Combination Strategy of 123 Reversal and Pivot Point

Overview

This strategy combines the 123 reversal pattern strategy and the pivot point strategy to achieve a higher win rate. The 123 reversal pattern strategy identifies trend reversal points, while the pivot point strategy determines key support and resistance levels. By combining the two, it can capture trends while identifying specific entry and exit prices.

Strategy Logic

123 Reversal Pattern Strategy

This strategy identifies trend reversal points using the Stochastic Oscillator indicator. Specifically:

It goes long when the close price is higher than the previous close for 2 consecutive days and the 9-period slow STO is below 50; It goes short when the close price is lower than the previous close for 2 consecutive days and the 9-period fast STO is above 50.

Pivot Point Strategy

This strategy calculates 3 support levels and 3 resistance levels based on the previous day's high, low and close prices. The calculations are:

Pivot Point = (High + Low + Close)/3

Support 1 = 2Pivot Point – High

Resistance 1 = 2Pivot Point – Low

Support 2 = Pivot Point – (Resistance 1 – Support 1)

Resistance 2 = Pivot Point + (Resistance 1 – Support 1)

Support 3 = Low – 2*(High – Pivot Point)

Resistance 3 = High + 2*(Pivot Point – Low)

It then identifies entry and exit based on the support and resistance levels.

Advantages

- Combines the strengths of two different types of strategies to achieve higher win rate

- The 123 pattern effectively identifies short-term trend reversals

- Pivot points use key S/R levels to filter false breaks

Risks and Hedging

- The double STO may lag and miss short-term reversals

- Pivot points may not always hold, breakouts can continue

- Parameters can be adjusted or combined with other indicators to hedge risks

Optimization Directions

- Test impacts of different parameter sets

- Combine with other indicators/patterns to improve performance

- Incorporate machine learning to dynamically optimize parameters

Summary

This strategy ingeniously combines trend identification and key price levels, enabling it to spot reversals while utilizing S/R to filter signals. Further improvements can be made through parameter tuning and combination with other strategies. It deserves more research and application by quant traders.

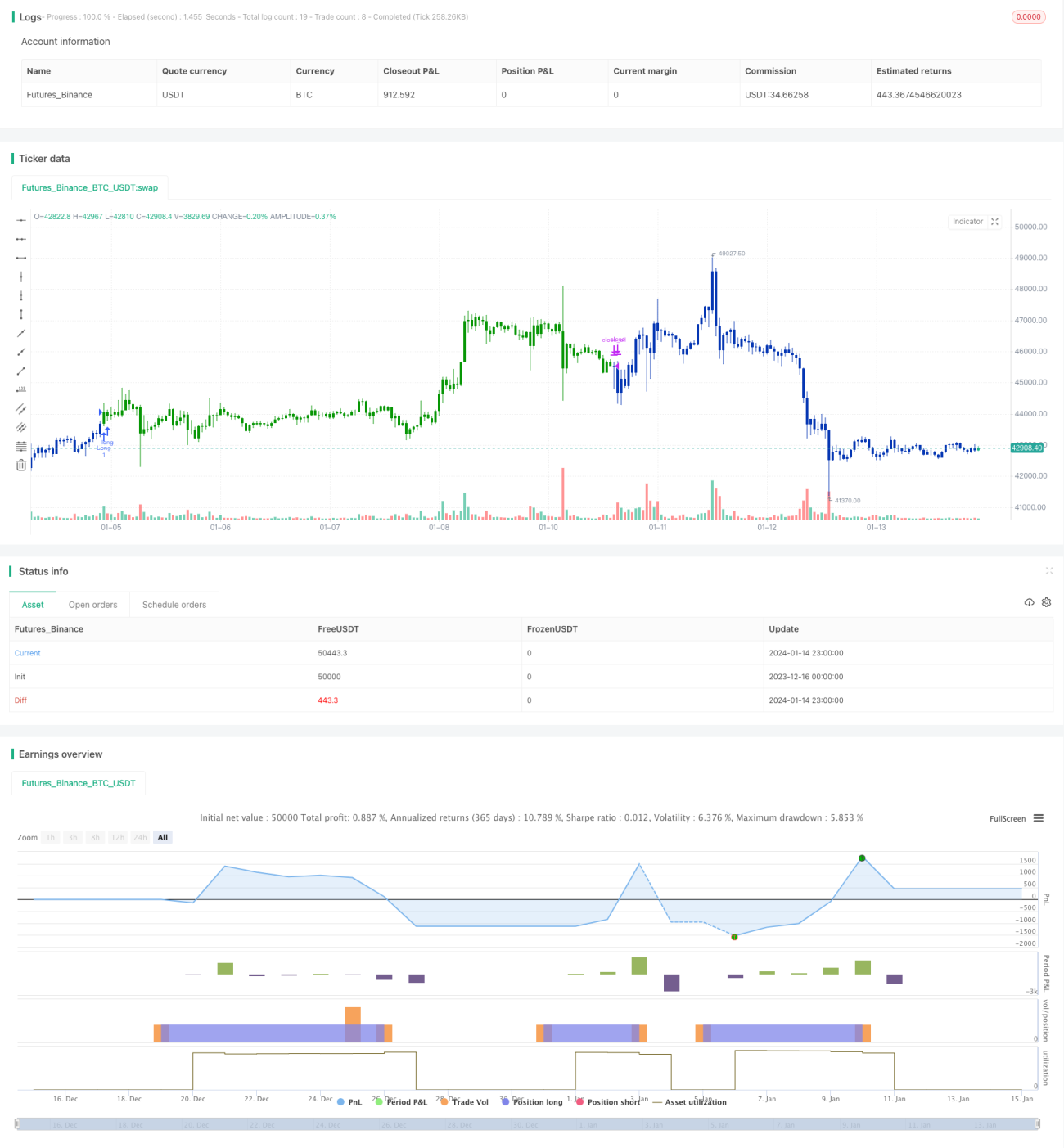

/*backtest

start: 2023-12-16 00:00:00

end: 2024-01-15 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 21/04/2021

// This is combo strategies for get a cumulative signal. - 1