Multiplicative Moving Average Dual-direction Trading Strategy

Overview

This strategy calculates the multiplicative moving average line and combines the crossings of price and PMax indicator to determine the trend direction. It adopts dual-direction trading to long when trend goes up and short when trend goes down, evaluating position risk in real time to exit with profit.

Strategy Principle

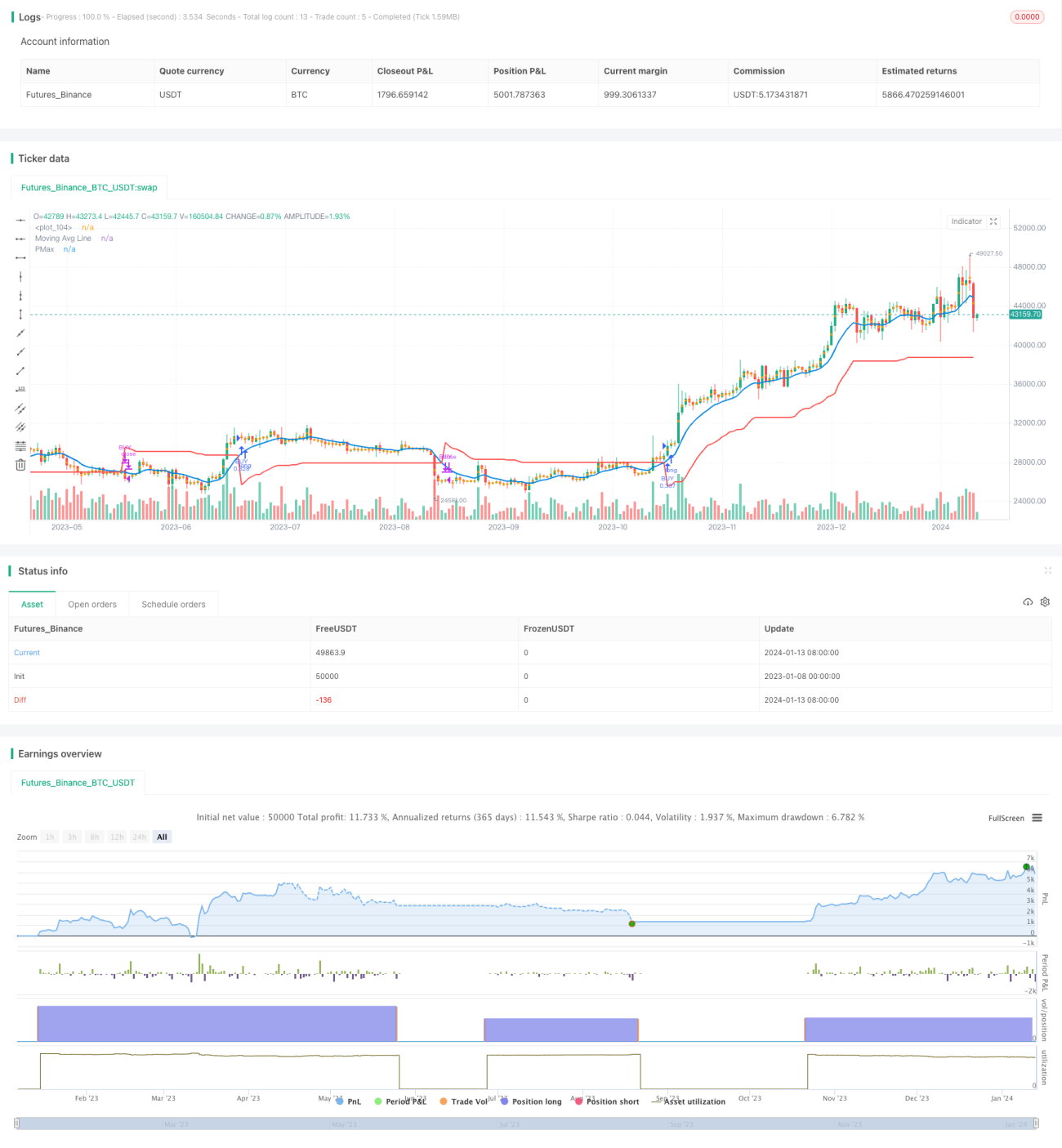

The core indicator of this strategy is the multiplicative moving average line. Indicator parameters include: ATR period, ATR multiplier, moving average type and length. The ATR value represents volatility over the period. The multiplicative moving average line equals average price plus/minus the product of ATR multiplier and ATR over the period. When price is above the line there is a long signal. When price is below the line there is a short signal.

The PMax indicator represents stop loss or take profit price. It is calculated from ATR value and trend direction. In uptrend, PMax equals moving average minus ATR multiplier times ATR, acting as a stop loss line. In downtrend, PMax equals moving average plus ATR multiplier times ATR, acting as a take profit line.

When price crosses PMax indicator upwards there is a long signal. When price crosses PMax indicator downwards there is a short signal. The strategy enters and exits based on the signals, going long in uptrend and short in downtrend, with dynamic trailing stop loss and take profit.

Advantage Analysis

The advantages of this strategy:

-

Adopting dual-direction trading makes it highly inclusive of all market conditions.

-

Applying multiplicative moving average produces stable and reliable trading signals.

-

With PMax for stop loss/take profit, it effectively controls risk.

-

The adjustable cycle and multiplier parameters make it highly adaptable.

Risk Analysis

There are also some risks:

-

Improper parameter settings may lead to whipsaw losses.

-

Pay attention to leverage limits when shorting.

-

Black swan events are hard to avoid.

Solutions:

-

Optimize parameters to reduce whipsaws.

-

Control leverage prudently and diversify.

-

Increase ATR multiplier to widen stop range.

Optimization Directions

The strategy can be upgraded in ways like:

-

Test stability across different markets and cycles.

-

Apply machine learning to auto optimize parameters.

-

Judge market regimes with deep learning techniques.

-

Integrate more data sources to empower decisions.

Summary

The overall performance of this strategy is stable with strong inclusiveness. By adopting dual-direction trade and dynamic stop loss/take profit, it effectively controls risks. Through parameter tuning and model iteration, strategy fitness and efficacy can be further improved. In general this is a strategy worth long-term attention and application.

/*backtest

start: 2023-01-08 00:00:00

end: 2024-01-14 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © melihtuna

//developer: @KivancOzbilgic

//author: @KivancOzbilgic- 1