Two Year New High Retracement Moving Average Strategy

Overview

This strategy is based on the unique calculation of the two-year new high price and moving average of stocks. It generates a buy signal when the stock price retreats to the 13-day exponential moving average after reaching a two-year high.

Strategy Principle

The core logic of this strategy is based on the following unique calculations:

-

When the stock price reaches a new high over the last two years, it forms a short-term peak. This is a critical price level.

-

When the price retreats from this new high and pulls back to the 13-day exponential moving average, it presents a good buying opportunity. This utilizes the price consolidation pattern.

-

In addition, when the buy signal triggers, the stock price must be within 10% range of the two-year high, not too far away. It also needs to be below 13-day line and above 21-day line to ensure proper timing.

-

For open positions, if the price breaks 5% below the 21-day MA line or declines 20% from the two-year high, the position will be stopped out to lock in profits.

Strategy Advantages

This is a long-term breakout strategy with these advantages:

-

The unique two-year high price can effectively identify potential trend reversal opportunities.

-

The 13-day EMA line serves as the entry filter to avoid whipsaws and determine stronger momentum.

-

The unique calculations generate signals based on price action, avoiding subjective interference.

-

Reasonable stop loss allows locking in most profits.

Risks and Solutions

There are also some risks mainly as follows:

-

Markets can experience deep drawdowns, unable to stop out in time. Need to assess the overall environment to decide whether to cut losses resolutely.

-

Overnight big gaps may prevent perfect stop loss. Hence stop loss percentage needs to be widened to adapt.

-

The 13-day line may not filter out consolidations well, generating excessive false signals. Can consider extending to 21-day line.

-

New high price may not work well to determine trend changes. Other indicators can combine to enhance effectiveness.

Strategy Optimization Suggestions

There is room for further optimization:

-

Incorporate other tools to judge overall market conditions, avoiding unnecessary positions.

-

Add momentum indicators to better avoid whipsaw ranges.

-

Optimize moving average parameters to better capture price patterns.

-

Utilize machine learning to dynamically optimize the two-year high parameter for more flexibility.

Conclusion

In summary, this is a unique long term breakout strategy, with the key being the two-year high price level and the 13-day EMA line serving as entry filter. It has certain advantages but also room for improvements, worth further research and exploration.

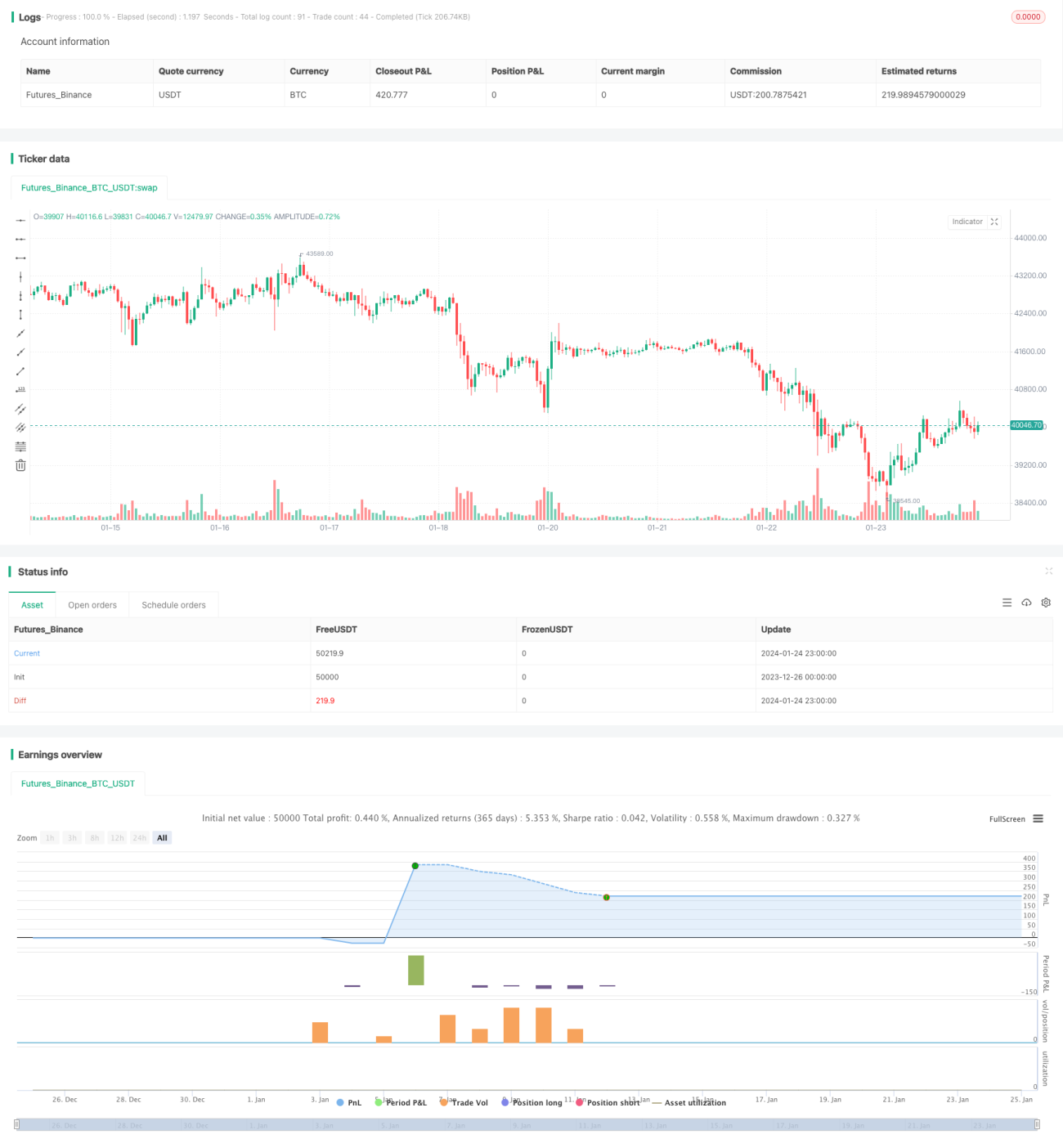

/*backtest

start: 2023-12-26 00:00:00

end: 2024-01-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Part Timer

//This script accepts from and to date parameter for backtesting. - 1