Dynamic Grid Trading Strategy

1

Follow

1802

Followers

Overview

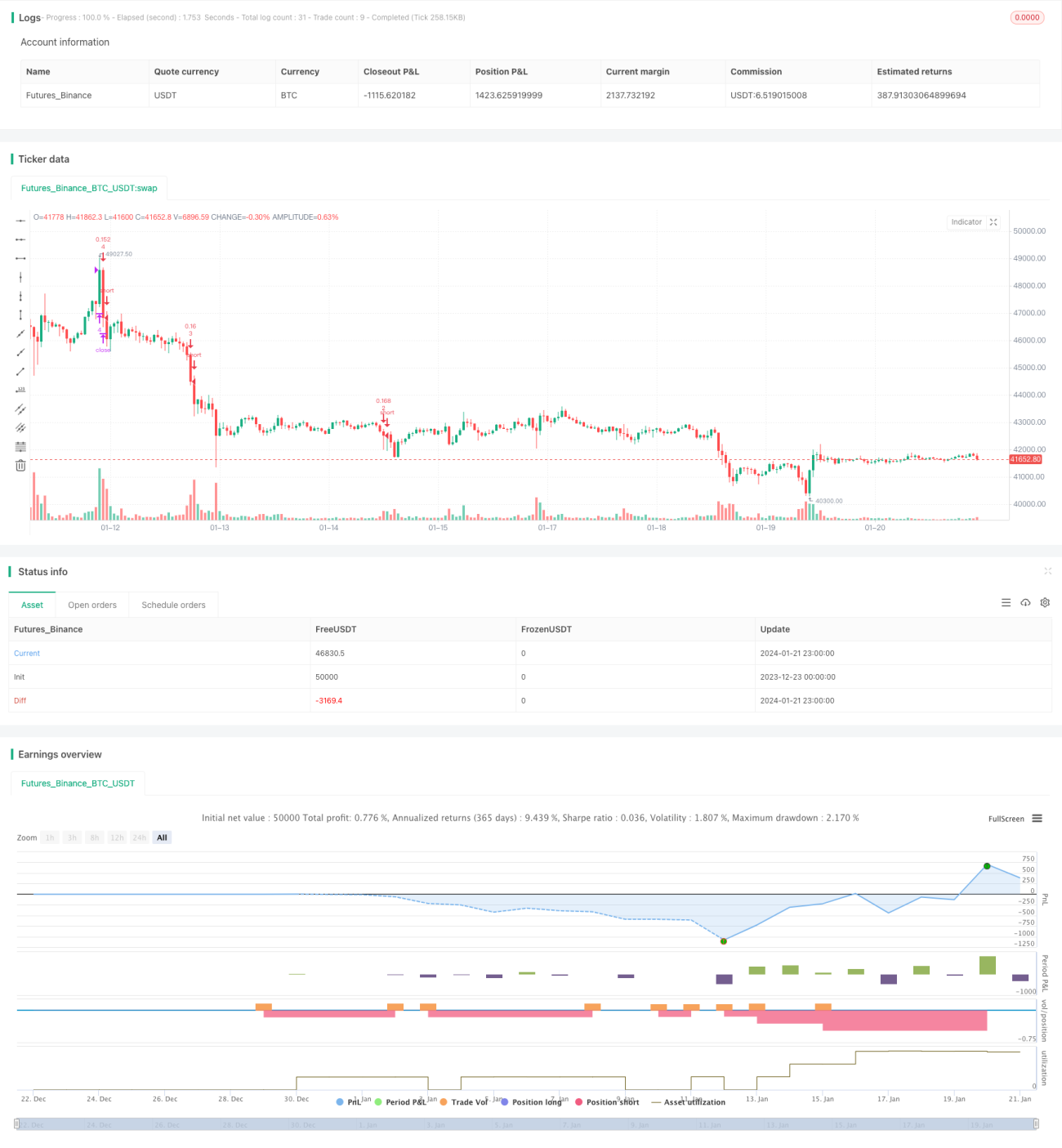

This strategy implements grid trading by placing multiple parallel buy and sell orders within a price range. It adjusts the grid range and lines based on market fluctuations to profit.

Strategy Logic

- Set upper and lower bounds of the grid, which can be manually configured or automatically calculated based on recent high and low prices.

- Calculate grid interval width according to specified number of grid lines.

- Generate grid line prices array with corresponding quantity.

- When price drops below a grid line, open long order below it; when price rises above a grid line, close short order above it.

- Dynamically adjust bounds, interval width and grid line prices to adapt the strategy to market changes.

Advantage Analysis

- Can steadily profit in range-bound and volatile market, regardless of trend direction.

- Supports both manual and automatic parameter settings for strong adaptability.

- Optimizable parameters like grid quantity, interval width and order size for better reward.

- Embedded position control for lower risk.

- Dynamic grid range adjustment enhances adaptability.

Risk Analysis

- Severe loss may occur in strong trending market.

- Improper grid quantity and position settings may amplify risk.

- Auto calculated grid range may fail in extreme price swings.

Risk Management:

- Optimize grid parameters and strictly control total position.

- Close strategy before significant price move.

- Judge market condition with trend indicators, close strategy when necessary.

Optimization Directions

- Choose optimal grid quantity based on market character and capital scale.

- Test different periods to optimize auto parameters.

- Optimize order size calculation for more steady reward.

- Add indicators for trend identification and strategy close conditions.

Summary

The dynamic grid trading strategy adapts to the market by adjusting grid parameters. It profits in range-bound and volatile market. With proper position control, the risk is mitigated. Optimizing grid settings and incorporating trend judgment indicators can further improve the strategy's stability.

Source

Pine

/*backtest

start: 2023-12-23 00:00:00

end: 2024-01-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("sarasa srinivasa kumar", overlay=true, pyramiding=14, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.1)

i_autoBounds = input(group="Grid Bounds", title="Use Auto Bounds?", defval=true, type=input.bool) // calculate upper and lower bound of the grid automatically? This will theorhetically be less profitable, but will certainly require less attention

i_boundSrc = input(group="Grid Bounds", title="(Auto) Bound Source", defval="Hi & Low", options=["Hi & Low", "Average"]) // should bounds of the auto grid be calculated from recent High & Low, or from a Simple Moving AverageStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1