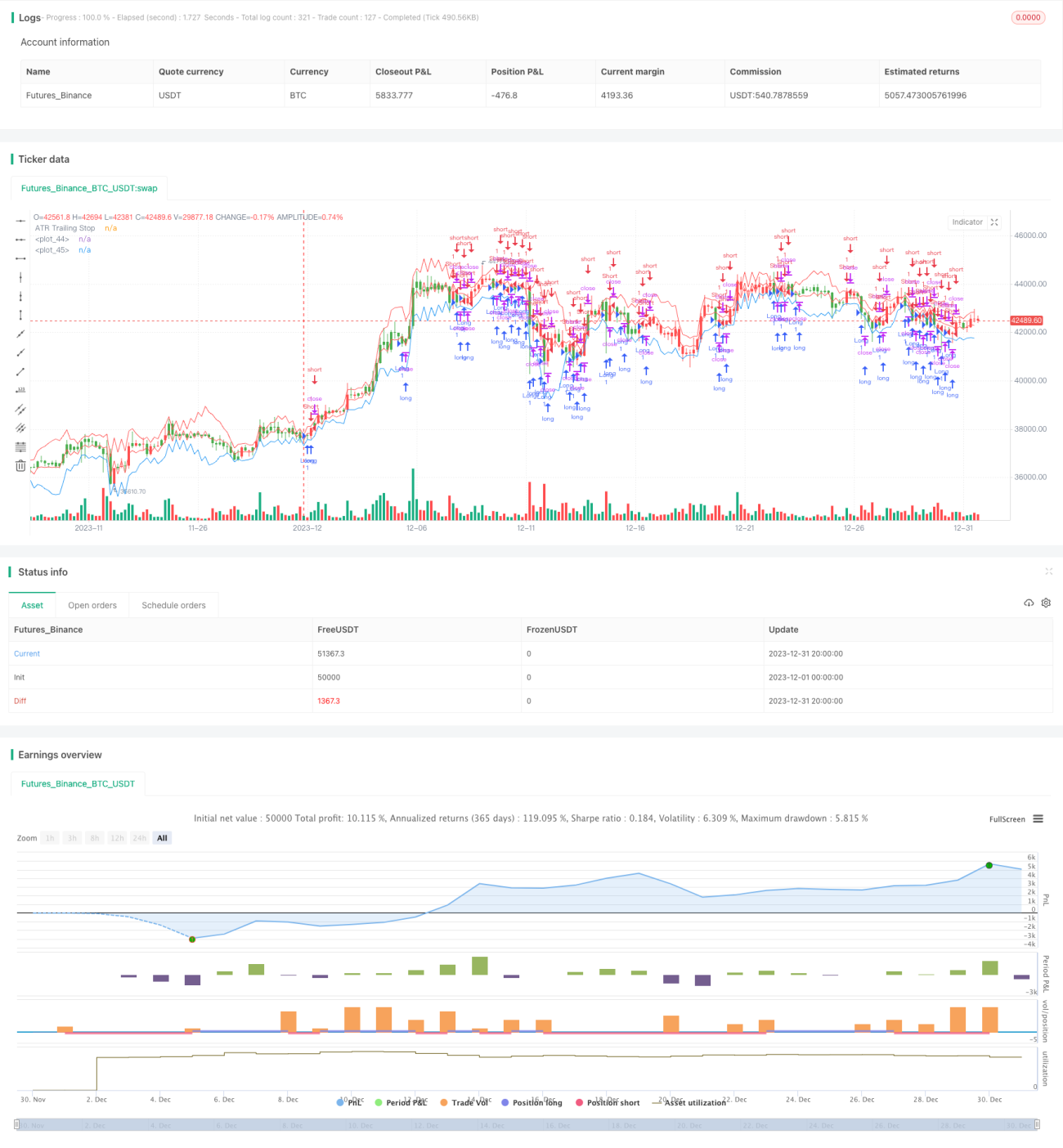

This strategy named "ATR Trend Following Strategy" is a trend following trading strategy based on Average True Range (ATR) for stop loss and standard deviation channel for entry signals. It is suitable for financial products with obvious trends, such as indexes, forex and commodities.

Trading Logic

The strategy uses ATR indicator to set stop loss price. ATR reflects the volatility of the market and can be used to dynamically set stop loss distance. The strategy calculates ATR value based on user input ATR period and multiplier, and uses the ATR value multiplied by the multiplier as stop loss distance. Specifically, the ATR trailing stop calculation formula is:

ATR Line = Prior ATR Line ± nLoss (nLoss = nATRMultip * ATR value)

If close > ATR Line, adjust ATR Line up to close - nLoss

If close < ATR Line, adjust ATR Line down to close + nLoss

This way, the ATR line can adjust dynamically based on price fluctuation to achieve trend following stop loss.

In addition to ATR trailing stop, the strategy also uses standard deviation channel to determine entry signals. The standard deviation channel calculation formula is:

Middle Line = ATR Trailing Stop Line

Upper Band = Middle Line + n * Standard Deviation

Lower Band = Middle Line - n * Standard Deviation

Go long when price breaks middle line upwards. Go short when price breaks middle line downwards.

Advantages

The biggest advantage of this strategy is that it uses ATR indicator to set stop loss dynamically based on market volatility, enabling trend following stop loss and effective risk control.

Additionally, using standard deviation channel for entry signals avoids frequently opening positions due to small price fluctuations.

Risks and Solutions

The main risk is that if stop loss distance is too big it cannot control risk effectively, but if it is too small it can be easily stopped out by market noise. To address this risk, ATR period and multiplier can be optimized to find the best parameter combination.

Another risk is inappropriate standard deviation channel parameters leading to overly high/low entry frequency. Parameters can be optimized to find the optimum.

Enhancement Opportunities

The strategy can be enhanced from the following aspects:

-

Optimize ATR period and multiplier to achieve better stop loss effect.

-

Optimize standard deviation channel parameters for better entry signals.

-

Add other indicators for filtering, e.g. moving average, candlestick patterns etc., to assist judging trend direction and improve profitability.

-

Optimize entry and exit logic, e.g. open positions only after confirming candlestick pattern when price reaches channel bands.

Summary

The strategy achieves trend following stop loss based on ATR indicator and uses standard deviation channel for entry signals. Its advantages lie in good risk control capability for trend trading. Risks and enhancements are also clearly analyzed. The strategy is worth further testing and optimization and has practical trading value.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version = 2

strategy(title="Average True Range Strategy", overlay = true)

nATRPeriod = input(11) //Hur många perioder ATR är på

nATRMultip = input(0.5) //Hur många gånger nuvarande ATR multipliceras med- 1