Extreme Short-term Scalping Strategy

Overview

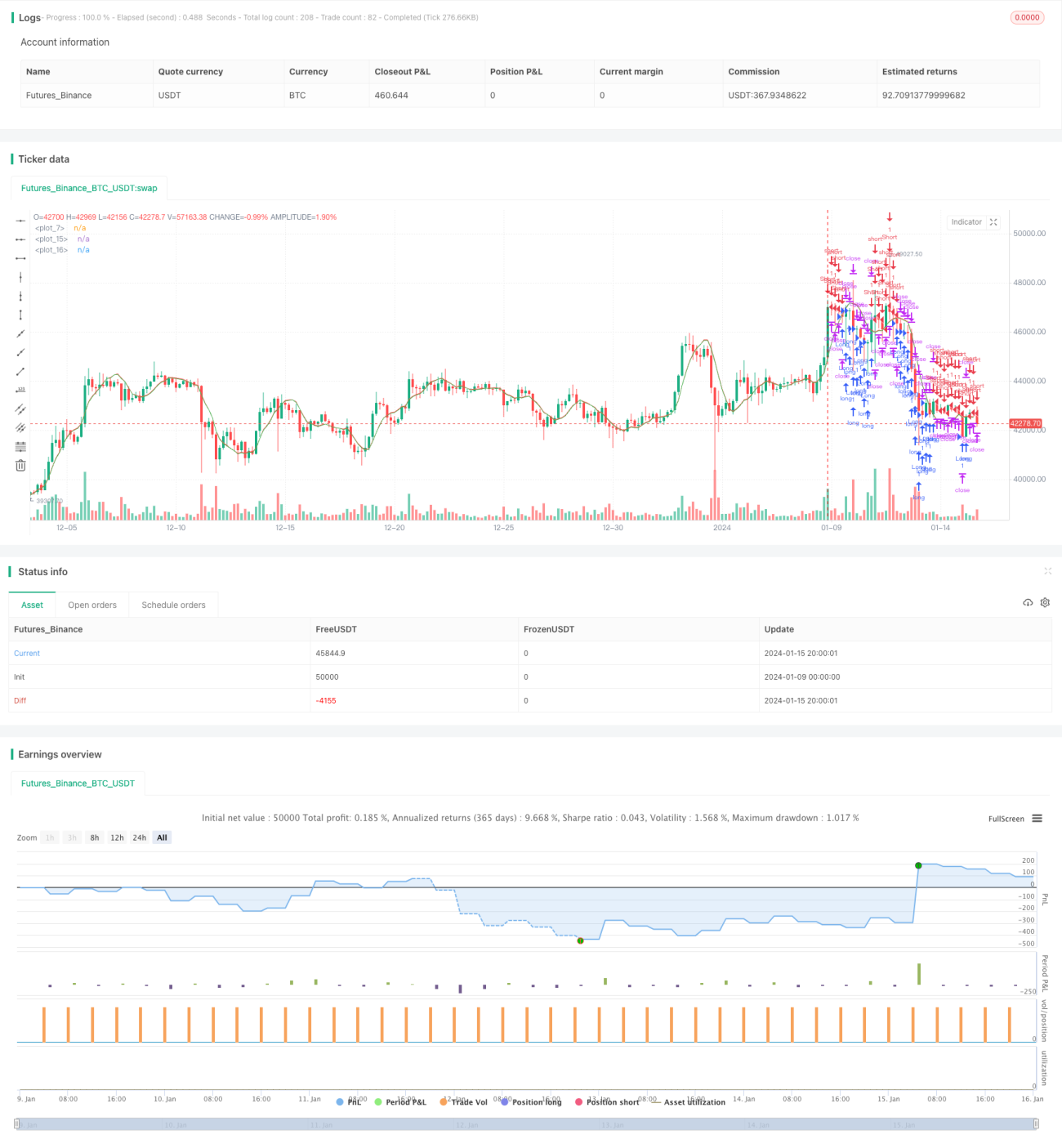

The extreme short-term scalping strategy attempts to establish short positions when prices approach or break support lines and sets very small stop loss and take profit levels for high frequency trading. The strategy exploits short-term price breakthroughs to capture market fluctuations for profits.

Strategy Logic

The strategy first calculates the linear regression line of prices. If the actual closing price is lower than the forecast closing price, long positions are established. If the actual closing price is higher than the forecast closing price, short positions are established. Stop loss and take profit are set to very small number of pips. The strategy allows choosing only long, only short or all direction trading.

Key parameters include:

- Source price: closing price

- Length of linear regression line: 14

- Offset: 1

- Trading direction: all/only buy/only sell

- Stop loss and take profit in pips: very small fixed pips or minimum tick pips

The main idea of the strategy is to capture short-term price breakthroughs of moving averages. When prices approach or break through support or resistance lines, timely establish positions. And set very small stop loss and take profit to realise profit then close positions immediately, repeating the process.

Advantage Analysis

The strategy has the following advantages:

- High trading frequency, suitable for high frequency trading, can capture more short-term price fluctuations

- Very small stop loss and take profit helps control single loss

- Can flexibly choose trading direction to adapt to different market environments

- Easy to implement with simple logic

Risk Analysis

There are also some risks:

- Price gaps may lead to expanded losses

- High transaction costs

- Signal errors may happen and need timely attention and optimisation

- Requires continuous market monitoring

Corresponding risk management measures include:

- Disable overnight trading

- Optimise stop loss and take profit to reduce transaction cost impacts

- Test and optimise parameters to reduce wrong signals

- Pay close attention to the market

Optimisation Directions

Further optimisation directions include:

- Add other indicators to filter signals and reduce wrong trades

- Dynamically adjust stop loss and take profit

- Optimise parameters to reduce overfitting

- Consider transaction cost impacts for reasonable stop loss and take profit configuration

- Test stability across products and timeframes

Summary

The extreme short-term scalping strategy is a typical high frequency trading strategy. By establishing positions around key price levels and setting very small stop loss and take profit, it captures short-term price fluctuations. Although it can achieve high returns, there are also certain risks. With continuous testing and optimisation, the strategy can be further enhanced for stability and profitability.

- 1