Dual Confirmation Reversal Trend Tracking Strategy

Overview

The dual confirmation reversal trend tracking strategy integrates the 123 reversal pattern strategy and the support/resistance breakout strategy to realize double confirmation of price reversal signals and filter out some noisy trading signals, thus improving the win rate of the strategy.

It is mainly used for medium-to-long term trading. When the price forms a reversal signal, it will detect whether the key support or resistance level is broken out at the same time. Trading signals are generated only after double confirmation.

Strategy Principle

The dual confirmation reversal trend tracking strategy consists of two parts:

-

123 reversal pattern strategy

By comparing the closing prices of the previous two candlesticks, determine whether the price has formed a reversal pattern. Combined with the stochastic indicator to determine the oscillation to filter out false opportunities.

-

Support/Resistance Breakout Strategy

Use the highest price, lowest price and closing price of the previous day to calculate the support and resistance levels. Monitor whether the price breaks through these key levels.

When the price meets the trading signals of both strategies at the same time, the reversal signal is considered to be double confirmed and the final trading order is generated.

Advantages of the Strategy

- Higher reliability with dual signal confirmation

- Timely capture turnaround opportunities with reversal tracking

- Effective fake breakout filtering with stochastic indicator

Risks of the Strategy

- A small number of opportunities are filtered out due to dual confirmation

- Risk of reversal failure under major trends

Parameters can be optimized to adjust the strictness of dual confirmation and balance the win rate and number of profitable trades.

Optimization Directions

- Adjust stochastic parameters to optimize oscillation filtering

- Test different timeframes for calculating support/resistance levels

- Add stop loss strategy to reduce reversal risk under major trends

Conclusion

The dual confirmation reversal trend tracking strategy successfully combines the advantages of reversal patterns and key level breakouts. While improving signal quality, it also ensures the number of trades. It is a suitable strategy for medium-to-long term trend trading. The addition of parameter tuning and stop loss strategies can further enhance the stability and practicability of the strategy.

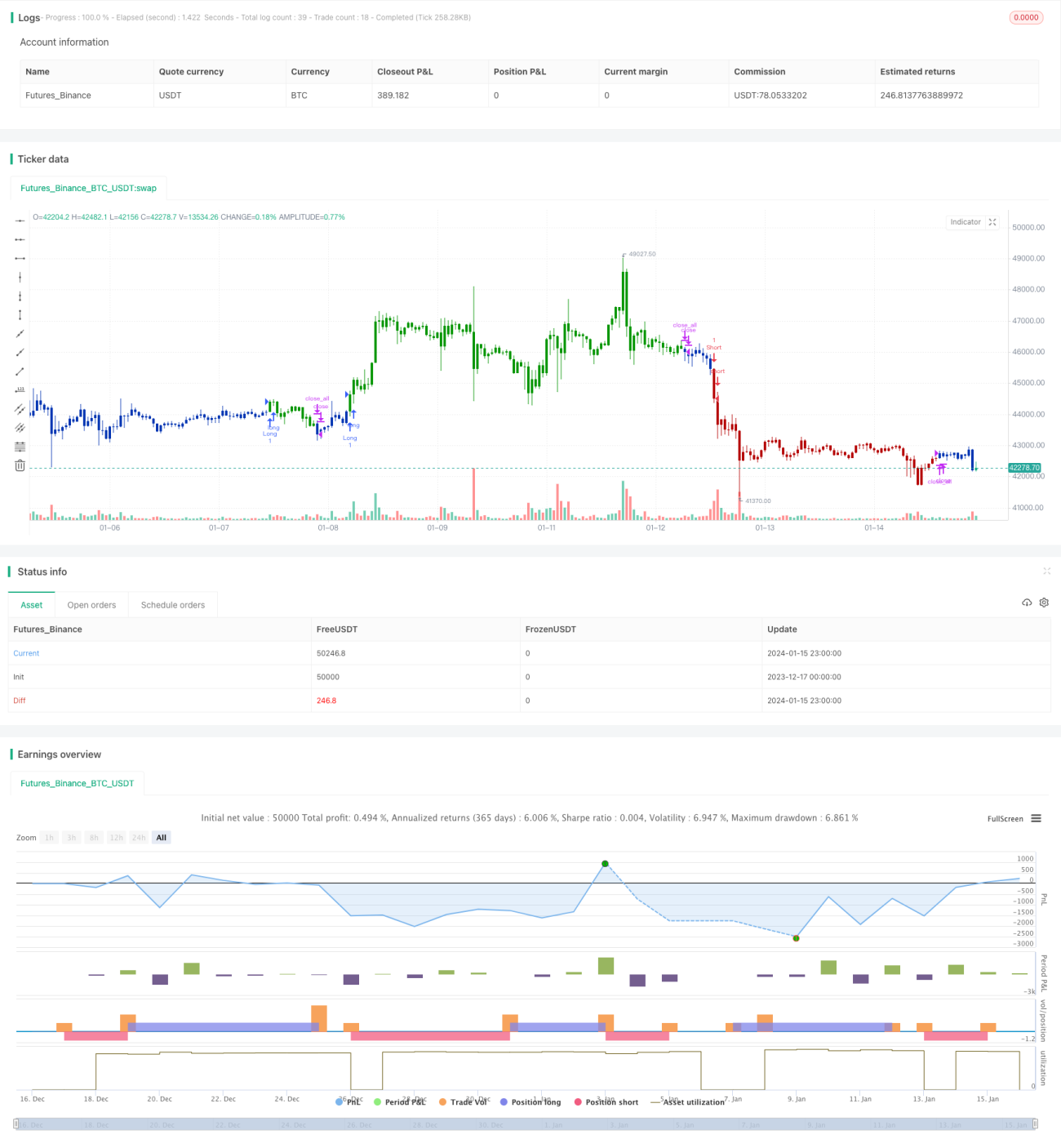

/*backtest

start: 2023-12-17 00:00:00

end: 2024-01-16 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/09/2020

// This is combo strategies for get a cumulative signal. - 1