Dual-Factor Momentum Tracking Reversal Strategy

Overview

This strategy combines the price reversal factor and momentum factor of stocks to construct a dual-factor model for capturing opportunities arising from short-term reversals and long-term persistence in the market. It first uses 123 chart patterns to determine near-term price reversal signals, then incorporates the Laguerre RSI indicator to judge the medium-to-long term trend, and eventually achieves effective integration of dual-factor signals.

Strategy Principles

The strategy consists of two parts:

-

123 Reversal Pattern Factor

This part detects short-term price reversal signals by examining the change in closing prices over the past two days. Specifically, if yesterday's closing price is lower than the previous two days' and today's closing price is higher than yesterday's, it can be determined as a bullish price reversal signal. The Stoch indicator serves as an auxiliary means to assist judgement.

-

Laguerre Filtered RSI Factor

This part builds a more responsive RSI indicator using Laguerre filters. The sensitivity of traditional RSI indicators to price changes is relatively low. By contrast, Laguerre filters can construct indicators using less historical data, thereby improving sensitivity to price fluctuations. The new RSI indicator is used to determine the medium-to-long term trend.

Ultimately, the strategy combines the signals from both factors, ensuring short-term reversals occur in alignment with overall market trends, in order to capitalize on retracement opportunities.

Advantages of the Strategy

The biggest advantage of this strategy lies in the successful combination of reversal and trend factors. The reversal factor captures short-term pullback opportunities after price consolidations, while the trend factor ensures the overall long/short bias does not change. Compared to standalone reversal or momentum models, this dual-factor model can improve the accuracy of long/short signals while lowering false signals.

Additionally, the introduction of the Laguerre RSI boosts the model's sensitivity to price changes, which is especially crucial for high-frequency trading.

Risk Analysis

The primary risk this strategy faces is the possibility of conflicting signals from the two factors. Particularly during volatile market corrections, short-term prices may reverse frequently while medium-to-long term trends also begin to shift. In such cases, the two types of signals can easily mismatch or experience delays. This leads to incorrect strategy signals and missed entry opportunities or unnecessary losses.

In addition, poor parameter configurations may also lead to poor strategy performance. The parameters for the technical indicators belonging to the reversal and trend factors need to be separately optimized and tested. Improper parameter combinations can significantly diminish the strategy's efficacy.

Optimization Directions

The main focuses of future optimizations for this strategy involve signal filtering and parameter selection. More filtering conditions could be introduced to take effect when the dual-factor signals conflict, ensuring trades are only placed in high-certainty scenarios. This can drastically reduce false signals.

For parameter selection, machine learning and scientific experiment methods could be attempted to systematically test various parameter combinations and arrive at optimal configurations. This requires considerable computing power but can significantly improve the stability of the strategy.

Summary

This strategy has successfully merged reversal and trend factors through a dual-factor model to capitalize on short-term pullbacks and medium-to-long term persistence. The introduction of the Laguerre filtered RSI also improves model sensitivity to price changes. The next phase shall focus on signal filtering and parameter optimization to further enhance the strategy.

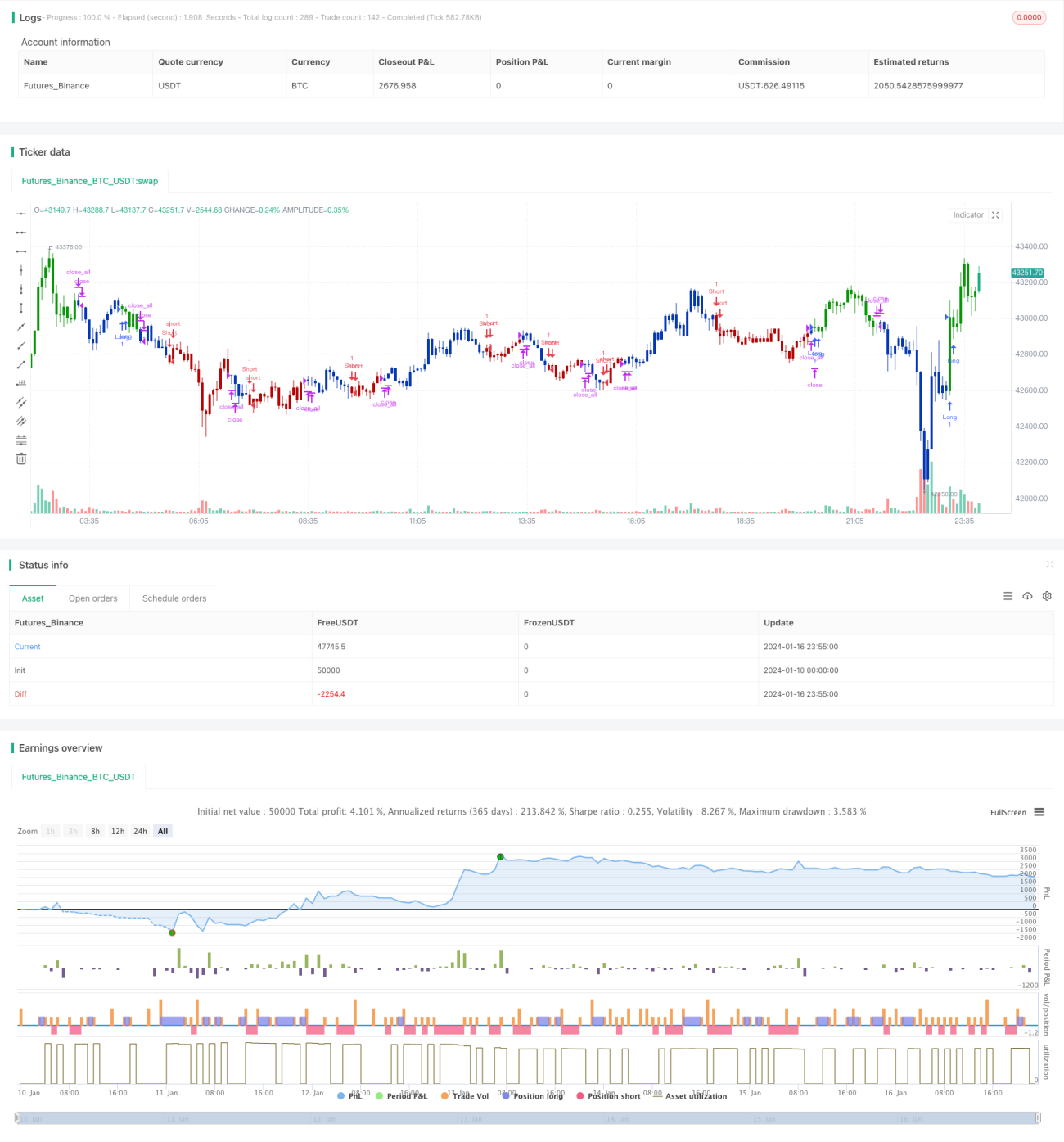

/*backtest

start: 2024-01-10 00:00:00

end: 2024-01-17 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 21/01/2021

// This is combo strategies for get a cumulative signal. - 1