Supertrend Advance Strategy

Overview

The Supertrend Advance Strategy is an optimized and upgraded version based on the classic Supertrend indicator. It combines price action, volatility, and multiple technical indicators to improve signal quality, reduce noise, and more accurately capture changes in market trends.

Strategy Principles

The core of the Supertrend Advance Strategy is the Supertrend line. It is calculated based on the average true range and price momentum to determine potential trend direction and inflection points. When the price is above the Supertrend line, it indicates an uptrend. Conversely, when below the line, it signals a downtrend.

Unlike the traditional Supertrend indicator which primarily considers closing price and ATR, the Advance strategy also incorporates dimensions like trading volume, momentum oscillators, and even fundamental data to validate the reliability of signals. This multidimensional approach ensures the generated signals are more reliable and less prone to market noise.

Advantage Analysis

The main advantages of the Supertrend Advance Strategy include:

-

More accurate trend identification and false breakout filtering. By waiting for confirmation from multiple indicators, the strategy greatly improves accuracy.

-

Reduced noise interference. The combination of filters screens out excessive unimportant market data, making judgments clearer.

-

Enhanced risk management. Clear trade signals facilitate planning stop losses and take profits more effectively.

-

Versatility. Apart from identifying trends, the strategy can also combine with other technical tools to create comprehensive trading systems.

Risk Analysis

The Supertrend Advance Strategy also has the following major risks:

-

Parameter setting risks. Incorrect parameter combinations may render the strategy ineffective or trigger too many false signals.

-

Trend misjudgment risks. No strategy can completely avoid the risk of judgment errors. When trends unexpectedly change, losses may be incurred.

-

Over-optimization risks. When parameters are over-fitted to historical data, the strategy may fail to adapt to changing market conditions.

-

Trading cost risks. As trade frequency increases, costs like commissions and slippage also rise significantly.

Corresponding solutions:

-

Optimize parameter settings and regularly backtest robustness.

-

Set stop loss and take profit to limit per trade loss.

-

Avoid over-optimization to maintain generalization capability.

-

Calculate risk/reward of signals and manage trading costs.

Optimization Directions

The Supertrend Advance Strategy can be optimized in the following aspects:

-

Adjust parameters based on different markets to better fit their characteristics. For instance, reduce cycle lengths for volatile markets.

-

Add adaptive filtering mechanisms to auto tune indicators or disable filters in certain market states.

-

Explore machine learning methods to dynamically optimize parameters using neural networks.

-

Incorporate sentiment data and news analytics to improve performance using unstructured data.

-

Add position sizing capability to increase returns when win rate is very high.

Conclusion

By introducing multiple filters and confirmation indicators, the Supertrend Advance Strategy optimizes the classic Supertrend indicator to judge trends more precisely and improve signal quality. Compared to single indicators, this multidimensional strategy provides more robust, comprehensive and efficient trading solutions. However, risks like improper parameter tuning and judgment errors should also be guarded against by adopting appropriate risk control measures. With further optimizations and integration with other tools, the Supertrend Advance Strategy has immense application potential.

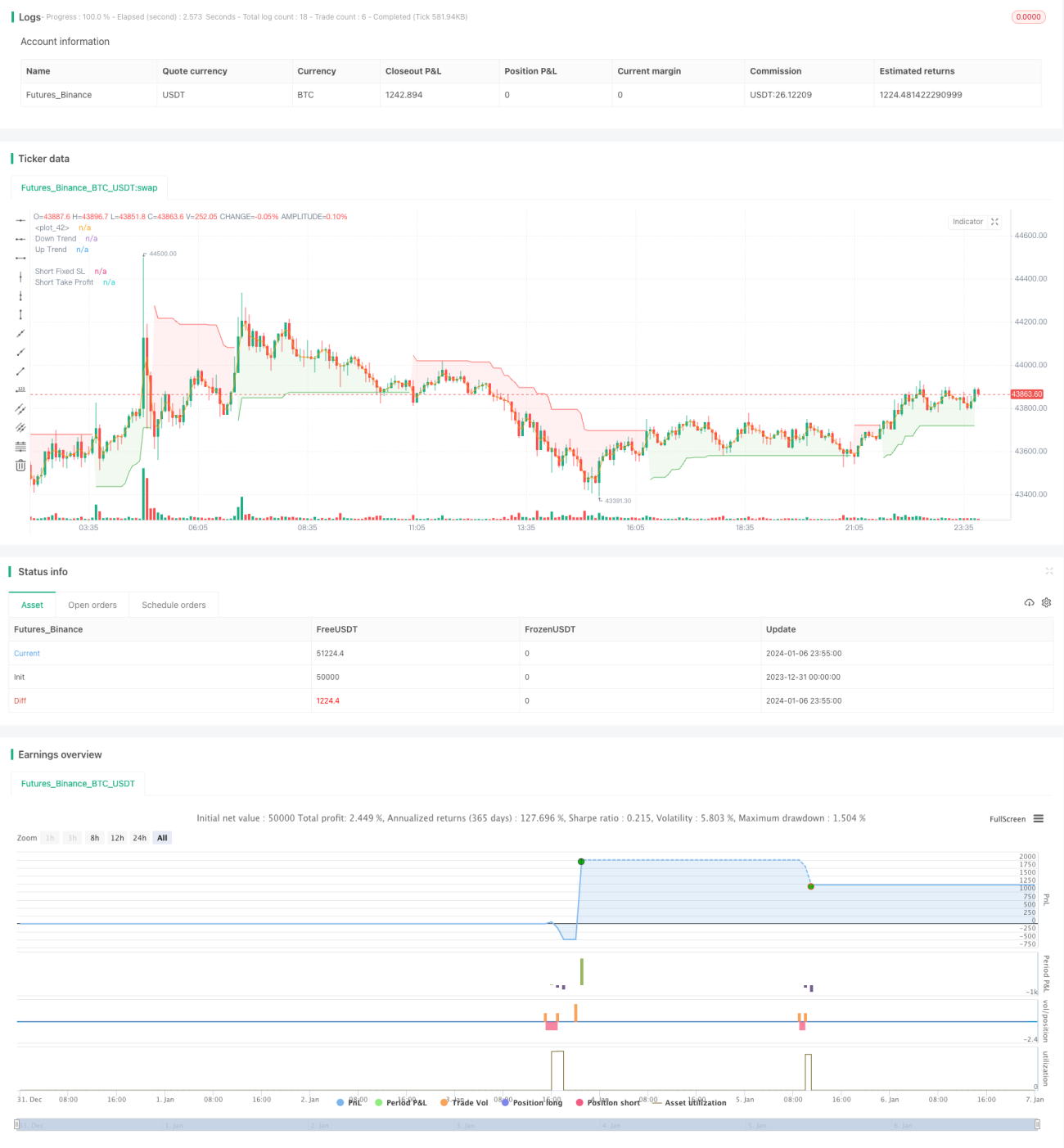

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1