Solid Trend Following Strategy

Overview

This strategy combines SSL Hybrid Channel, QQE MOD and Waddah Attar Explosion indicator to build a robust trend following strategy. It can achieve steady profit on major cryptocurrencies like BTC and ETH over medium to long term timeframes.

Strategy Logic

Entry Logic

Long Entry Conditions:

- Close price above SSL Hybrid Baseline

- QQE MOD turns blue

- Waddah Attar Explosion indicator green

Short Entry Conditions:

- Close price below SSL Hybrid Baseline

- QQE MOD turns red

- Waddah Attar Explosion indicator red

Exit Logic

Long Exit Condition:

- QQE MOD turns red

Short Exit Condition:

- QQE MOD turns blue

Advantage Analysis

The advantages of this strategy:

-

Combination of 3 indicators ensures accuracy and reliability of trading signals

-

SSL baseline and QQE MOD effectively capture trend direction

-

Waddah Attar Explosion further validates signals to avoid false breakouts

-

Clean code structure, easy to understand and modify

-

Complete stop loss, take profit and risk management system to control risks

-

Excellent backtest results over longer timeframes (e.g. 1H, 4H)

Risk Analysis

The risks of this strategy:

-

Poor backtest results over short timeframes (e.g. 5m)

-

Stop loss may trigger frequently during high volatility

-

Results may vary across different cryptocurrencies

Possible solutions:

-

Only use over medium to long term

-

Widen stop loss to prevent too frequent triggering

-

Test on more assets to find suitable ones

Optimization Directions

Potential improvements:

-

Test different parameter sets to find optimum combination

-

Incorporate machine learning for better adaptability

-

Combine with sentiment and other factors to enhance stability

-

Adjust for specific industries based on characteristics

-

Add algorithmic trading module to boost returns

Conclusion

Overall this strategy is highly recommended. With sound logic, full risk control and stability across suitable assets and timeframes, it has great profit potential. Continuous enhancements will turn it into a highly efficient trading tool.

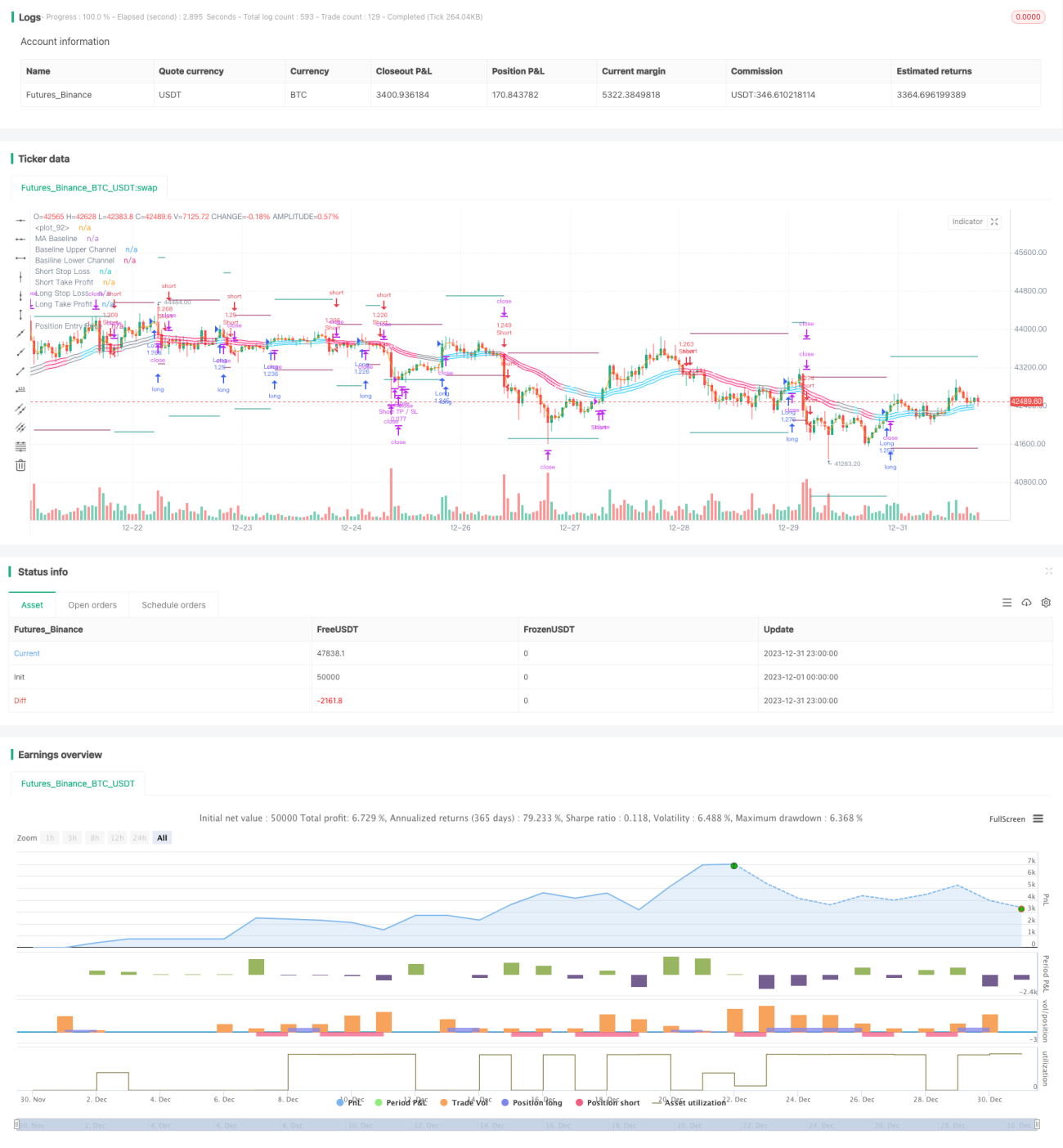

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1