Trend Following Strategy Based on SSL Baseline

Overview

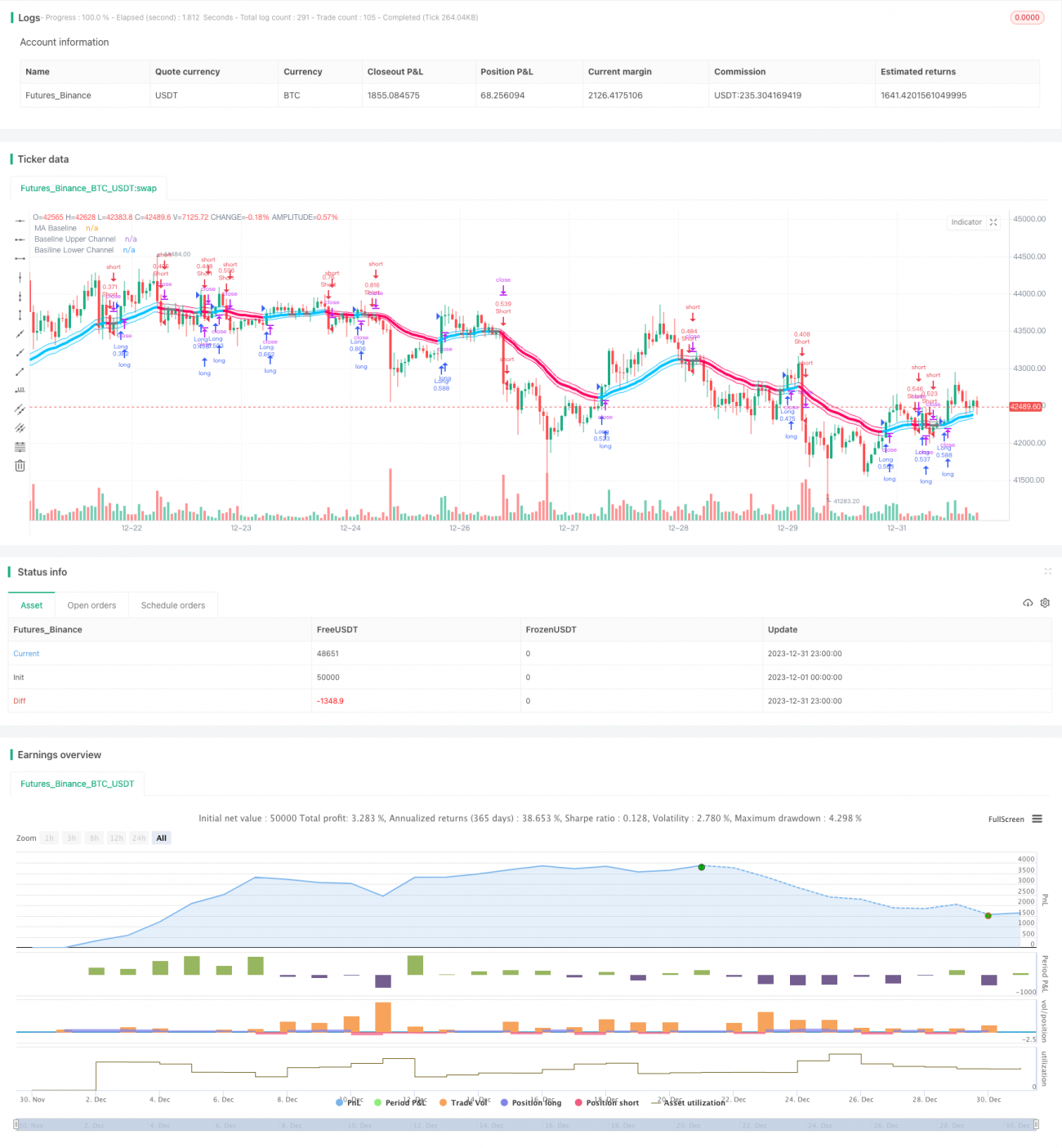

This strategy uses the SSL Channel to judge market trends and follows the trend based on moving average baselines. It is suitable for medium and long term timeframes like the 4-hour and daily charts.

Strategy Logic

-

The SSL Channel consists of Keltner Channels and True Range. It can determine the trend direction. A breakout above the upper band stands for a bullish signal while a breakout below the lower band stands for a bearish signal.

-

The strategy calculates a baseline with EMA and other MA indicators. This baseline filters some false breakouts.

-

The strategy goes long when price breaks above the SSL upper band and goes short when price breaks below the lower band. It follows uptrend by buying dips and downtrend by selling rallies.

-

Stop loss methods include percentage based, ATR based and looking back to highest high/lowest low. Take profit is a multiplier of stop loss. Specific parameters are determined by users.

Advantage Analysis

-

SSL Channel accurately judges trend direction with less false signals. Combining with MA lines as entry trigger avoids buying tops and selling bottoms.

-

Flexible MA types and parameters suit more market situations.

-

Flexible stop loss methods effectively control risks. Take profit multiplier also customizable for different preferences.

-

Ability to go both long and short makes full use of bilateral market opportunities.

Risk Analysis

-

Lagging of MA indicators may lead to accumulating losses.

-

Swift reversals after breaking SSL bands bring whipsaws in ranging markets.

-

ATR and look back stop loss may be too loose on anomalies, expanding losses.

Risk Management Tactics:

- Adjust MA parameters or use other types of MA.

- Expand stop loss percentage for timely stop loss.

- Add multiplier in ATR. Tune lookback cycle.

Optimization Direction

- Test more MA types to find optimal parameters.

- Optimize ATR cycle for stop loss.

- Test different stop loss multipliers.

- Test risk reward coefficient for take profit.

Conclusion

This strategy effectively follows trends by combining SSL Channel to determine trends and MA lines to confirm entry triggers. It provides flexible methods to stop losses and take profits, balancing risks and returns. Continuous testing and parameter tuning will lead to better performance. It is an efficacious strategy worthy of long term tracking and usage.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1