Crude Oil Moving Average Crossover Strategy

Overview

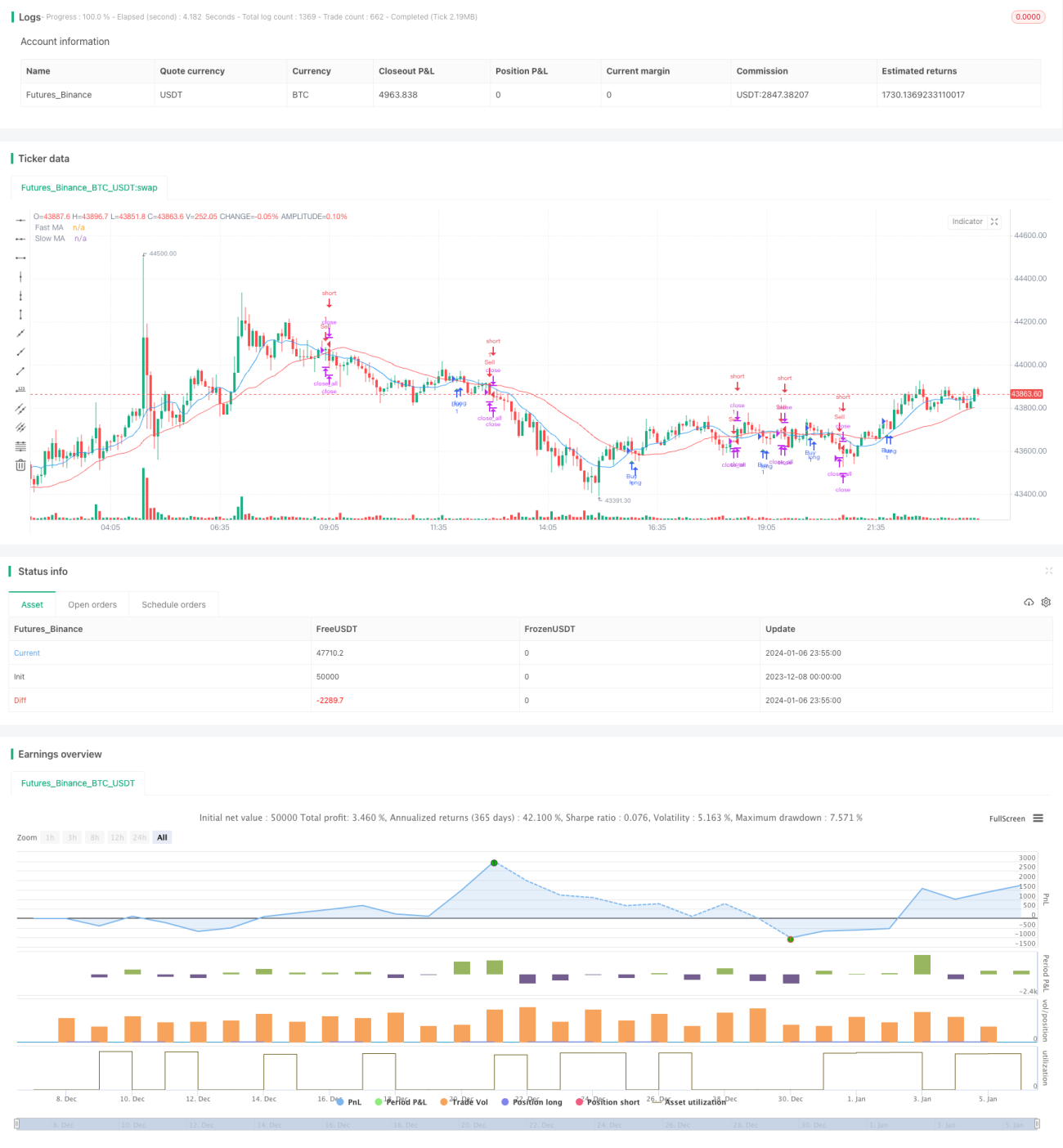

This strategy utilizes two moving averages with different parameters, a faster moving average and a slower moving average. When the faster moving average crosses above the slower moving average, a buy signal is generated. When the faster moving average crosses below the slower moving average, a sell signal is generated. Additionally, a sell signal is generated if the slower moving average crosses above the faster moving average.

Strategy Logic

The core logic of this strategy is based on the golden cross theory of moving averages. The so-called golden cross refers to the fast moving average crossing above the slow moving average, which is regarded as a signal of market reversal and usually indicates upward movement in price. The death cross, on the other hand, refers to the fast moving average crossing below the slow moving average, indicating downward price movement.

Specifically, this strategy defines two moving averages - a fast moving average with length 10 days and a slow moving average with length 30 days. At the end of each candlestick bar, the values of these two moving averages are calculated. If the fast moving average crosses above the slow moving average, a buy signal is generated. If the fast moving average crosses below the slow moving average, a sell signal is generated.

To cut losses in a timely manner, if the slow moving average crosses above the fast moving average, a sell signal is also generated to close all positions directly.

Advantage Analysis

This strategy has the following advantages:

-

It utilizes the golden cross theory of moving averages, which is a simple and effective technical indicator trading strategy.

-

The fast moving average has a parameter of 10 days, which can respond quickly to price changes. The slow moving average has a parameter of 30 days which can filter out market noise effectively.

-

The strategy incorporates a stop loss mechanism which cuts losses fast when unfavorable patterns emerge, effectively controlling risks.

-

The strategy logic is simple to understand and implement, suitable for automated execution in quantitative trading.

-

Indicator parameters can be adjusted flexibly for trading different products.

Risk Analysis

While the strategy has obvious advantages, there are also certain risks to be aware of:

-

If prolonged trending occurs in the market, it may generate frequent false signals. This can be optimized by adjusting moving average parameters.

-

Moving averages themselves have a lagging nature, which may cause some lag in signal generation.

-

Single indicator strategies are easily misguided and should be combined with other factors to determine final entry.

-

Improper stop loss positioning may lead to unnecessary losses. Reasonable stop loss levels should be set for different products.

Optimization Directions

There is room for further optimization of this strategy:

-

More parameter combinations can be tested to find the optimal lengths for fast and slow moving averages.

-

Confirmation from other indicators like volume, Bollinger bands etc. can be added to improve signal accuracy.

-

Adaptive moving averages can be used to optimize parameters dynamically based on varying market conditions.

-

Slippage control can be implemented to avoid unnecessary slippage loss in times of high volatility.

-

A dynamic stop loss strategy can be added based on ATR to set stops.

Conclusion

This strategy utilizes the simple double moving average golden cross theory to provide a simple and practical technical indicator trading strategy for quantitative trading. It is easy to understand and implement, and can be applied to different products and market environments after parameter optimization, making it worthwhile for quantitative investors to pay attention to and test.

Overall, moving average strategies have a probability edge, and with strict risk control, can be profitable in the long run. But traders also need to be aware of its limitations, apply it flexibly, and complement it with other analysis tools.

- 1