RSI Target and Stop Loss Tracking Strategy

Overview

This strategy uses the RSI indicator to generate buy and sell signals, combined with tracking stop profit and stop loss mechanisms to achieve the purpose of fixed profits and risk control. The strategy is suitable for medium and short term trading, with flexible and practical characteristics.

Strategy Principle

-

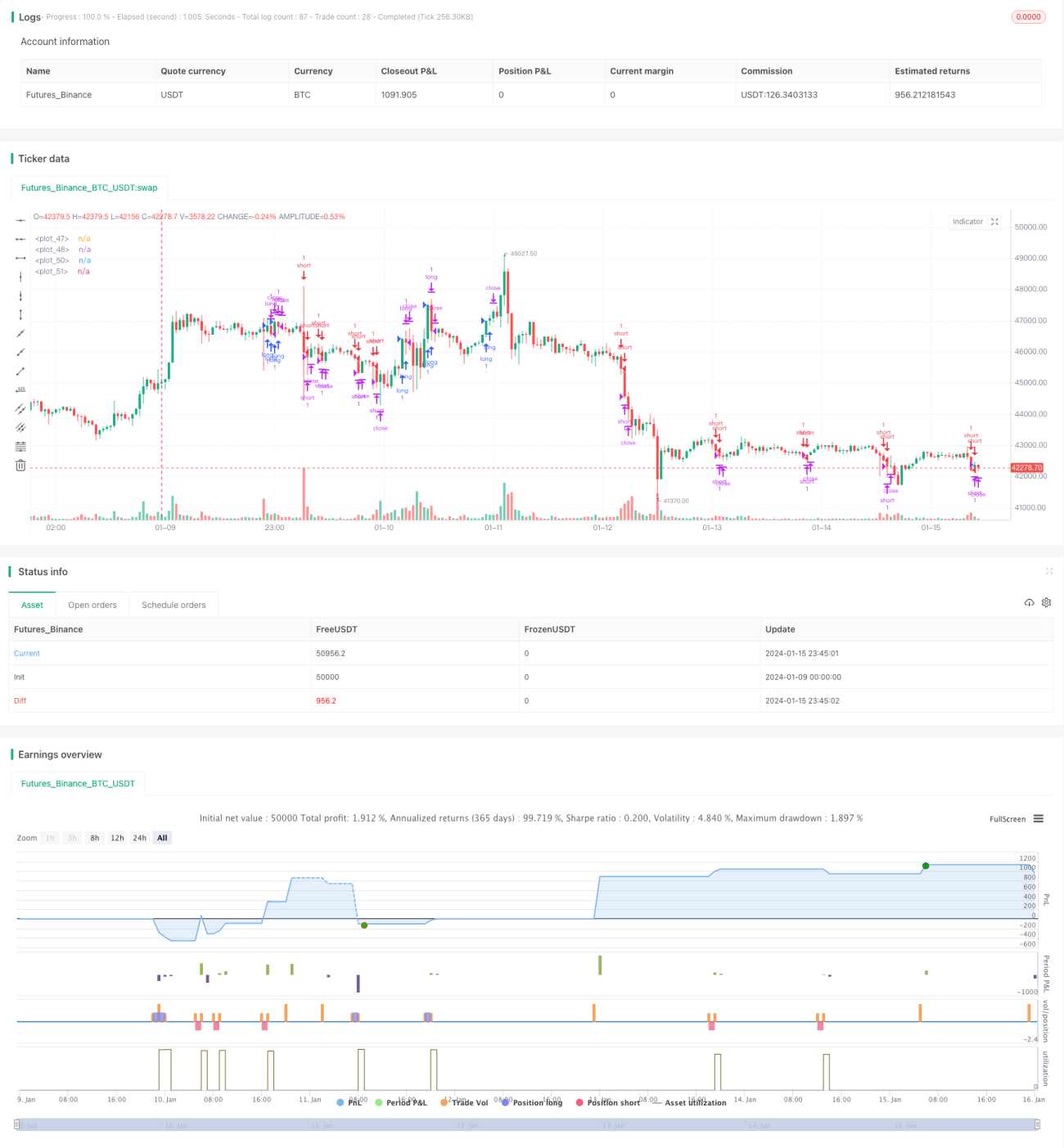

Use the RSI indicator to judge overbought and oversold conditions in the market. A buy signal is generated when the RSI crosses above 60, and a sell signal is generated when it crosses below 40.

-

After entering the market, set tracking stop profit and stop loss. The profit distance is the entry price plus the number of points set by the user, and the loss distance is the entry price minus the number of points set by the user.

-

When the price reaches the profit or loss distance, the trade stops profit or loss automatically.

Advantage Analysis

-

The RSI indicator works well in judging market trends, combined with tracking stop loss and profit taking, it can effectively control risks.

-

The profit and loss distances are set in absolute number of points. No matter the entry price is high or low, the profit space and loss space are fixed, and the risk reward ratio is controllable.

-

The strategy parameter setting is simple. Users only need to set the number of points for stop profit and stop loss based on their own risk preferences, without complicated optimization.

Risk Analysis

-

RSI indicators may generate false signals, resulting in unnecessary losses. False signals can be reduced by adjusting RSI parameters or adding other indicators for filtration.

-

Fixed stop profit and loss distances can lead to insufficient profit space or excessive losses. Users need to reasonably set stop profit and loss distances according to market volatility.

-

Tracking stop loss may be broken in extreme market conditions, unable to limit the maximum loss. It is recommended to combine temporary stops to reduce risks.

Optimization Direction

-

Optimize RSI parameter to find the best parameter combination.

-

Add MA and other indicators to filter RSI signals and reduce unnecessary trades.

-

Set stop profit and loss ratio instead of absolute number of points, which can automatically adjust distances based on price.

-

Add temporary stops to prevent risks in extreme market conditions.

Summary

This strategy uses the RSI indicator to determine the timing of buying and selling, and uses tracking stop profit and loss to control risks and returns. The strategy is simple and practical. Parameters can be adjusted based on market and personal risk preferences. Combined with multi-indicator judgments and stop loss optimization, the stability and profitability of the strategy can be further enhanced.

- 1