An Analysis of Quantitative Trading Strategy Based on Gaussian Error Function

Overview

This strategy is a quantitative trading strategy based on P-Signal indicator calculated by Gaussian error function to measure price changes. It uses P-Signal to determine price trend and turning points for entries and exits.

Strategy Logic

The core indicator of this strategy is P-Signal. The calculation formula of P-Signal is:

fPSignal(ser, int) =>

nStDev = stdev(ser, int)

nSma = sma(ser, int)

fErf(nStDev > 0 ? nSma/nStDev/sqrt(2) : 1.0)

Here ser represents the price series, int represents the parameter nPoints, which is the number of bars to look back. This formula consists of three parts:

- nStDev is the standard deviation of price;

- nSma is the simple moving average of price;

- fErf is the Gaussian error function.

The meaning of the whole formula is to take the moving average of price divided by the standard deviation of price, then divided by sqrt(2) for standardization, and finally mapped to (-1, 1) range by the Gaussian error function. That is, if the price fluctuation is greater than the average, P-Signal is close to 1; if the price fluctuation is less than the average, P-Signal is close to -1.

The strategy uses the value of P-Signal and the sign of its change to determine entries and exits:

strategy.entry("long", strategy.long, 1, when = nPSignal < 0 and ndPSignal > 0)

strategy.close("long", when = nPSignal > 0 and ndPSignal < 0)

It goes long when P-Signal is less than 0 and change to positive. It closes position when P-Signal is greater than 0 and change to negative.

Advantages

The advantages of this strategy include:

- Using Gaussian error function to fit price distribution. Gaussian error function can fit normal distribution very well, which is in line with most financial time series distributions.

- Automatically adjusting parameters by standard deviation of price. This makes the strategy more robust across different market conditions.

- P-Signal combines the advantages of trend following and mean reversion. It considers both price fluctuation trend and reversal points, which helps capturing opportunities in both trend trading and reversal trading.

Risks

There are also some risks with this strategy:

- High frequency trading risk. As a typical high frequency trading strategy, it may generate more trades, thus bearing higher transaction costs and slippage risks.

- Underperformance in ranging markets. P-Signal may produce many false signals when price has no clear trend or pattern.

- Difficult parameter optimization. Complex relationship between multiple parameters makes parameter optimization challenging.

To reduce those risks, some measures can be taken into consideration: adding filters to reduce trade frequency; optimizing parameter combination and transaction costs setting; live testing and choosing suitable products.

Enhancement

There is room for further enhancement:

- Adding filters to avoid false signals, eg. AND/OR with other indicators to filter out some noise.

- Optimizing parameter combination. Adjusting the size of nPoints across different products and timeframes to improve stability.

- Considering dynamic parameters. Adaptively adjusting nPoints according to market volatility may improve robustness.

- Incorporating machine learning methods. Using AI algorithms on parameters, filters and cross-product timing optimization.

Conclusion

In conclusion, the core idea of this strategy is innovative, fitting price distribution with Gaussian function and automatically adjusting parameters. But as a high frequency trading strategy, it requires further testing and optimization on risk control and parameter tuning before stable profitability in live trading, especially as a high frequency trading strategy.

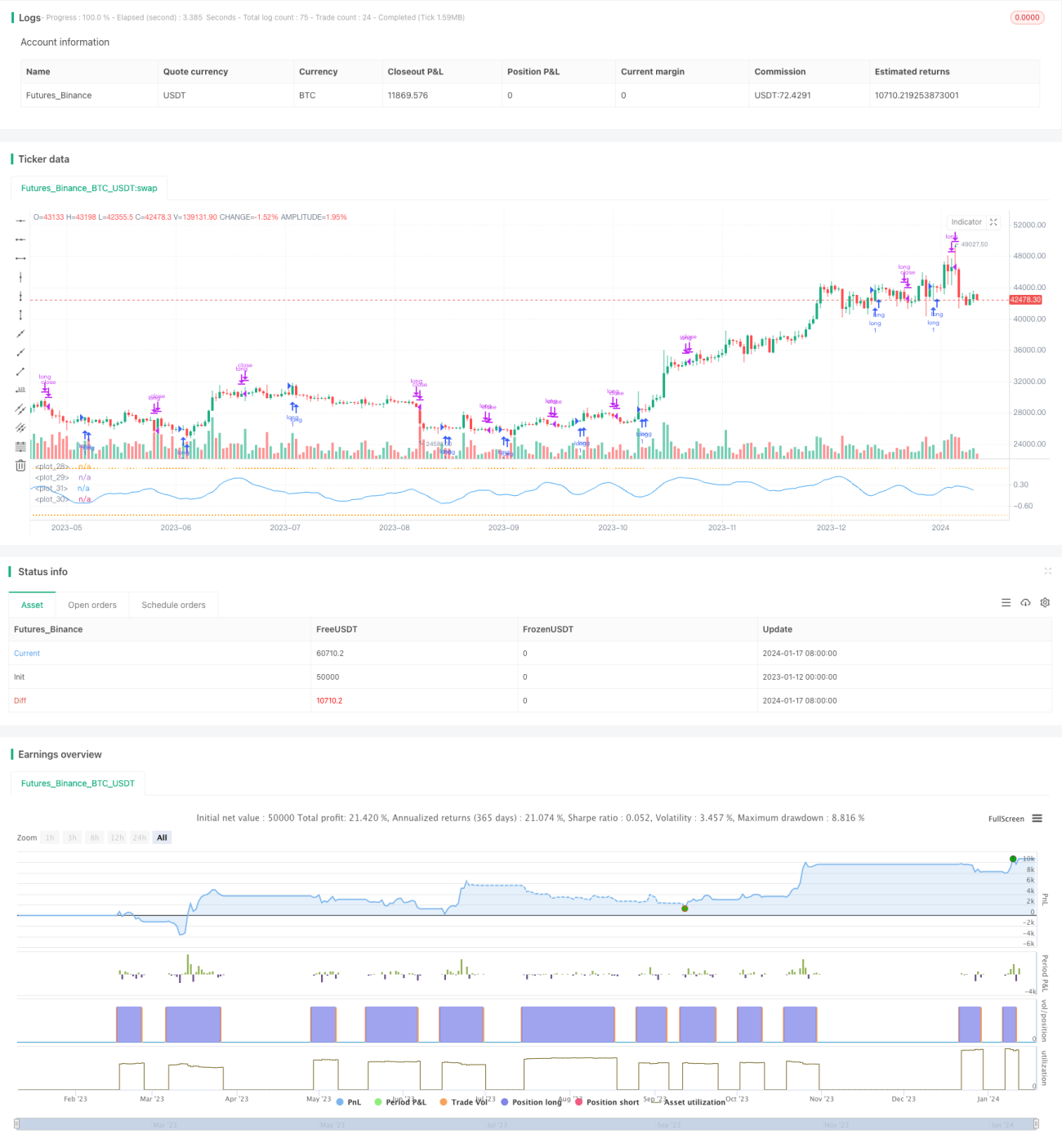

/*backtest

start: 2023-01-12 00:00:00

end: 2024-01-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// **********************************************************************************************************

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// P-Signal Strategy © Kharevsky

// @version=4- 1