RSI 5 Momentum Trading Strategy

Overview

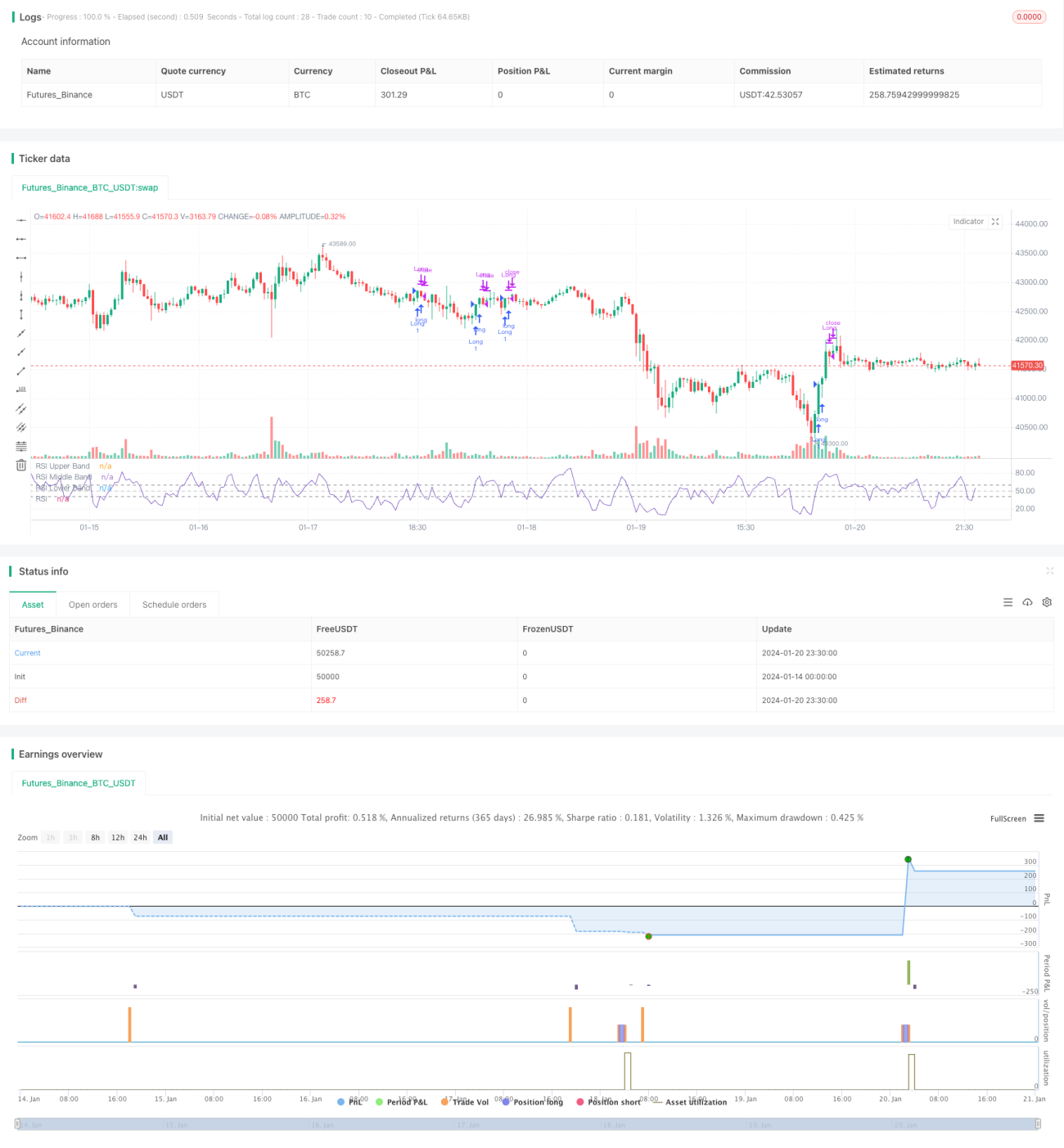

This is a short-term trading strategy based on the RSI (Relative Strength Index) indicator. It utilizes RSI to identify potential strength and weakness in the market, thus assisting trading decisions.

The strategy uses a 5-period RSI to capture short-term price momentum. It determines entry and stop loss levels based on peaks and troughs of the RSI curve.

Strategy Logic

Long entry conditions: previous candle's RSI below 50; current candle's RSI above 60.

Exit conditions: when the RSI curve makes lower lows, indicating weakening trend, close long positions.

Advantage Analysis

- RSI effectively identifies reversal points in prices, as RSI peaks and troughs combinations have strong signaling effects.

- The 5-period RSI captures fast price fluctuations for short-term trading.

- The strategy rules are clear and simple to implement.

Risk Analysis

- RSI may generate false signals, causing unnecessary stop loss.

- High trading frequency from short-term trading can incur larger slippage costs.

- Parameters like RSI periods, threshold levels require fine tuning for actual trading.

Optimization:

- Adding filter indicators like MACD and KD to reduce errors.

- Relaxing stop loss levels to avoid oversensitivity.

- Adjusting RSI parameters to find optimal parameter combinations.

Summary

The strategy utilizes the reversal pattern of RSI peaks and troughs to set clear long entry and stop loss rules. The logic is simple and practical but has some instability. Strategy stability can be improved through parameter optimization and indicator combinations.

- 1