CMO and WMA Based Dual Moving Average Trading Strategy

Overview

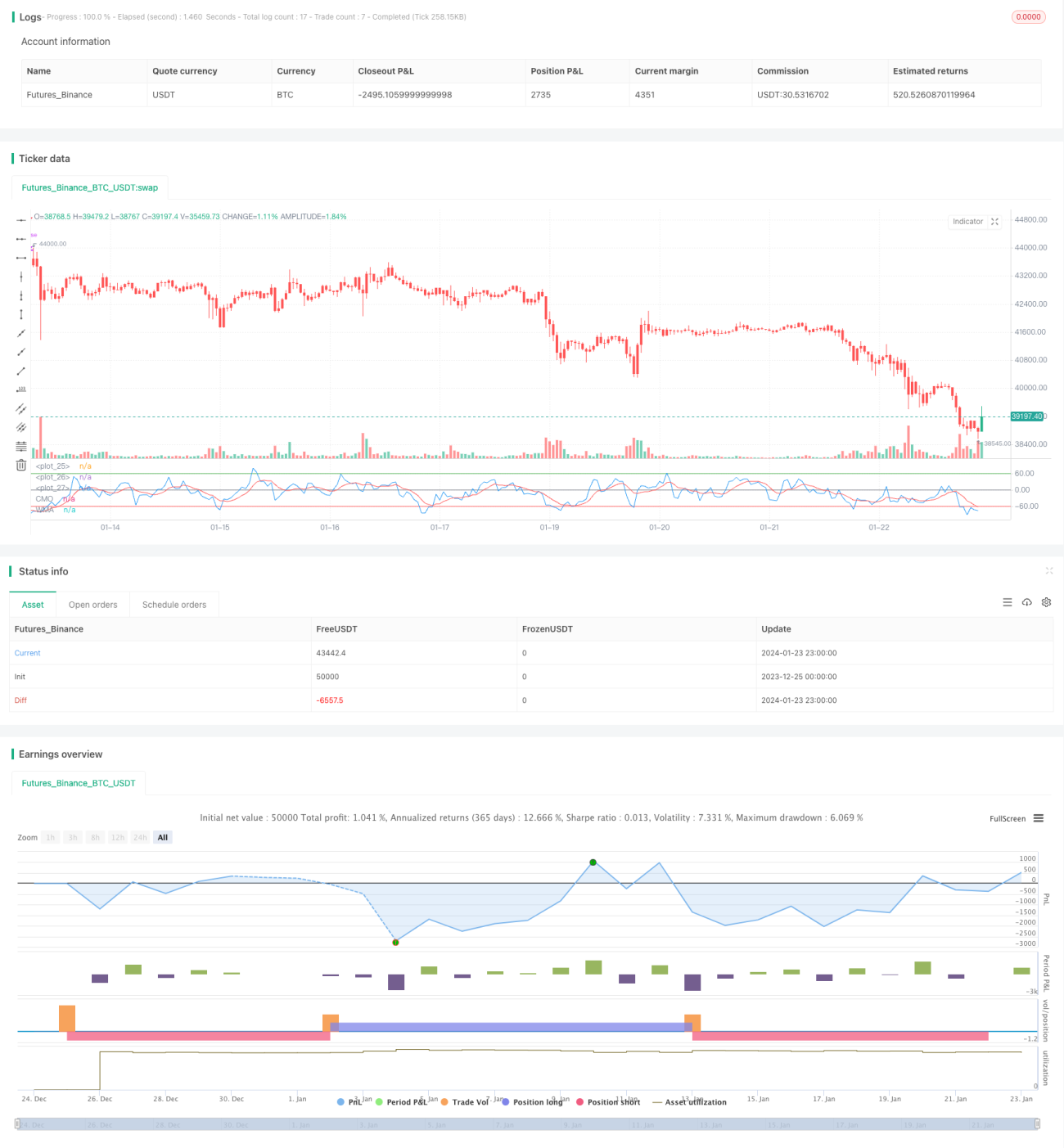

This strategy is a dual moving average trading strategy based on the price momentum indicator Chandre Momentum Oscillator (CMO) and its Weighted Moving Average (WMA). It attempts to identify trend reversals and continuation using CMO crossover its WMA.

Strategy Logic

The strategy first calculates CMO, which measures the net change in price momentum. Positive values indicate upside momentum while negative values indicate downside momentum. It then calculates the WMA of CMO. When CMO crosses above its WMA, a long position is taken; when CMO crosses below its WMA, a short position is taken. The strategy attempts to capture turning points in the trend using CMO and WMA crossovers.

The key steps in calculating CMO are:

- Calculate the daily price change (xMom)

- Take n-day SMA of price change as the "true" price momentum (xSMA_mom)

- Calculate n-day net price change (xMomLength)

- Standardize the net price change (nRes) by dividing by the SMA

- Take m-day WMA of the standardized net price change to get CMO (xWMACMO)

The advantage of this strategy is capturing medium-term trend reversals in price. The absolute magnitude of CMO reflects the strength of the price run, while the WMA helps filter out false breakouts.

Advantage Analysis

The biggest advantage of this strategy is using the absolute value of CMO to gauge market crowd sentiment and using the WMA filter to identify turning points in the medium-term trend. Compared to single moving average strategies, it is better able to capture medium-term trends with higher elasticity.

CMO standardizes price changes and maps them into a -100 to 100 range for easier judgment of market crowd sentiment; absolute magnitude represents strength of current trend. The WMA provides additional filtering on CMO to avoid excessive false signals.

Risk Analysis

The main risks that may exist in this strategy are:

- Improper CMO and WMA parameter settings leading to excessive false signals

- Inability to effectively handle trending oscillations, resulting in high trading frequency and slippage costs

- Failure to identify true long term trends, leading to losses in long term positions

Corresponding optimization methods:

- Adjust CMO and WMA parameters to find optimal combination

- Add supplementary filters like volume energy to avoid trading in oscillating markets

- Incorporate longer term indicators like 90-day MA to avoid missing opportunities in long term trends

Optimization Directions

The main optimization directions for this strategy are around parameter tuning, signal filtering and stop losses:

- CMO and WMA parameter optimization through brute force testing

- Supplementary signal filtering using volume, strength indicators etc. to avoid false breakouts

- Incorporating dynamic stop losses to exit when price breaks back below CMO and WMA

- Considering Breakout Failure patterns as entry signals when CMO and WMA first break key levels but quickly fall back

- Judging the major trend using longer term indicators to avoid counter-trend trading

Conclusion

Overall this strategy uses CMO to judge trend strength and turning points, combined with the WMA filter to generate trading signals, a typical dual moving average system. Compared to single MA strategies, it has a stronger advantage in capturing elastic medium-term trends. But there is still room for optimization around parameters, filtering and stop losses. Controlling trade frequency and incorporating dynamic stops can further improve system stability.

/*backtest

start: 2023-12-25 00:00:00

end: 2024-01-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/10/2018

// This indicator plots Chandre Momentum Oscillator and its WMA on the - 1