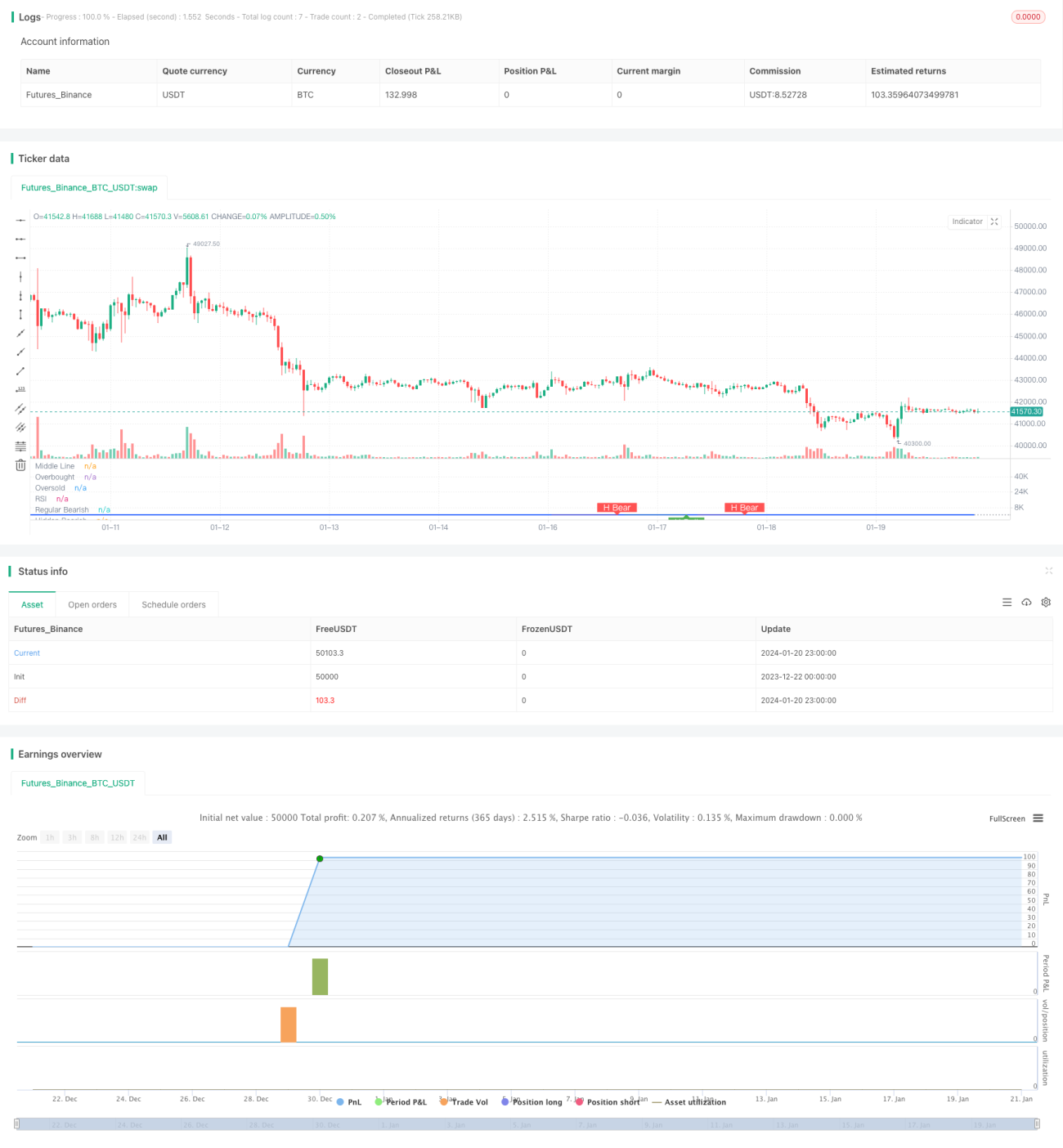

RSI Divergence Trading Strategy

Strategy Name

RSI Bullish/Bearish Divergence Trading Strategy

Overview

This strategy identifies regular and hidden bullish/bearish RSI divergence signals to determine long and short positions.

Principles

When price makes a new high and RSI fails to make a new high, it forms bullish divergence, which is treated as selling signal. When price makes a new low and RSI fails to make a new low, it forms bearish divergence, which is treated as buying signal. Regular divergence refers to the obvious divergence between price and RSI while hidden divergence means relatively concealed divergence between them. Long or short positions are determined based on identified regular or hidden bullish/bearish divergence signals.

Advantage Analysis

- Divergence signals have relatively high reliability with higher winning rate.

- Identification of both regular and hidden bullish/bearish divergence provides extensive coverage.

- Adjustable RSI parameters make it adaptable to different market environments.

Risk Analysis

- Hidden divergence signals have higher probability of misjudgment.

- Manual review is needed to filter out misjudged signals.

- Effectiveness depends on RSI parameter settings.

Optimization Directions

- Optimize RSI parameters to find best parameter combinations.

- Add machine learning algorithms for automatic identification of true signals.

- Incorporate more indicators to verify signal reliability.

Summary

This strategy identifies RSI divergence trading signals based on regular and hidden bullish/bearish divergence to determine long or short positions, which provides relatively higher winning rate. Further improvements on strategy effectiveness could be achieved by optimizing RSI parameters, adding other validating indicators.

/*backtest

start: 2023-12-22 00:00:00

end: 2024-01-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Divergence Indicator")

len = input.int(title="RSI Period", minval=1, defval=14)

src = input(title="RSI Source", defval=close)- 1