Trend Following Trading Strategy Based on T3 Indicator

Strategy Overview

This strategy designs a trend following trading system based on the T3 moving average indicator. It can automatically identify the direction of price trends and take corresponding long or short positions. It goes long when prices rise and goes short when prices fall. The system also has the function of reversal trading.

Strategy Logic

The strategy uses the T3 indicator to determine the direction of the price trend. The T3 indicator is an adaptive moving average with higher sensitivity that can respond to price changes faster. Its calculation formula is:

T3(n) = GD(GD(GD(n)))

Where GD represents the generalized DEMA (double exponential moving average), which is calculated as:

GD(n,v) = EMA(n) * (1+v)-EMA(EMA(n)) * v

v is the volume factor, which determines the sensitivity of the moving average's response to linear price trends. When v=0, GD=EMA; when v=1, GD=DEMA. The author suggests setting v=0.7.

The strategy compares the T3 indicator with the price. When T3 crosses above the price, it determines an upward price trend and goes long. When T3 crosses below the price, it determines a downward price trend and goes short.

Advantages

- Uses adaptive moving average T3 indicator, sensitive to price trend changes

- Automatically determines price trend direction, no manual judgment needed

- Configurable reversal trading, flexible to cope with market changes

Risks

- T3 indicator may have difficulty determining trend direction during range-bound consolidation

- Adaptive moving average indicators tend to produce false signals

- Risk control for reversal trading needs to be cautious

This can be mitigated by adjusting T3 parameters or adding other indicators for filtration, as well as setting stop loss to control single loss.

Optimization Directions

- Add other indicators for filtration, such as MACD, RSI etc for combination

- Add trend judgment rules to avoid false operations during sideways markets

- Optimize parameters, adjust v value for better parameter combination

- Add stop loss logic

Summary

The strategy automatically determines the price trend direction through the T3 indicator, without the need for manual judgment, and can automatically go long or short. It can also be configured for reversal trading to cope with more complex market situations. There is room for optimizing parameters, trading logic etc. to make the strategy perform even better.

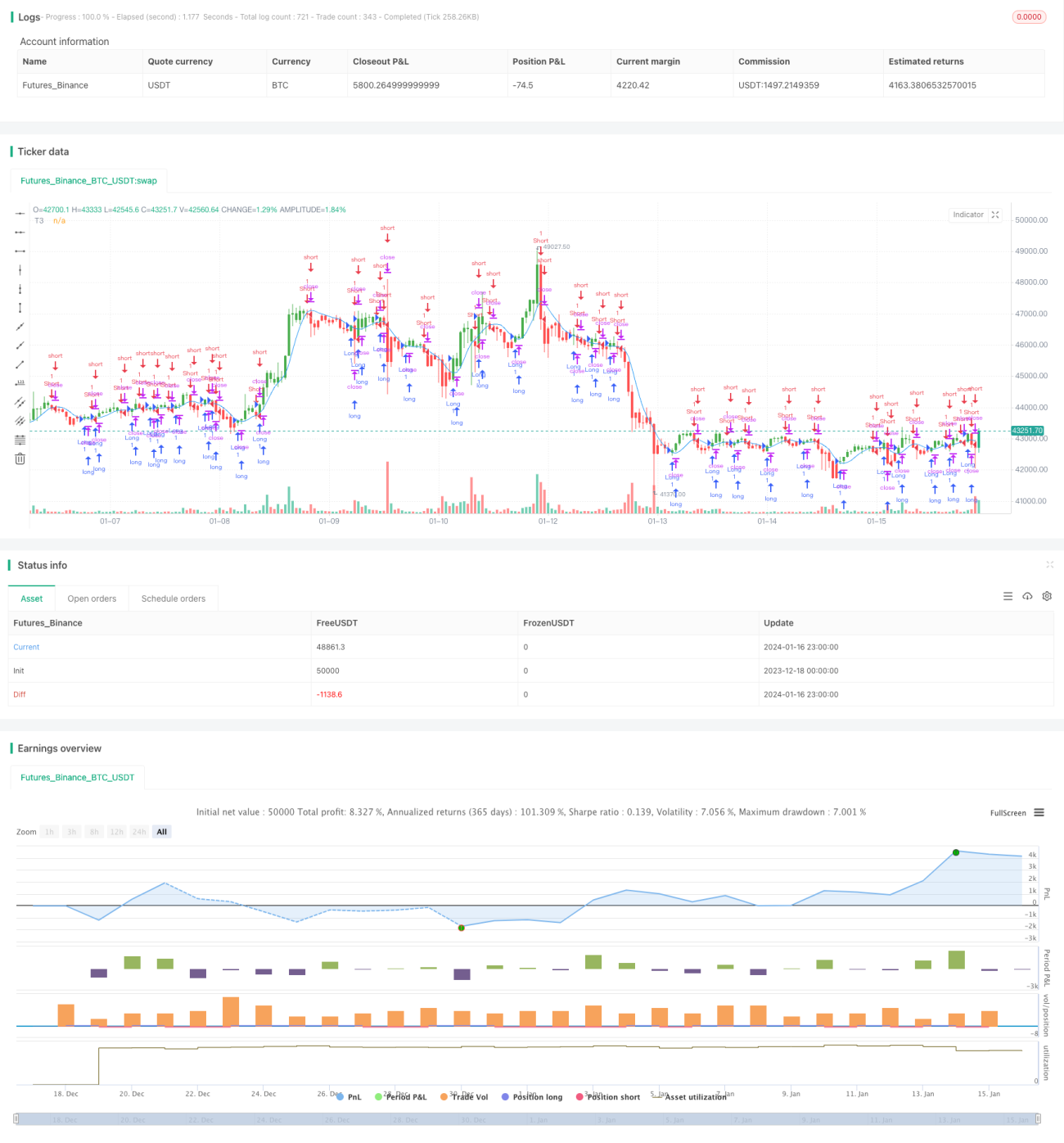

/*backtest

start: 2023-12-18 00:00:00

end: 2024-01-17 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.00 29/11/2017

// This indicator plots the moving average described in the January, 1998 issue- 1