Short-term Trading Strategy Based on Stochastic Index

Overview

This strategy designs a short-term trading strategy based on the Stochastic Index (SMI) indicator, mainly for short-term trading of stocks and digital currencies. The strategy integrates the overbought and oversold signals of the Stochastic Index indicator and the confirmation of moving averages to capture better entry points during intermediate pullbacks in a trending market.

Strategy Principle

The strategy mainly uses the Stochastic Index indicator to judge the overbought and oversold zones of the market. The calculation formula of the Stochastic Index indicator is:

SMI = (MA(Close - LL)/(HH - LL)) * 100

Where LL is the lowest price in N days, HH is the highest price in N days. The design concept of this indicator is that when the closing price is close to the highest price in N days, the market is in an overbought state; when the closing price is close to the lowest price in N days, the market is in an oversold state.

In this strategy, the SMA parameter N takes 5 and 3, indicating that the 5-day and 3-day Stochastic Index are used. Usually, using only one parameter can easily generate wrong signals. Therefore, this strategy adopts double SMA double confirmation, which can filter out some noise.

In addition, the EMA indicator is superimposed in the strategy, and the parameters are set to be consistent with the SMI indicator to further confirm the signals of the SMI indicator and avoid misjudgment.

Advantages of the Strategy

- Judge overbought and oversold areas based on Stochastic Index indicator to capture reversal opportunities

- Double SMA parameter settings can effectively filter out wrong signals

- Combining with EMA indicator for confirmation to avoid misjudgment

Risks of the Strategy

- The SMI indicator is prone to generating wrong signals. Even with double SMA and EMA indicators, the risks cannot be completely avoided.

- In a trending market, this strategy may generate too many reverse operations, thus affecting the overall profit.

Risk Prevention:

- Use stop loss to control single loss

- Only use this strategy in sideways or range trading markets to avoid using it in trending markets

Optimization Directions

- Test SMI indicators under different parameter settings to find the optimal parameter combination

- Try to combine with other indicators for confirmation, such as Bollinger Bands, KDJ, etc., to improve signal accuracy

- Optimize stop loss strategies and set variable stop loss based on market volatility

- Combine with trend judgment indicators to avoid using during trending markets

Summary

In general, this is a strategy suitable for short-term trading. It combines the overbought and oversold characteristics of the Stochastic Index indicator with moving average confirmation and filtering to identify some short-term trading opportunities. However, this strategy is prone to generating wrong signals in trending markets, so special attention needs to be paid when using it. It is best to use it with trend judgment indicators to avoid such situations. In general, this strategy can capture some short-term trading opportunities during range-bound markets, but attention needs to be paid to risk control and stop-loss exits during use.

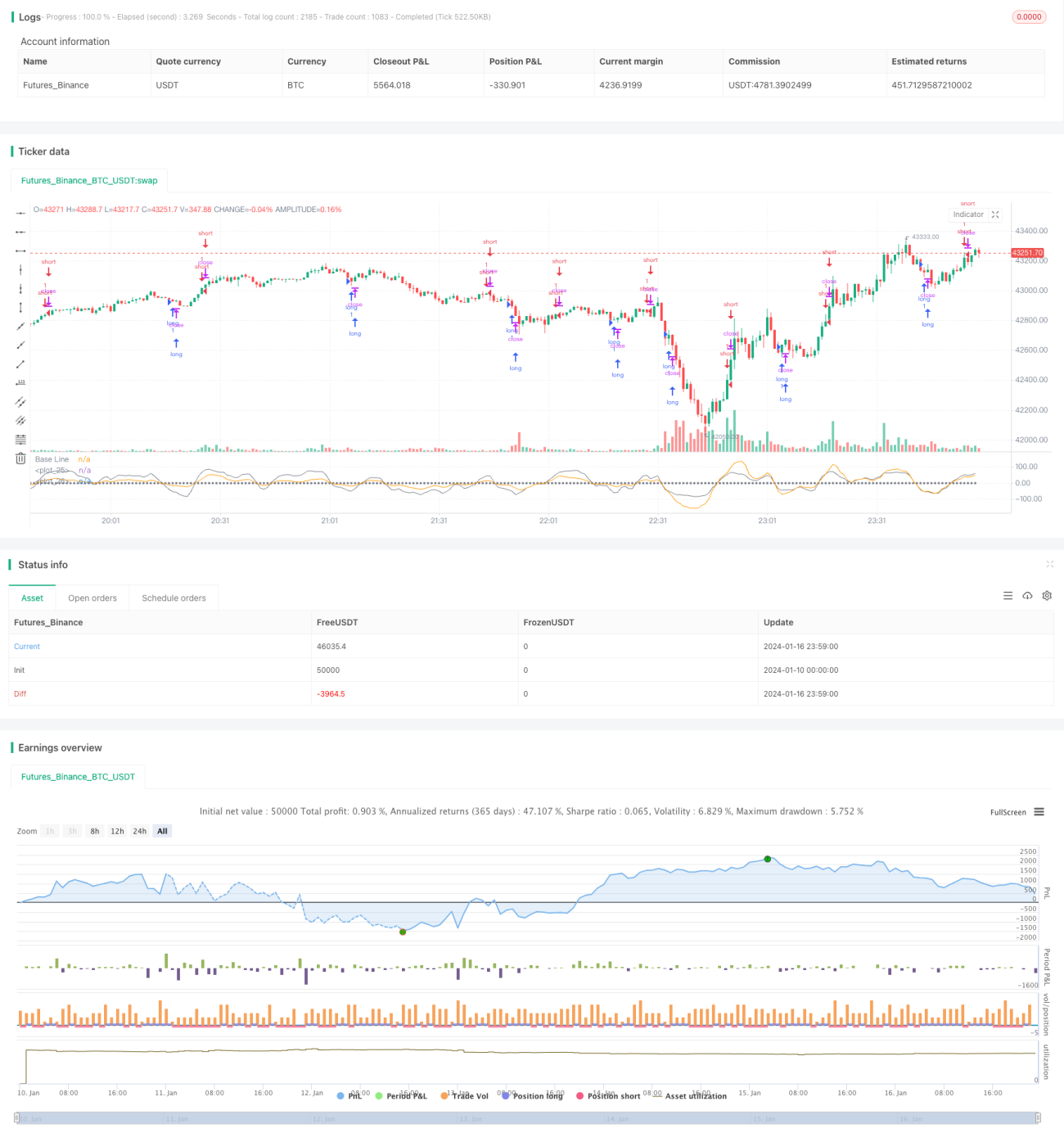

/*backtest

start: 2024-01-10 00:00:00

end: 2024-01-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title="SMIndex Strategy", shorttitle="SMIndex Strategy", overlay=false, pyramiding=0, initial_capital=1000, currency=currency.USD)

//

sm1 = input(5, 'sm1')- 1