RSI of MACD Reversal Strategy

Overview

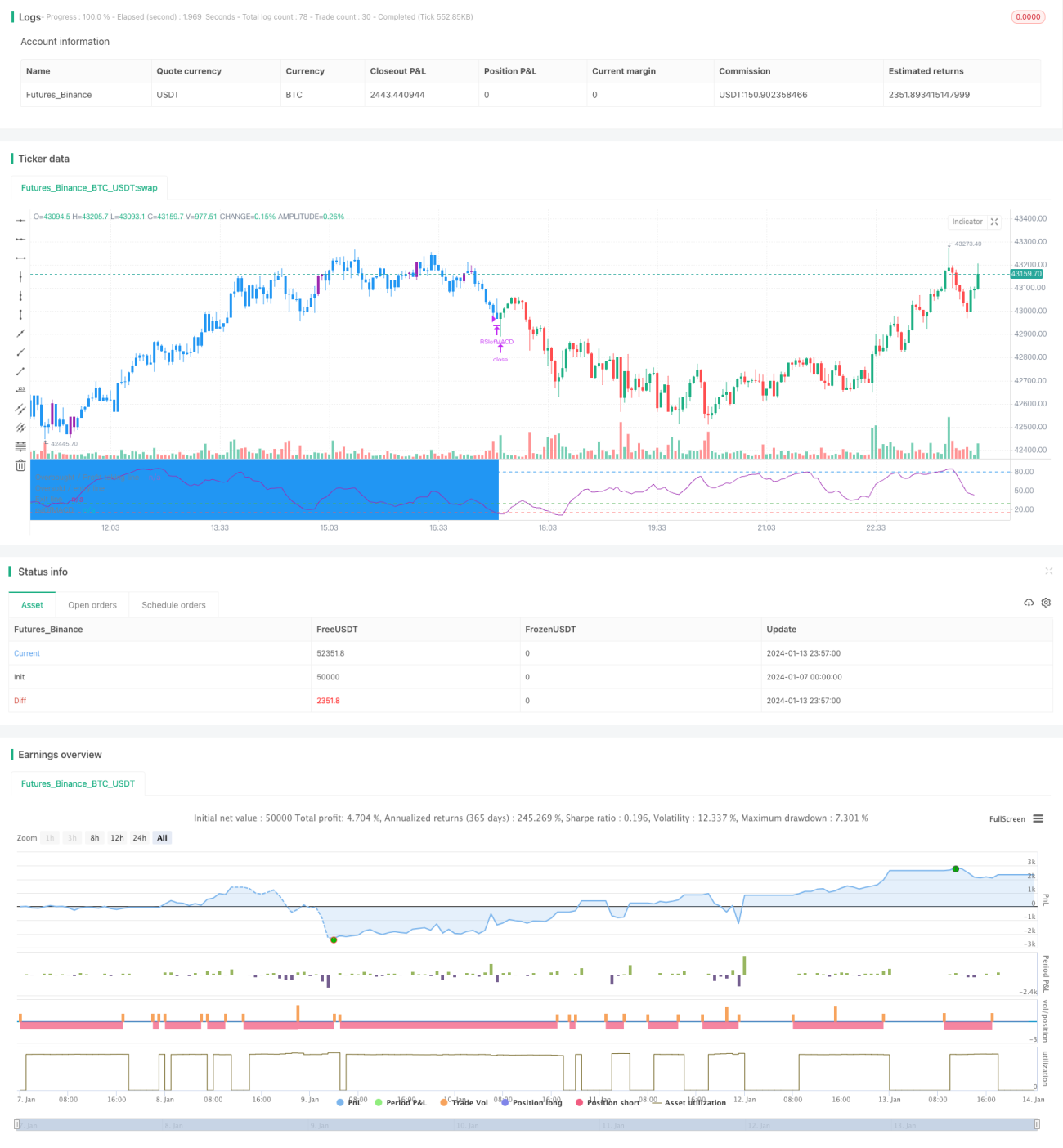

This strategy is based on the RSI values of the MACD indicator to determine buy and sell signals. It buys when the RSI exceeds the overbought line or range, and sells or stops profit/loss when the RSI breaks below the overbought range.

Strategy Principle

This strategy combines the advantages of both the MACD and RSI indicators.

First, the three curves of the MACD indicator are calculated, including the DIF, DEA and MACD lines. Then the RSI indicator is calculated on the MACD line to form the RSI of MACD.

When the RSI of MACD indicator exceeds the overbought range of 30 or 35, a buy signal is generated, indicating the MACD line has entered the oversold range and the price trend has started to reverse upwards. When the RSI of MACD indicator breaks below the overbought range of 15 again, a sell signal is generated, indicating the trend reversal has ended.

The strategy also sets partial profit taking. When the RSI of MACD indicator exceeds the overbought level of 80, part of the position can be sold to lock in partial profits.

Advantage Analysis

- Utilize MACD indicator to determine trend reversal points

- Utilize RSI indicator to determine overbought/oversold levels to filter fake signals

- Combination of dual indicators for accurate buy/sell points

- Partial profit taking set to prevent enlarged losses

Risk Analysis

- Inaccurate judgement of trend if improper MACD parameters

- Inaccurate judgement of overbought/oversold zones if improper RSI parameters

- Potentially missing greater upside if profit taking too aggressive

Solutions:

- Optimize MACD parameters to find best combination

- Optimize RSI parameters to improve accuracy

- Relax profit taking criteria properly to target greater returns

Optimization Directions

The strategy can also be optimized in the following aspects:

- Add stop loss strategy to further control downside risks

- Add position sizing module to gradually ramp up positions as price moves

- Integrate machine learning models trained on historical data to further improve buy/sell point accuracy

- Attempt running on shorter timeframes like 15m or 5m to improve strategy frequency

Conclusion

The overall strategy design philosophy is clear, with the core idea of using MACD reversal combined with RSI filter to determine buy/sell points. With parameter optimization, stop loss management, risk control measures etc., it can be shaped into a very practical quant trading strategy.

- 1