Zero Lag Volatility Breakout EMA Trend Strategy

Overview

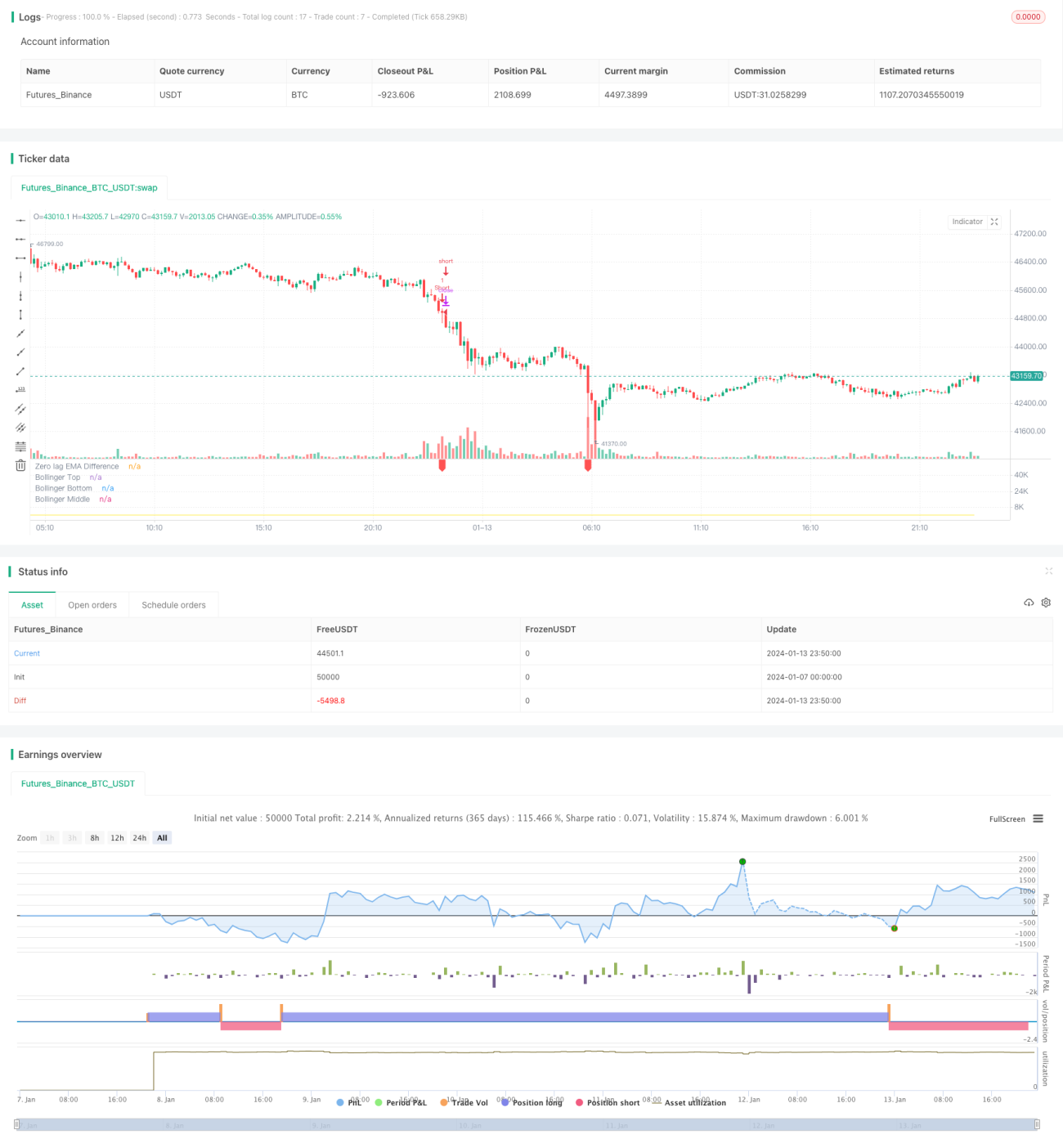

This is a simple breakout strategy that uses the difference between two different zero lag EMAs to track the upward or downward momentum of an instrument. When the difference breaks out a Bollinger Band of configurable standard deviation, long/short signals are generated based on the direction of the underlying EMA.

Strategy Logic

The strategy uses two specially calculated EMA indicators to get the volatility difference, as shown in below formulas:

hJumper = math.max(src,ta.ema(src,lx))

lJumper = math.min(src,ta.ema(src,lx))

dif = (hJumper / lJumper) - 1

The difference responds instantly to sharp price changes without lag.

When dif crosses above the Upper Bollinger Band, entry signal is triggered. When dif crosses below the Middle Bollinger Band, exit signal is triggered. The direction of base EMA determines long or short.

Advantage Analysis

The biggest advantage of this strategy is its fast response to breakout signals without lag. This is achieved by using two specially calculated zero lag EMAs. This allows the strategy to instantly capture price breakout events and enter early in emerging trends.

Another advantage is the simplicity of this strategy. It has only one parameter lx. Less parameters make optimization easier and reduce the risk of overfitting.

Risk Analysis

The main risk of this strategy is possible false breakout of the signals. Consecutive false breakouts may happen during ranging periods. To mitigate this risk, we can increase the Bollinger Band multiple to make signals more stable.

Another risk is frequent small wins/losses during choppy markets. This can be alleviated by adjusting exit mechanisms, for example by setting stop loss or take profit price levels.

Optimization Directions

Below are some directions this strategy can be optimized:

-

Add filter indicators to validate entry signals and reduce false signals.

-

Incorporate stop loss and take profit to better manage trades.

-

Look for trading volume confirmation to avoid false breakouts without volume commitment.

-

Adopt adaptive Bollinger Bands to adjust parameters based on market volatility.

-

Optimize parameters dynamically based on machine learning.

Conclusion

In summary, this zero lag volatility breakout EMA strategy captures price momentum rapidly by using specially calculated EMAs without lag. Next step optimizations may include adding filters, stop loss/profit, volume confirmation etc. to make the strategy robust across different market environments.

- 1