Multi-level Moving Average Crossing Strategy for Quant Masters

Overview

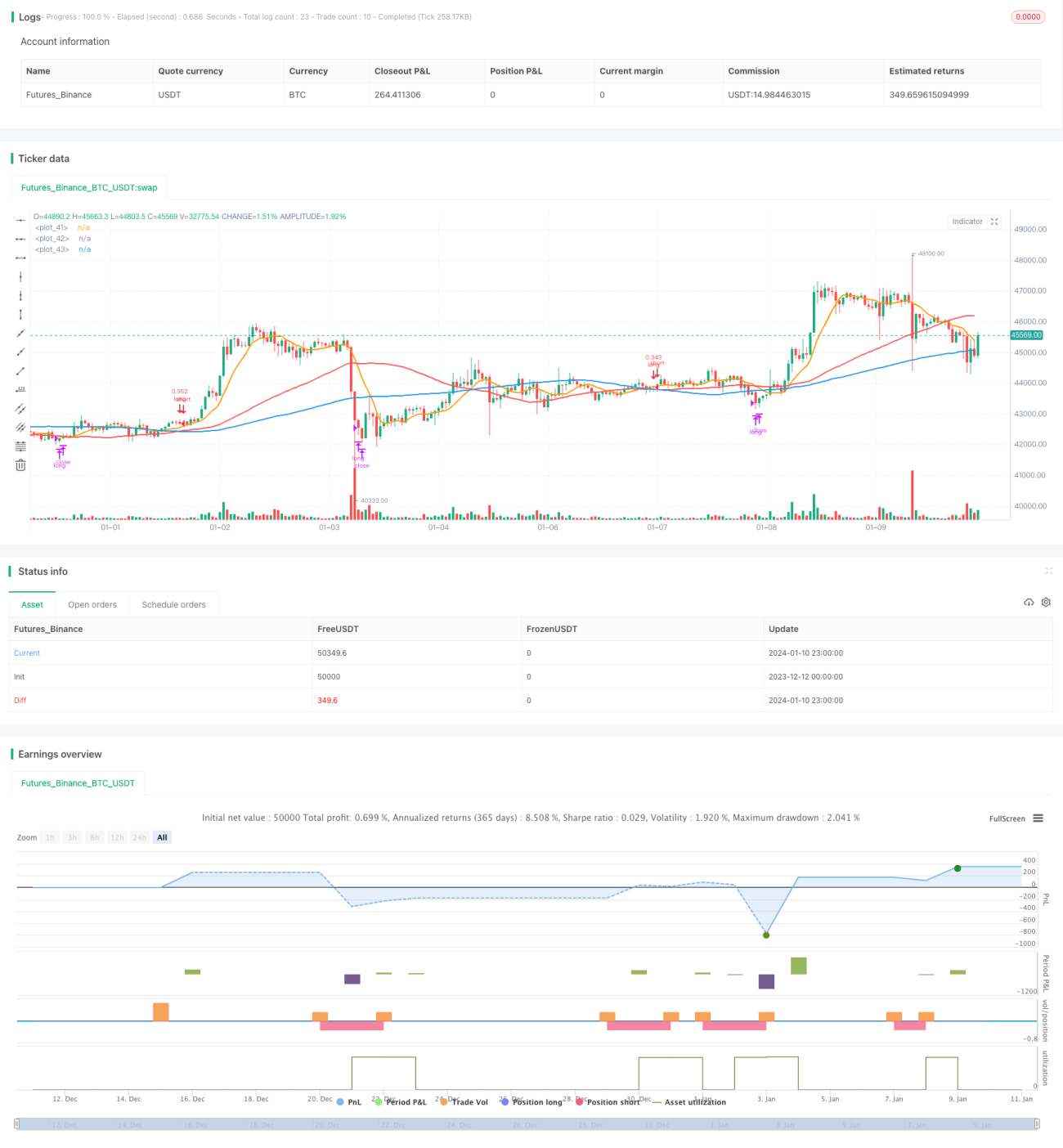

This strategy utilizes the principle of multi-level moving average line crossing to capture medium-long term trends and achieve steady profits. It employs fast, medium, and slow three sets of moving averages with different parameters and makes trading decisions based on their crossovers. Compared to traditional strategies with only two sets of moving averages, this multi-level moving average crossing strategy can filter out more false signals and improve the win rate of the strategy.

Strategy Logic

The strategy uses three sets of moving averages: the fast moving average MAshort, the medium speed moving average MAmid, and the slow moving average MAlong. MAshort has a parameter of 9, responds the fastest, and is used to capture short-term signals; MAmid has a parameter of 50, has a medium speed and is used to confirm the trend; MAlong has a parameter of 100, responds the slowest and is used to determine long-term trend direction.

The specific trading logic of the strategy is: when the medium speed moving average line MAmid crosses above the slow moving average line MAlong, it indicates that the upward momentum of the stock price is forming. At this time, the strategy goes long; when the fast moving average MAshort crosses below the medium speed moving average MAmid, it indicates that a short-term trend reversal has occurred, and the strategy exits its position at this time.

The biggest advantage of this strategy is that by combining multiple moving averages, it can effectively filter out false signals and only choose relatively strong breakouts during a medium-long term uptrend to open long positions.

Advantage Analysis

The advantages of this strategy are:

- The strategy parameters are optimized to effectively match the medium and long term trends with a relatively high win rate.

- The multi-level moving average design filters noise and false signals.

- It is suitable for all kinds of stocks and cryptocurrencies with relatively good historical backtesting results.

- The operation frequency is low and each opening position occupies 30% of the funds and the risk is controllable.

- The time period is configurable, which provides flexibility for live trading.

Risk Analysis

This strategy also has the following risks:

- The probability of long-term trend reversals is relatively small but when it does happen, the stop loss magnitude may be large.

- The trading frequency is low and therefore has the problem of inefficient capital utilization.

- The parameters of the strategy need to be optimized for different trading varieties, which limits the applicable scope.

To address these risks, we will further expand the applicability of the strategy while controlling maximum drawdown with stop loss techniques. We will respond to the reversal of the medium and long term trend by reducing positions.

Optimization Directions

This strategy can also be optimized in the following ways:

- Optimize the days parameter of the moving average to find the best parameter combination

- Add volume indicators to confirm and avoid curve fitting problems

- Set the maximum loss for the strategy, such as 20% max drawdown, to force stop loss

- Incorporate machine learning models to judge trends and improve the adaptability of the strategy

Summary

This strategy belongs to a typical medium-long term quantitative strategy which, with the premise of controlling trading risks, continuously profits by matching multi-level moving averages with medium-long term trends. Compared with a single indicator, this strategy incorporates multiple parameters and can effectively identify strong medium and long term trend signals. Through further optimization, this strategy can be applied to more varieties and play an important role in quantitative trading.

- 1