MACD Double Optimization Trading Strategy

II. Strategy Overview

This strategy uses the MACD indicator and moving average cross principles to construct trading signals. Its advantage is that it can optimize the parameters of MACD separately for long and short directions, so that the parameters can be optimally configured for different market directions.

III. Strategy Principle

-

Calculate the MACD indicator separately for long and short directions. One set of parameters is used for long, and another set of parameters is used for short, which can be freely configured.

-

Judge the trading signals generated by the crossover of the MACD line and the Signal line. Look for bullish crossover for long, and bearish crossover for short.

-

You can configure whether the Signal line also needs to cross to trigger the signal, so as to avoid false signals.

-

After entering long or short position, close the position when a reverse crossover occurs.

IV. Advantages of the Strategy

-

Two-way parameter optimization: parameters for long and short can be freely optimized to be optimally configured for market directions separately.

-

Configurable signal smoothing: The Signal parameter can control the smoothness of the signal line to filter out false signals.

-

Configurable signal filtering: Can be configured whether the Signal line crossover is required to trigger to avoid false signals.

-

Fine-tuned position control: Long or short alone can be enabled separately, or long and short can be done at the same time.

V. Risks of the Strategy

-

MACD lag: MACD itself has some lag which may miss fast reversals.

-

Risk of switching between long and short: Frequent position switching may occur when the market changes rapidly.

-

Parameter risk: Improper parameter configurations may fail to capture market characteristics.

-

Lack of stop loss protection: Reasonable stop loss should be set to control single loss.

Methods to manage risks:

-

Combine with other indicators to judge the big picture and avoid chasing highs and selling lows.

-

Set signal delay and smoothing parameters to reduce error signals.

-

Repeatedly test and optimize parameters to match the rhythm of the market in different cycles.

-

Set up stop loss and take profit mechanism to control single loss.

VI. Directions for Optimization

Some ways this strategy can be further optimized:

-

Test different combinations of fast line and slow line length parameters to find the optimal parameters for market conditions in different cycles.

-

Test different Signal line parameters. Smoother signal lines can filter out more noise.

-

Test the difference between turning on and off the Signal line crossover filter to find the optimal balance.

-

Set the optimal stop loss and take profit ratio based on backtest results.

-

Try only long or only short to see if the strategy effect can be maximized.

VII. Summary

By configuring long and short parameters separately, this MACD Double Optimization Trading Strategy realizes optimization tailored to different market directions, and allows free adjustment of the participation direction. At the same time, signal filtering mechanisms are introduced to avoid erroneous signals. Through parameter optimization and risk management measures, the strategy effect can be further improved.

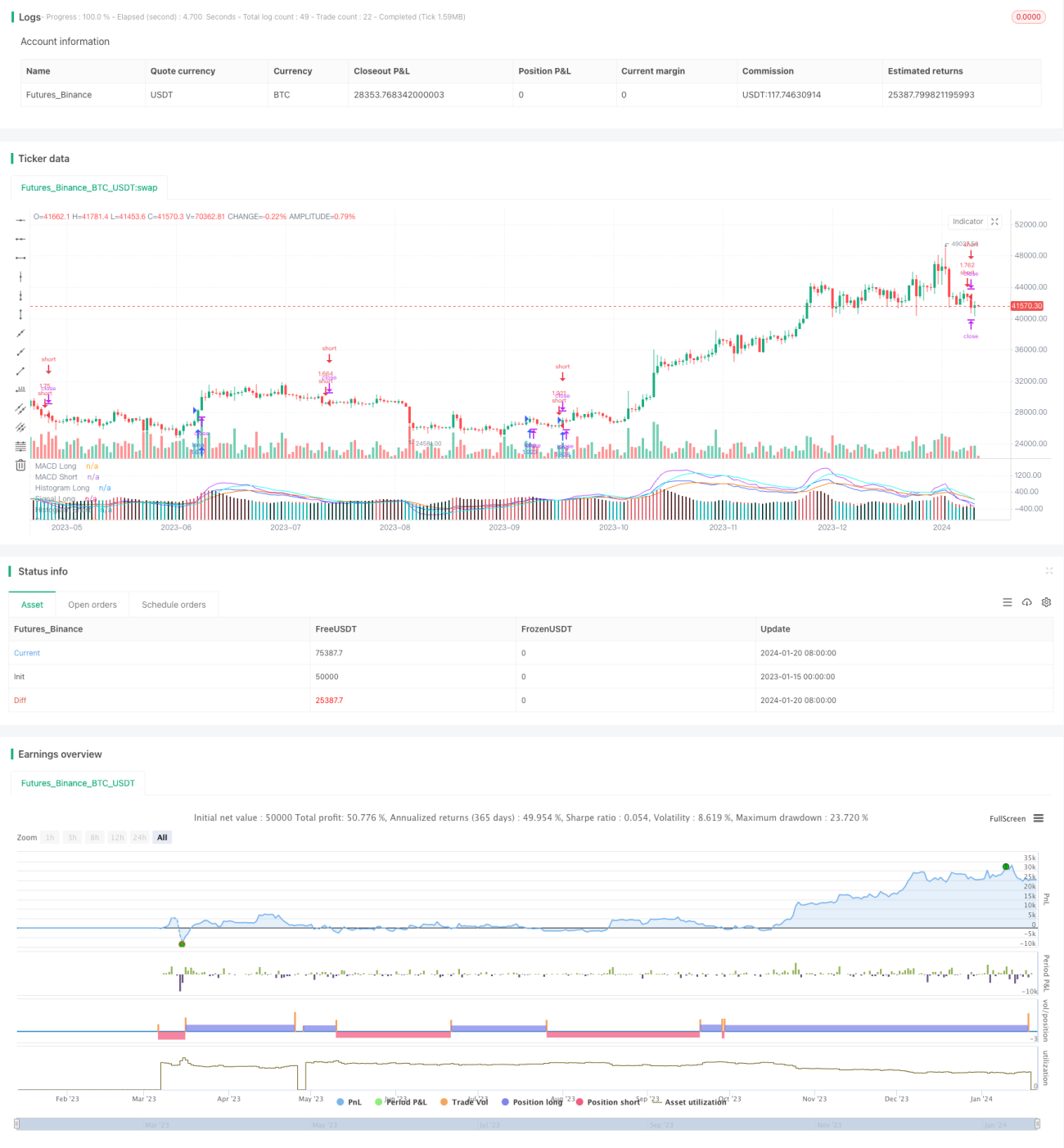

/*backtest

start: 2023-01-15 00:00:00

end: 2024-01-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Gentleman-Goat & TradingTools.Software/Optimizer

strategy(title="MACD Short/Long Strategy for TradingView Input Optimizer", shorttitle="MACD Short/Long TVIO", initial_capital=1000, default_qty_value=100, default_qty_type=strategy.percent_of_equity)- 1