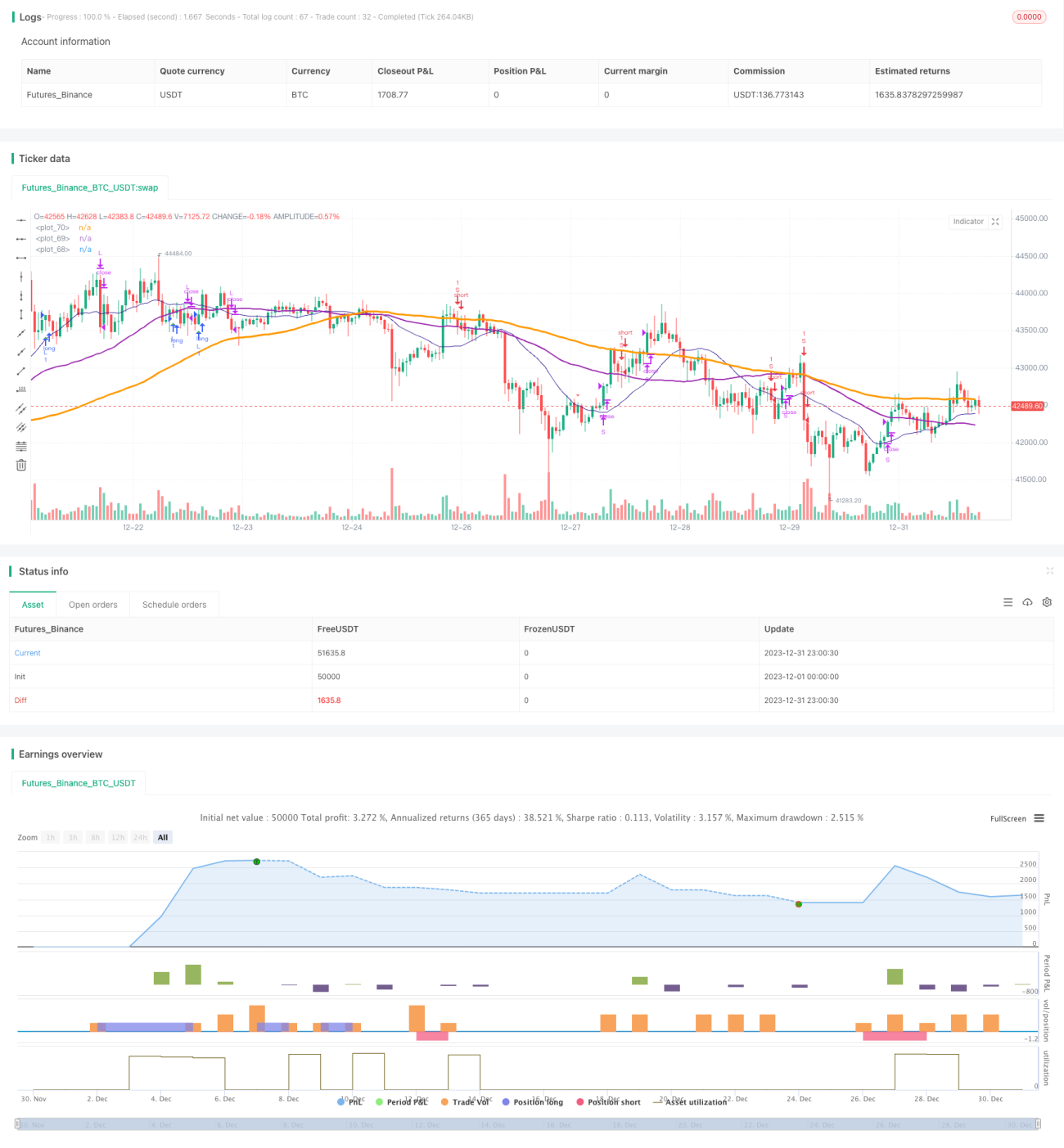

Quantitative Support and Resistance Oscillation Strategy

1

Follow

1802

Followers

Overview

This strategy combines RSI crossover strategy with optimized stop loss strategy to achieve precise logic control and accurate stop loss and take profit. Meanwhile, by introducing signal optimization, it can better grasp the trend and achieve reasonable capital management.

Strategy Principle

- RSI indicator determines overbought and oversold area. Combined with K and D value golden cross and dead cross to form trading signals.

- Introduces candlestick pattern recognition to assist in judging trend signals to avoid wrong trades.

- SMA lines assist in determining trend direction. Uptrend when short period SMA breaks out upper long period SMA.

Advantage Analysis

- RSI parameter optimization determines overbought and oversold area precisely to avoid wrong trades.

- STO parameter optimization, smoothness adjustment filters out noise and improves signal quality.

- Heikin-Ashi technology introduced to recognize candlestick direction change and ensure accurate trading signals.

- SMA lines assist judging major trend direction, avoids trading against the trend.

- Stop loss strategy locks in maximum profit for each trade.

Risk Analysis

- Facing greater risk when market continues going down.

- High trading frequency increases trading cost and slippage cost.

- RSI tends to generate false signals, needs filtering by other indicators.

Strategy Optimization

- Adjust RSI parameters, optimize overbought oversold judgement.

- Adjust STO parameters, smoothness and period to improve signal quality.

- Adjust moving average period to optimize trend judgement.

- Introduce more technical indicators to improve signal accuracy.

- Optimize stop loss ratio to reduce single trade risk.

Conclusion

The strategy integrates advantages of multiple mainstream technical indicators. Through parameter optimization and logic refinement, it balances trading signal quality and stop loss. With certain versatility and steady profitability. Further optimization can improve win rate and profitability.

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//study(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true)

strategy(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true )

smoothK = input(3, minval=1)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1