RSI V-shaped Pattern Swing Trading Strategy

1

Follow

1802

Followers

Overview

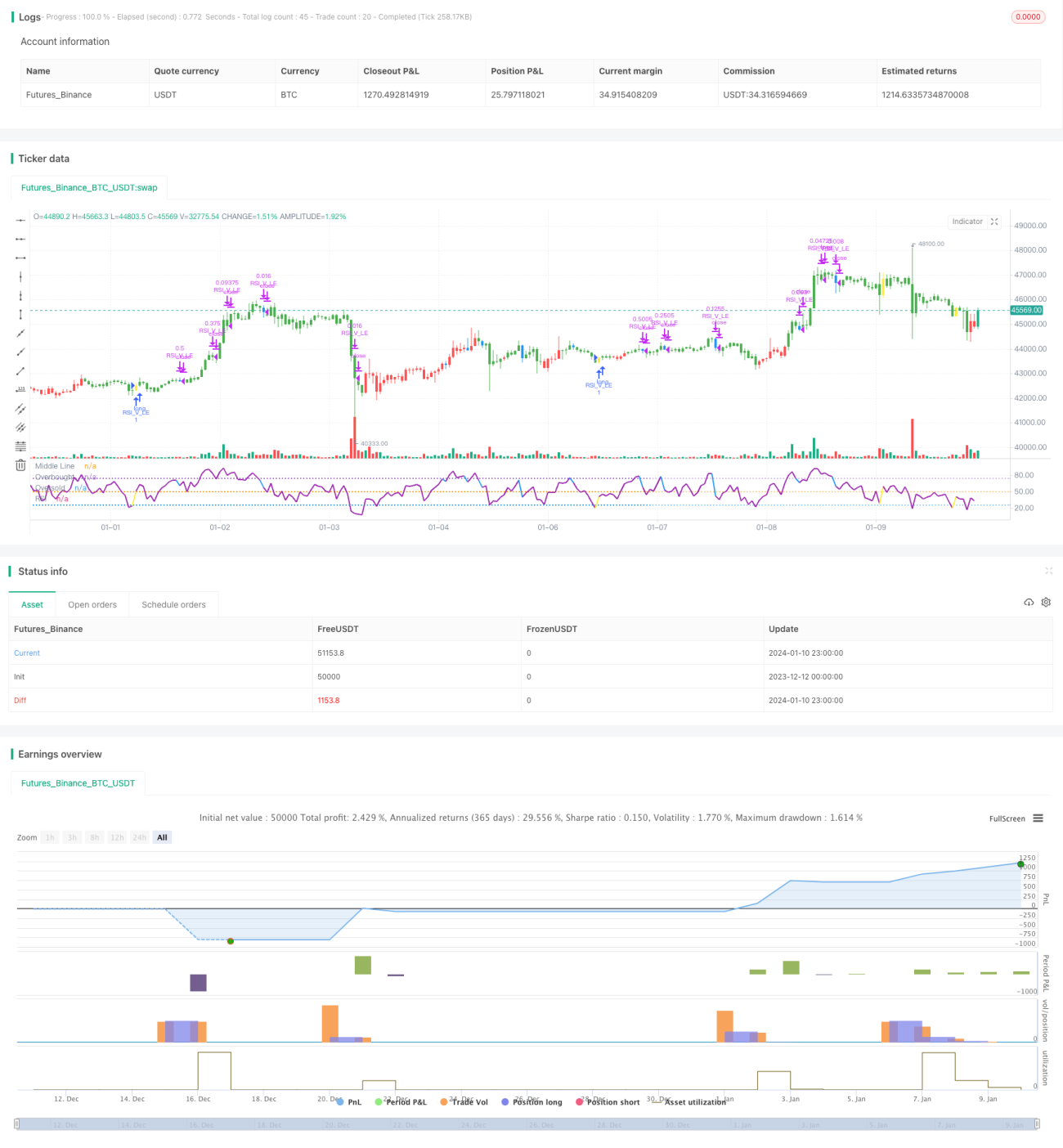

This strategy is based on the V-shaped pattern formed by the RSI indicator, combined with EMA filters, to develop a reliable short-term profitable trading strategy. It captures rebound opportunities when the price is oversold by accurately going long through RSI’s V-shaped signals, for the purpose of making profits in the short run.

Strategy Logic

- Use 20-day EMA above 50-day EMA as the judgment of long-term uptrend

- RSI forms V-shaped pattern, indicating oversold rebound opportunities

- Previous bar's low is lower than previous 2 bars' low

- Current bar’s RSI is higher than previous 2 bars’ RSI

- RSI crosses above 30 as the completion signal of V-shaped pattern to go long

- Set stop loss at 8% below entry price

- When RSI crosses 70, start closing positions and move stop loss to entry price

- When RSI crosses 90, close 3/4 positions

- When RSI goes below 10 / stop loss triggered, close all positions

Advantage Analysis

- Use EMA to judge overall market direction, avoid trading against the trend

- RSI V-shaped pattern captures mean-reverting opportunities when oversold

- Multiple stop loss mechanisms to control risks

Risk Analysis

- Strong downtrend may incur unstoppable losses

- RSI V-shaped signals may give false signals, leading to unnecessary losses

Optimization Directions

- Optimize RSI parameters to find more reliable V-shaped patterns

- Incorporate other indicators to enhance reliability of reversal signals

- Refine stop loss strategy, balance between preventing over-aggressiveness and timely stop loss

Summary

This strategy integrates EMA filter and RSI V-shaped pattern judgment to form a reliable short-term trading strategy. It can effectively seize the rebound opportunities when oversold. With continuous optimization on parameters and models, improving stop loss mechanisms, this strategy can be further enhanced in stability and profitability. It opens the door of profitable swing trading for quant traders.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1