Price Reversal with Crossover Capturing Strategy

Overview

The price reversal with crossover capturing strategy is a compound strategy that combines price reversal trading techniques and indicator crossovers. It first generates trading signals using price reversal patterns, then filters the signals with overbought/oversold crossovers of a stochastic oscillator, in order to capture short-term reversals in the market.

Strategy Logic

The strategy consists of two sub-strategies:

- 123 Reversal Strategy

- When the close price turns from higher to lower in two days, and the 9-day stochastic indicator is at lower band (below a threshold), a buy signal is generated

- When the close price turns from lower to higher in two days, and the 9-day stochastic indicator is at upper band (above a threshold), a sell signal is generated

- Stochastic Crossover Strategy

- When the %K line crosses below the %D line, while both lines are in overbought levels, a sell signal is generated

- When the %K line crosses above the %D line, while both lines are in oversold levels, a buy signal is generated

The compound strategy checks the signals from both sub-strategies and only triggers actual trades when the signals align in the same direction.

Advantages

The strategy combines price reversal patterns and indicator crossovers to evaluate both price action and indicator information, which helps filter out false signals and uncover reversal opportunities to improve profitability.

Specific advantages include:

- Capturing market reversals quickly without long consolidation waits

- Increased signal accuracy with dual validation from both sub-strategies

- Better win rate combining analysis of both price action and indicators

Risks

There are also some risks with this strategy:

- Price may reverse abruptly during high volatility, causing incorrect signals

- Poor indicator parameter tuning affects signal quality

- Unsure about reversal timing, some time risk exists

These risks can be managed by adjusting parameters, using stop losses etc.

Enhancement Opportunities

Some ways the strategy can be enhanced:

- Optimize indicator parameters

- Add other filters like volume

- Customize parameters based on symbol and market conditions

- Incorporate stop loss for risk control

- Employ machine learning for signal identification

Conclusion

The price reversal with crossover capturing strategy combines multiple complementary strategies to profit while controlling risks. With continuous improvements, it can be tailored into an efficient strategy that thrives in changing markets.

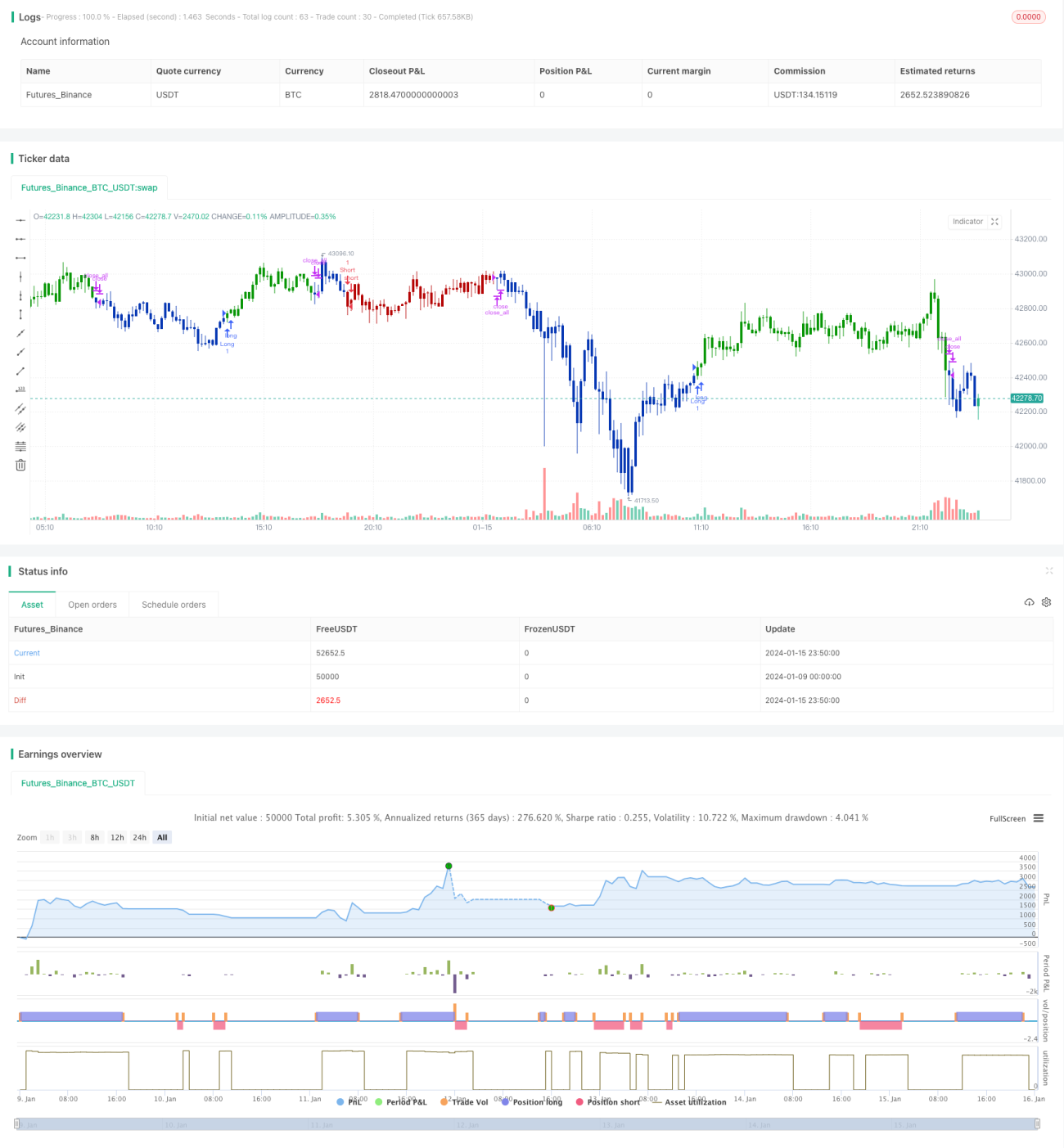

/*backtest

start: 2024-01-09 00:00:00

end: 2024-01-16 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/09/2021

// This is combo strategies for get a cumulative signal. - 1