Fibonacci Average Candle with Moving Average Strategy for Quantitative Trading

Overview

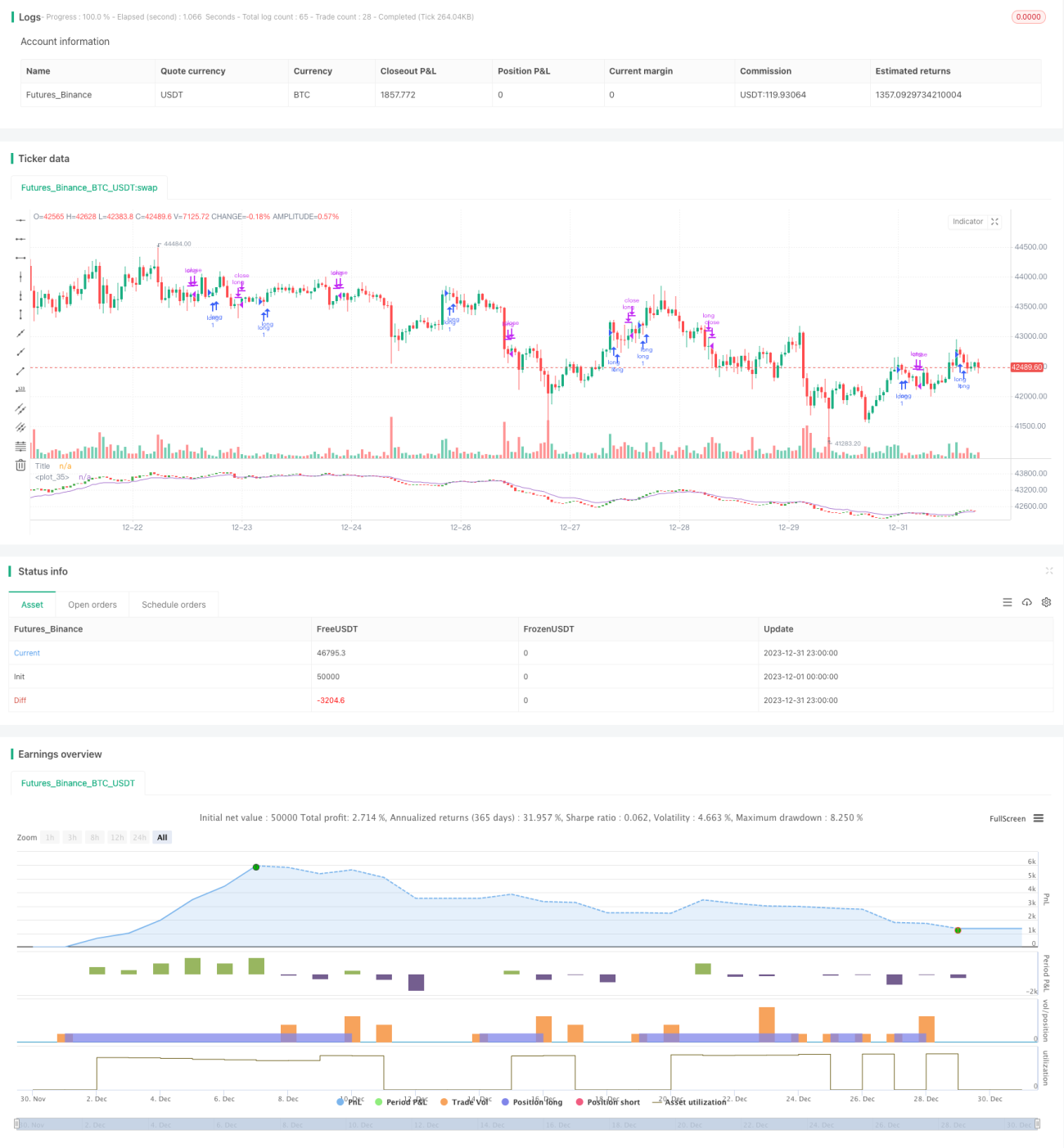

This strategy constructs average candles and moving averages based on the Fibonacci sequence to implement quantitative trading with only long positions and no short positions. Initial tests show that this strategy performs better on larger timeframes.

Strategy Principle

The main steps of this strategy are:

-

Calculate the average close, high, low and open prices of the most recent 10 Fibonacci cycles to construct an average candle.

-

Compute 1-, 2-, 3-, 5-, 8-, 13-, 21-, 34- and 55-period exponential moving averages (EMA) of the average close price, and take their average to obtain the average EMA.

-

Set long and close conditions: open long position when the average candle shows bullish patterns (like closing above open, bullish engulfing) and close is above average EMA; close long position when average candle shows bearish patterns (like closing below open, bearish engulfing) and close is below average EMA.

By calculating average candles to filter price fluctuations and combining with moving average indicators to generate trading signals, this strategy can effectively identify trends and control trading risks.

Advantages

-

Average candles based on Fibonacci sequence can filter random price noise effectively and identify trend signals.

-

Average of multiple EMAs enhances stability of support/resistance levels and improves signal quality.

-

Only long positions reduces number of trades, lowers trading costs and slippage impacts.

-

Performs well on larger timeframes, suitable for medium-to-long term trading.

Risks

-

Only-long strategy can incur significant losses in bearish markets.

-

EMA lines are prone to lagging, potentially missing best entry points.

-

Overly pursuing large timeframes may miss opportunities in shorter timeframes.

-

Limited parameter optimization space means real trading performance may underperform backtest results.

Enhancement Areas

-

Can test adding appropriate stop loss to exit positions when losses mount.

-

Can combine volatility measures like ATR to dynamically adjust position sizing.

-

Can test taking short positions appropriately during downtrends to increase profits.

-

Can optimize EMA period parameters to find best combinations.

Conclusion

This strategy identifies trend signals for quantitative trading by constructing Fibonacci average candles and moving average indicators. It takes advantage of filtering price noise with average candles and reducing trading costs by only going long. It also has the risks of bearish markets for only-long positions and EMA lagging issues. Overall, this strategy controls trading risks from multiple aspects and performs well on larger timeframes, suitable for medium-to-long term trading. Further optimizations can improve robustness and profitability.

- 1