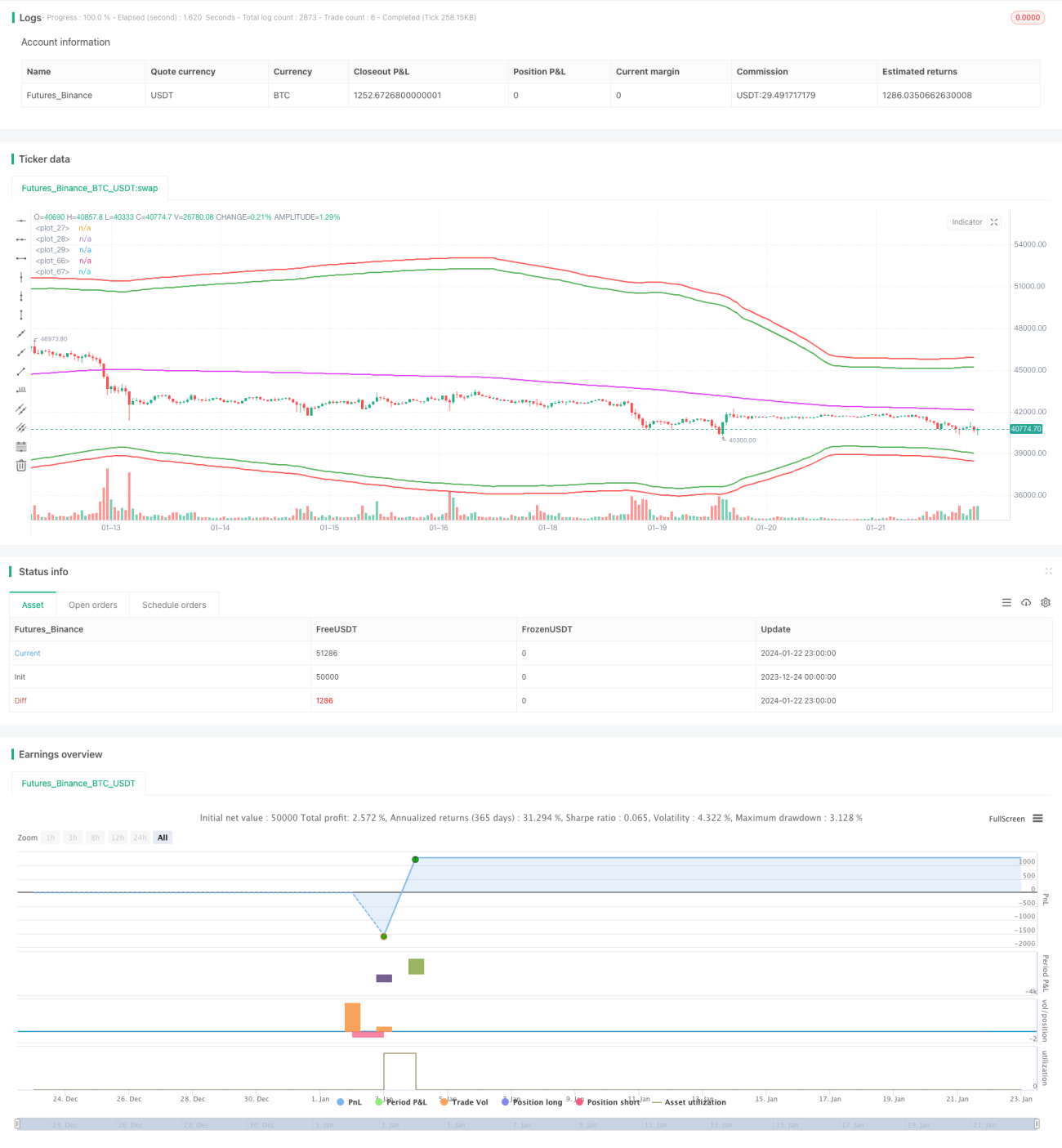

概述

该策略是一个使用布林带作为entries,移动平均线作为close, 以及简单止损百分比作为止损的做市商策略。它在2022年6月份xtbtusd合约上获得了极高的盈利。

策略原理

该策略使用布林带的上下轨作为建仓的机会区域。具体来说,当价格低于下轨时,会开多单建仓;当价格高于上轨时,会开空单建仓。

此外,该策略还使用移动平均线作为平仓的基准。当持有多单时,如果价格高于移动平均线,会选择平仓;同样地,当持有空单时,如果价格低于移动平均线,也会选择平仓。

对于止损,该策略使用的是入场价乘以一定百分比这种简单的滚动止损方式。这可以有效避免单边行情下的巨额亏损。

优势分析

该策略的主要优势有以下几点:

- 使用布林带可以有效捕捉价格的波动性,在波动加剧时获得更多交易机会。

- 做市商策略可以通过双向交易获得买卖双方的手续费收入。

- 采用百分比止损可以主动控制风险,有效避免单边行情下的超大亏损。

风险分析

该策略也存在一些风险:

- 布林带并不总是一个可靠的入场指标,有时会发出错误信号。

- 做市商策略容易在震荡行情中被套牢。

- 百分比止损可能过于武断,无法灵活应对复杂行情。

为了降低这些风险,我们可以考虑结合其他指标进行过滤,优化止损策略的设定,或适当限制头寸规模。

优化方向

该策略还有进一步优化的空间:

- 可以测试不同参数组合找出最优参数。

- 可以加入更多过滤指标进行多因子验证。

- 可以使用机器学习方法自动优化参数。

- 可以考虑使用更精细的止损方式,如抛物线止损。

总结

该策略整体来说是一个非常赚钱的高频做市商策略。它利用布林带提供交易机会,同时控制风险。但我们也需要意识到它存在的问题与不足,并在实盘中谨慎验证。通过进一步优化,该策略有望产生更稳定的超高收益。

策略源码

Pine

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1