Dual EMA and AC Indicator Based Trend Following Strategy

Overview

This strategy is designed based on dual EMA and AC acceleration oscillator indicators. The dual EMA indicator is used to determine the price trend direction, while the AC indicator is used to confirm the trend signal for filtering effect. This strategy combines both trend following and signal filtering functions to improve signal quality and profit from trends.

Strategy Logic

The strategy consists of two modules:

-

Dual EMA Module

-

Build a dual EMA indicator using 2-day EMA and 20-day EMA. A buy signal is generated when price crosses above 2-day EMA. A sell signal is generated when price crosses below 20-day EMA.

-

This module determines short-term and medium-term trend directions for basic trend following.

-

-

AC Module

-

Use the positive and negative values of the AC acceleration oscillator to confirm trend signals. Trading signals are only generated when dual EMA and AC indicators agree on directions.

-

This module filters out false signals and improves reliability.

-

In summary, this strategy integrates dual EMA for detecting major trends and AC indicator for filtering out false breakouts, forming a systematic trend following methodology.

Advantage Analysis

The advantages of this strategy are:

-

Dual EMA traces medium-long term trends while AC filters out short-term noise, great combo effect.

-

Excellent filtering effect to avoid selling after long profit or buying after short profit.

-

Flexible parameter tuning adaptable to different products and market environments.

-

Clear strategy logic, easy to understand, optimize and improve.

-

Decent trend following profit potential for trending products.

Risk Analysis

There are some risks in this strategy:

-

Improper dual EMA parameter setting may miss shorter trends or generate redundant trades.

-

Improper AC parameter setting may filter out valid but weaker signals or fail to filter enough noise.

-

Unable to adapt to rapidly changing markets, like sharp cliff-styled crashes.

-

Insufficient profitability in ranging markets, should be used as trend following strategy.

Optimization Directions

The strategy can be optimized in the following aspects:

-

Test more parameter combinations to find optimal parameters fitting different product characteristics.

-

Add stop loss module to exit at oversized losses.

-

Filter signals with more indicators.

-

Develop long-short combo strategies to trace medium-long term trends, utilizing short-term trades to reduce or add positions along the trend.

Conclusion

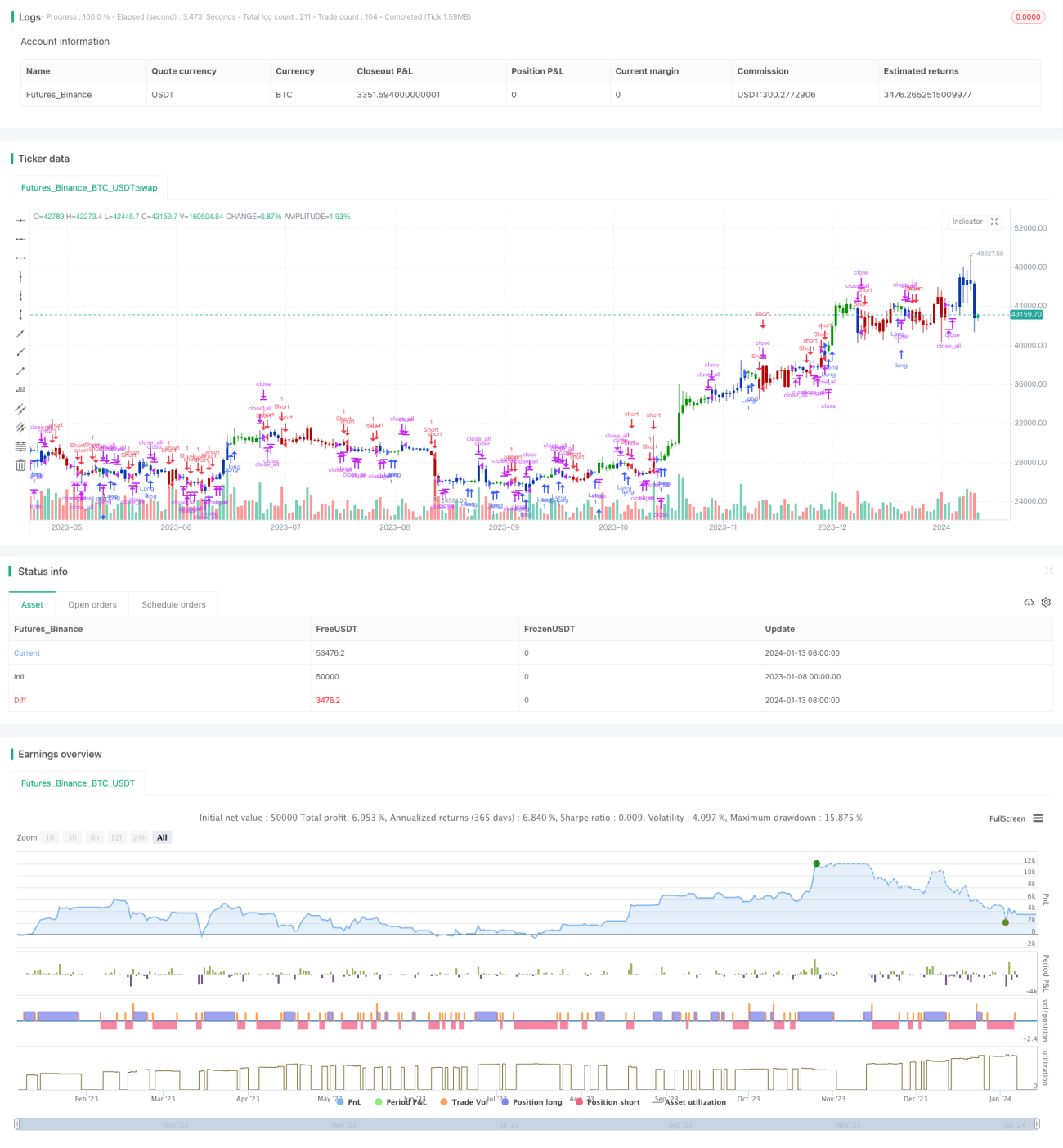

The idea of combining dual EMA for trend and AC for noise filtering is worth learning. This strategy has quality signals and reliability, suitable for tracking trending products. With proper parameter tuning, great profits can be achieved by riding trends using this strategy.

/*backtest

start: 2023-01-08 00:00:00

end: 2024-01-14 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 19/01/2022

// This is combo strategies for get a cumulative signal. - 1