An ATR Channel Breakout Quantitative Trading Strategy

Overview

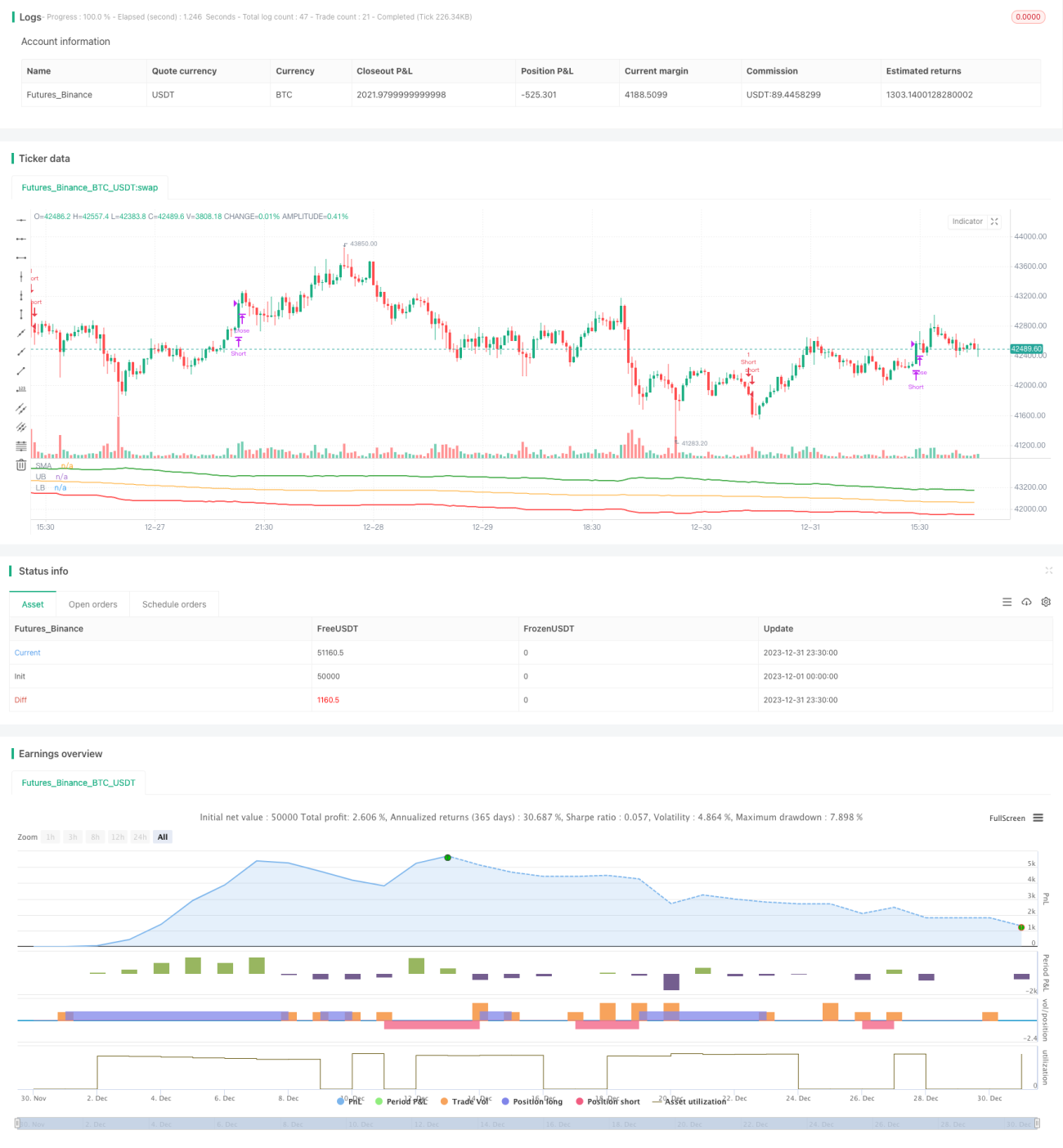

This strategy trades based on channels formed using the Average True Range (ATR). Specifically, it calculates a SMA line over a certain period, then uses the ATR values to determine the upper and lower bands of the channel. It goes long when the price breaks out above the upper band, and goes short when the price breaks below the lower band. Positions are closed when the price crosses back below the SMA line.

Strategy Logic

The core logic of this strategy is based on ATR channels. The ATR indicator can effectively reflect market volatility and price movements, and is usually used to determine stop loss and take profit levels. The strategy first calculates the SMA line over n periods (default 150), then uses the ATR value and coefficient to determine the upper and lower channel bands. The specific formulas are:

Upper Band = SMA + ATR Value × Upper Band Coefficient (default 4)

Lower Band = SMA - ATR Value × Lower Band Coefficient (default 4)

When the price breaks out above the upper band, it indicates the start of a trend channel and upside momentum, so a long position is taken. When the price breaks below the lower band, it signals the start of a reversal, so a short position is taken. Exits occur when the price crosses back below the SMA line, closing out all longs, or crosses back above the SMA line, closing out all shorts.

Advantages

-

Using ATR as the reference for channel range can more accurately capture market volatility. ATR effectively measures market volatility for better channel sizing.

-

The dual filters of SMA and ATR channel ensure more reliable trade signals, reducing false signals.

-

Parameters can be optimized to maximize the capture of upside and downside price movements for trend trading profits. Both channel width and lookback period are tunable.

-

Simple and clear logic that is easy to understand and implement. Intuitive long/short decisions based on indicators and channel breakouts.

-

Includes both long and short trades to profit from up and down trends.

Risk Analysis

-

Channel breakout trades are prone to losses at key reversal points if breakout turns out to be false.

-

SMA has systemic risk of lagging market turns. Price may already be falling but SMA has yet to turn down.

-

Poor ATR parameter and coefficient settings can result in irrational channel ranges.

-

Persistent short losses in bull market uptrends, and persistent long losses in bear market downtrends.

Possible solutions:

-

Adjust trade frequency or add filters to avoid losses from false breakouts.

-

Add cross-confirmation with MACD, KDJ to avoid SMA systemic lag risk.

-

Optimize ATR period and coefficient to ensure reasonable channel range.

-

Determine overall market regime for trend bias. Go long in bull trending markets and short in bear trends.

Enhancement Opportunities

Some ways this strategy can be enhanced:

-

Add additional indicator filters to reduce false breakout whipsaws, using MACD, KDJ etc. to confirm signals.

-

Optimize ATR period and channel coefficient to fit current market volatility conditions through extensive backtesting.

-

Incorporate automated stop loss to control maximum loss per trade. Trailing stops are a common implementation.

-

Cut losses quickly when price diverges away from SMA baseline.

-

Incorporate higher timeframe trend analysis to determine bull/bear bias for breakout direction. For example, use weekly to determine overall trend for daily breakout entries.

Summary

This is a classic channel breakout strategy using SMA and ATR channel bands. Its strength lies in more reliable signals from the dual filters, while weakness is the risk of false breakouts. Further improvements can be made through parameter optimization, stop losses, and trend analysis to make it more robust and aligned with market conditions. With tune-up, it can achieve more consistent profits. The simplicity of this strategy makes it worth exploring and optimizing in practice.

- 1