Ichimoku Kinko Hyo Breakout Strategy

I. Strategy Overview

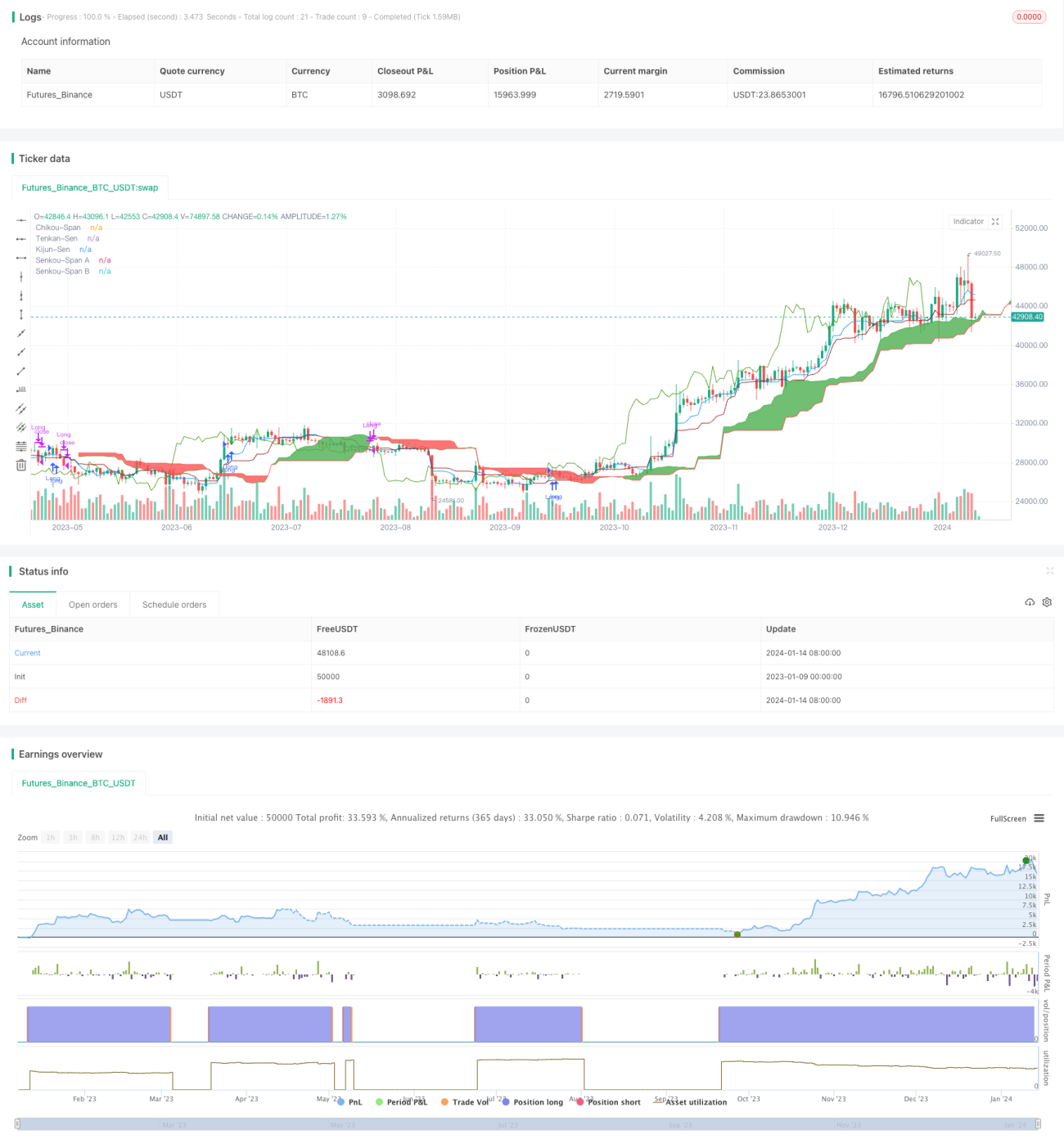

The strategy is named "Ichimoku Kinko Hyo Indicator Based Breakout Strategy". It utilizes the Tenkan-Sen, Kijun-Sen lines, Senkou Span lines and Kumo cloud from the Ichimoku Kinko Hyo indicator to determine the trend direction and implement breakout entry and exit signals.

II. Strategy Details

-

Calculate the components of the Ichimoku Kinko Hyo indicator:

- Tenkan-Sen: middle of highest and lowest prices

- Kijun-Sen: middle of highest and lowest prices

- Senkou Span A: middle of Tenkan-Sen and Kijun-Sen

- Senkou Span B: middle of highest and lowest prices

- Chikou Span: lagging span

-

Determine long signal:

- When Tenkan-Sen cross above Kijun-Sen;

- And close price break above the Kumo cloud;

- And Chikou Span break above the Kumo cloud.

-

Determine short signal:

- When Tenkan-Sen cross below Kijun-Sen;

- And close price break below the Kumo cloud;

- And Chikou Span break below the Kumo cloud.

III. Advantage Analysis

- Ichimoku Kinko Hyo is accurate in determining trends.

- Chikou Span avoids false breakouts.

- Allow long and short trading in both uptrend and downtrend.

- Customizable parameters for different periods.

IV. Risk Analysis

- Frequent losing trades during market consolidation.

- Missing best entry points due to multiple criteria.

- High turnover rate increases transaction costs.

Solutions

- Adjust parameters to avoid overtrading.

- Combine with other indicators to confirm signals.

- Extend holding period to decrease turnover.

V. Optimization Directions

- Add moving averages to confirm trading signals.

- Implement stop loss to limit downside risk.

- Optimize parameters to improve robustness.

VI. Strategy Summary

The strategy determines trend direction accurately using Ichimoku Kinko Hyo indicators and takes breakout signals as entry and exit points, allowing long and short trading. Compared with single indicator strategies, it has higher accuracy and avoids many false signals. There is also some lagging in capturing best entry price. In conclusion, the strategy is quite effective in determining trends and the risks are manageable. Further optimizations and walk-forward testing are recommended.

- 1