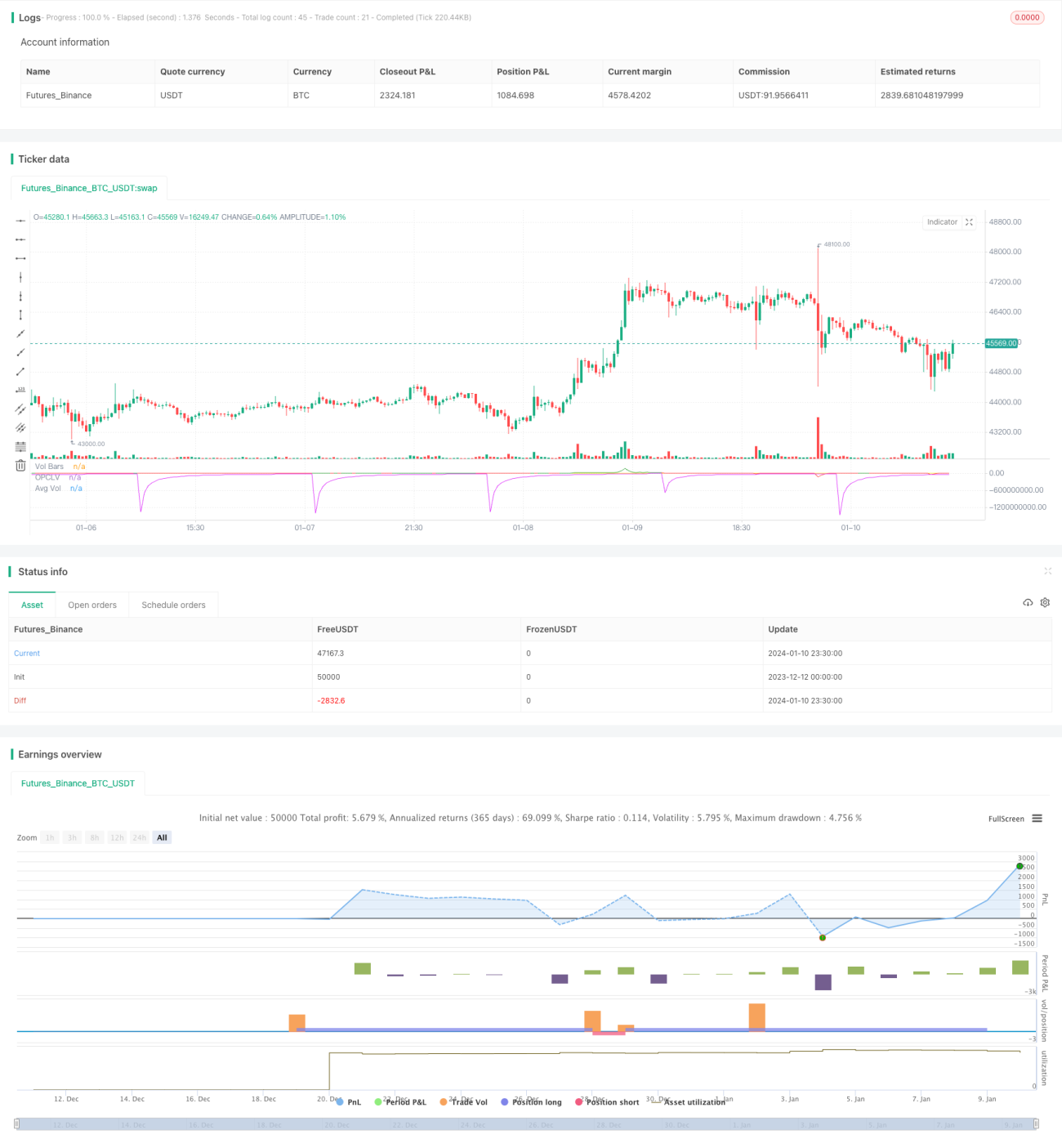

Quantitative Trading Strategy - Quantity Trend Tracking Opening

Overview

This strategy realizes the automatic opening operation of discovering quantity trends by tracking price movement trends and combined with changes in trading volume. The strategy uses the moving average system to judge the price change trend, and then combines the change of trading volume in the same direction as the opening confirmation signal.

Strategy Principle

The core logic of the quantitative trading strategy quantity trend tracking opening is based on tracking the matching relationship between price movement trends and changes in trading volume. Specifically, the strategy uses the difference between the closing price and the opening price as the price change, and then multiplies it by the trading volume of the day to obtain the price and volume joint curve. This joint curve can reflect the price change trend and trading volume accompanies the relationship at the same time. Then calculate the moving average of this joint curve as the quantitative trend benchmark. When the joint curve penetrates its moving average, a buy signal is generated. When it falls below its moving average, a sell signal is generated, thereby realizing the opening operation of quantitative tracking of price trend changes.

Advantage Analysis

This strategy combines price movement trends and changes in trading volume to effectively filter out some price-insensitive false trends and reduce opening risks and improve opening accuracy. Compared with pure price technical indicators, the effect of quantitative tracking is better. This strategy also uses the moving average system to set dynamic benchmark lines, which can automatically adapt to changes in market conditions and has high flexibility.

Risk Analysis

This strategy mainly relies on the price-volume relationship to determine the reasonableness of the quantitative trend. If the relationship between price and volume becomes unmatched, it will lead to an increase in misjudgment risks. In addition, improper setting of moving average parameters will also affect strategy effectiveness. Need to be optimized and tested for different varieties and market environments.

Optimization Direction

Consider joining more filters to optimize strategies, such as using volatility indicators to determine trend quality, introducing sentiment indicators to determine market psychology, and so on. It is also possible to test the change in strategy effectiveness under different moving average systems to find the optimal parameter portfolio. Adding machine learning model training to judge rules is also the direction for follow-up optimization.

Summary

This quantitative trading strategy realizes automatic opening based on tracking and judging the price trend and trading volume relationship, by quantifying matching price trends with trading enthusiasm, it can effectively filter out invalid signals and improve the success rate of opening. There is still a lot of room for optimization of strategies, which is worth continuing research and improvement.

- 1