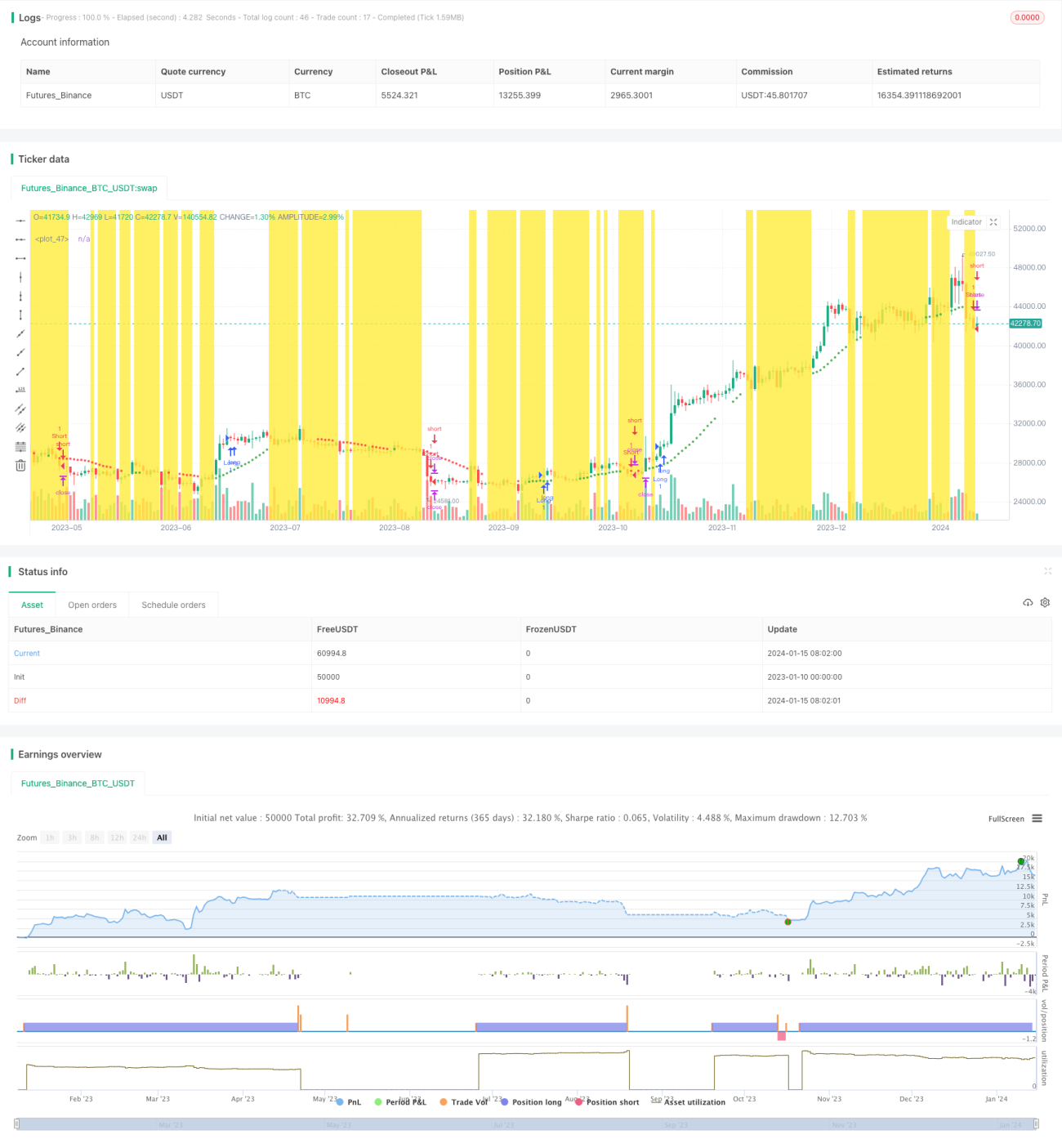

Baseline Cross Qualifier ATR Volatility & HMA Trend Bias Mean Reversion Strategy

Overview

This strategy integrates the baseline mean reversion signal, ATR volatility filter, and HMA trend filter to generate robust trading signals for quantitative trading strategies. It uses two moving averages with different periods to construct trading signals, combines the ATR volatility indicator to filter out some invalid signals, and utilizes HMA to determine the major trend direction to avoid adverse selection.

Strategy Logic

The strategy uses a 37-period moving average as the baseline. When the price breaks out upward from this baseline, it generates a buy signal, and when it breaks down from above, it generates a sell signal. To avoid false signals, the strategy requires the price to move beyond 2xATR volatility after penetrating the baseline to confirm the validity of signals. Also, the strategy uses an 11-period HMA to judge the major trend. It only confirms valid signals when price penetrating baseline is aligned with HMA direction to prevent adverse selection.

For profit taking, the strategy supports using one or multiple (two or three) take profit levels. For stop loss, it simply takes the upper and lower band lines as SL for long and short positions.

Advantage Analysis

Compared with simple moving average breakout strategies, this strategy adds the ATR volatility filter that removes a lot of invalid signals. This aligns very well with visual pattern breakout techniques, thus leading to higher win rates. Also, the HMA trend bias prevents adverse selection and significantly reduces unnecessary losses. The multiple take-profit scheme also allows more profits to be locked in.

Risks & Solutions

The major risk is the ATR volatility filter may remove some valid signals, causing failure to open positions timely. Also, the HMA trend judgment is not very significant sometimes when price is just having a short-term retracement, not reversal. This may lead to unnecessary stop loss. To reduce the risks, we can lower the ATR volatility filter parameter to allow more signals. We can also adjust the HMA period parameter to use longer-term HMA for judging major trends, preventing interference from short-term fluctuations.

Optimization Directions

The strategy can be optimized in the following aspects:

-

Test more parameter combinations to find the optimum set of values, e.g., baseline period, ATR period, volatility coefficient etc.

-

Add more filters or oscillators to judge market conditions to enhance model robustness.

-

Optimize parameters for profit taking mechanisms, test more price levels and allocation schemes.

-

Incorporate machine learning models to generate more effective trading signals.

Conclusion

This strategy integrates dual moving average baseline signal, ATR volatility filter and HMA trend bias filter into a very practical quantitative trading system. Although it still has space to enhance performance through parameter tuning, it already serves well for disciplined rule-based trading.

- 1